AP Presentation

E N D

Presentation Transcript

Accounts Payable RizalinaNacachi-Raymundo, CPA

Accounts Payable • Introduction • Definition • Concepts • Accounts Payable Process • AP Flow Chart • Documentations • Three–way match • Approvals • Internal Control • End-of-Discussion practice

Definition Account payable is defined as a liability to a creditor, carried on open account, usually for purchases of goods and services. It is an accounting entry that represents an entity's obligation to pay off a short-term debt to its creditors. On many balance sheets, the accounts payable entry appears under the heading current liabilities.

Definition The term accounts payable can also refer to the person or staff that processes vendor invoices and pays the company's bills. That's why a supplier who hasn't received payment from a customer will phone and ask to speak with "accounts payable." HOME

Concepts When a company orders and receives goods (or services) in advance of paying for them, we say that the company is purchasing the goods on account or on credit. The supplier (or vendor) of the goods on credit is also referred to as a creditor. If the company receiving the goods does not sign a promissory note, the vendor's bill or invoice will be recorded by the company in its liability account Accounts Payable (or Trade Payables).

Concepts As it is expected for a liability account, Accounts Payable will normally have a credit balance. Hence, when a vendor invoice is recorded, Accounts Payable will be credited and another account must be debited (as required by double-entry accounting). When an account payable is paid, Accounts Payable will be debited and Cash will be credited. Therefore, the credit balance in Accounts Payable should be equal to the amount of vendor invoices that have been recorded but have not yet been paid.

Concepts Under the accrual method of accounting, the company receiving goods or services on credit must report the liability no later than the date they were received. The same date is used to record the debit entry to an expense or asset account as appropriate. Hence, accountants say that under the accrual method of accounting expenses are reported when they are incurred (not when they are paid). HOME

Accounts Payable Process The accounts payable process involves reviewing an enormous amount of detail to ensure that only legitimate and accurate amounts are entered in the accounting system. Much of the information that needs to be reviewed will be found in the following documents: • purchase orders issued by the company • receiving reports issued by the company • invoices from the company's vendors • contracts and other agreements

Accounts Payable Process The accuracy and completeness of a company's financial statements are dependent on the accounts payable process. A well-run accounts payable process will include: • the timely processing of accurate and legitimate vendor invoices, • accurate recording in the appropriate general ledger accounts, and • the accrual of obligations and expenses that have not yet been completely processed.

Accounts Payable Process The efficiency and effectiveness of the accounts payable process will also affect the company's cash position, credit rating, and relationships with its suppliers. The accounts payable process or function is immensely important since it involves nearly all of a company's payments outside of payroll. It might be carried out by an accounts payable department in a large corporation, by a small staff in a medium-sized company, or by a bookkeeper or perhaps the owner in a small business.

Accounts Payable Process Regardless of the company's size, the mission of accounts payable is to ”pay only the company's bills and invoices that are legitimate and accurate”. This means that before a vendor's invoice is entered into the accounting records and scheduled for payment, the invoice must reflect: • what the company had ordered • what the company has received • the proper unit costs, calculations, totals, terms, etc.

Accounts Payable Process The accounts payable process must also be efficient and accurate in order for the company's financial statements to be accurate and complete. Because of double-entry accounting an omission of a vendor invoice will actually cause two accounts to report incorrect amounts. For example, if a repair expense is not recorded in a timely manner: Answer

Accounts Payable Process • the liability will be omitted from the balance sheet, and • the repair expense will be omitted from the income statement. That way your Liability and Expense are understated which overstates your Balance Sheet and Income Statement. Also, If the vendor invoice for a repair is recorded twice, there will be two problems as well: • the liabilities will be overstated, and • repairs expense will be overstated.

Accounts Payable Process In other words, without the accounts payable process being up-to-date and well run, the company's management and other users of the financial statements will be receiving inaccurate feedback on the company's performance and financial position. A poorly run accounts payable process can also mean missing a discount for paying some bills early. If vendor invoices are not paid when they become due, supplier relationships could be strained. This may lead to some vendors demanding cash on delivery.

Accounts Payable Process If that were to occur it could have extreme consequences for a cash-strapped company. Just as delays in paying bills can cause problems, so could paying bills too soon. If vendor invoices are paid earlier than necessary, there may not be cash available to pay some other bills by their due dates. HOME

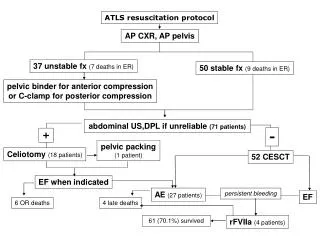

Accounts Payable Flow Chart Every company has their own AP Flow Chart, it depends on the industry or the company’s policies and procedures. Fakih IVF AP Flow Chart: HOME

Documentations Purchase Order A purchase order or PO is prepared by a company to communicate and document precisely what the company is ordering from a vendor. The paper version of a purchase order is a multi-copy form with copies distributed to several people. The people or departments receiving a copy of the PO include: • the person requesting that a PO be issued for the goods or services • the accounts payable department

Documentations • the receiving department • the vendor • the person preparing the purchase order The purchase order will indicate a PO number, date prepared, company name, vendor name, name and phone number of a contact person, a description of the items being purchased, the quantity, unit prices, shipping method, date needed, and other pertinent information.

Documentations One copy of the purchase order will be used in the three-way match, which we will discuss later. Sample PO

Documentations Goods Received Note(GRN)/Receiving Report A receiving report is a company's documentation of the goods it has received. The receiving report may be a paper form or it may be a computer entry. The quantity and description of the goods shown on the receiving report should be compared to the information on the company's purchase order. After the receiving report and purchase order information are reconciled, they need to be compared to the vendor invoice. Hence, the receiving report is the second of the three documents in the three-way match. Sample Zeta GRN

HOME Documentations Vendor Invoice The supplier or vendor will send an invoice to the company that had received the goods and/or services on credit. When the invoice or bill is received, the customer will refer to it as a vendor invoice. Each vendor invoice is routed to accounts payable for processing. After the invoice is verified and approved, the amount will be credited to the company's Accounts Payable account and will also be debited to another account (often as an expense or asset). Sample

Three-way match The accounts payable process often uses a technique known as the three-way match to assure that only valid and accurate vendor invoices are recorded and paid. The three-way match involves the following:

Three-way match Only when the details in the three documents are in agreement will a vendor's invoice be entered into the Accounts Payable account and scheduled for payment. To illustrate the three-way match: Let's assume that BuyerConeeds 10 cartridges of toner for its printers. BuyerCo issues a purchase order to SupplierCorp for 10 cartridges at AED60 per cartridge that are to be delivered in 10 days.

Three-way match PO Distribution: • to SupplierCorp. • to the person requisitioning the cartridges • to the receiving department • to accounts payable • and one copy is retained by the person preparing the PO. When BuyerCo receives the cartridges, a receiving report is prepared.

Three-way match The three-way match involves comparing the following information: • The description, quantity, cost and terms on the company's purchase order. • The description and quantity of goods shown on the receiving report. • The description, quantity, cost, terms, and math on the vendor invoice.

Three-way match After determining that the information reconciles, the vendor invoice can be entered into the liability account “Accounts Payable”. The information entered into the accounting software will include the ff: • invoice reference information (vendor name or code • invoice number and date, etc.) • the amount to be credited to Accounts Payable, the amount(s) and account(s) to be debited • and the date that the payment is to be made.

Three-way match The payment date is based on the terms shown on the invoice and the company's policy for making payments. Lastly, the documents should be stamped or perforated to indicate they have been entered into the accounting system thus avoiding a duplicate payment. HOME

HOME Approvals Fakih IVF-AUH

Internal Controls To safeguard a company's cash and other assets, the accounts payable process should have internal controls. A few reasons for internal controls are to: • prevent paying a fraudulent invoice • prevent paying an inaccurate invoice • prevent paying a vendor invoice twice • be certain that all vendor invoices are accounted for. “Periodically companies should seek professional assistance to improve its internal controls!”

Internal Controls Good internal control of a company's resources is enhanced when the company assigns a separate employee with a specific, limited responsibility. The following chart illustrates the concept of the separation (or segregation) of duties involving accounts payable: When the duties are separated, it will require more than one dishonest person to steal from the company. Hence, small companies without sufficient staff to separate employees' responsibilities will have a greater risk of theft.

Internal Controls In order to protect a company's assets it is important that a company have in place a variety of controls over issuing purchase orders, issuing checks, adding vendors to the accounts payable master vendor file, segregating duties, and other safeguards. It is recommended that a professional who is well-versed in internal controls perform a review of a company's policies and procedures.

Internal Controls Batching the payments to vendors In order for the accounts payable staff to operate efficiently, it is helpful to process the checks written to vendors only on specified days each month. Writing the checks on pre-announced days will hopefully discourage the need for "rush" checks and allow the accounts payable processing to be more efficient. HOME