The Cost Approach

The Cost Approach. Real Estate 614 Real Estate Appraisal Dr. Longhofer. The Cost Approach. Begin by estimating the cost of any improvements on the land Reproduction cost is the cost to construct the building today, replicating it in exact detail

The Cost Approach

E N D

Presentation Transcript

The Cost Approach Real Estate 614 Real Estate Appraisal Dr. Longhofer Real Estate Appraisal

The Cost Approach • Begin by estimating the cost of any improvements on the land • Reproduction cost is the cost to construct the building today, replicating it in exact detail • Replacement cost is the cost required to construct a building of equal utility, using modern construction techniques, materials, and design • Subtract from this the cost of any accrued physical, functional, or external depreciation • Add in the value of the site as raw land to get the indicated value using the cost approach Real Estate Appraisal

Estimating Construction Costs • Comparative-unit Method – For relatively standardized structures, the size of the building is multiplied by the per-square foot cost of that type of construction • Segregated-cost Method – The costs of the individual components in the building are used to estimate the overall replacement cost • Quantity-survey Method – Identifies the exact materials required to reproduce the structure to estimate the cost • Index Method – Assumes that the replacement cost is simply the original construction cost times a cost index Real Estate Appraisal

Categories of Accrued Depreciation • Physical deterioration is the result of wear and tear, weathering from the elements, vandalism and neglect • Functional obsolescence refers to features, design, and other elements of the building that are not up to modern standards; it also includes features in excess of what the market can support (superadequacies) • External (economic) obsolescence refers to loss of value due to influences outside the property Real Estate Appraisal

Estimating Accrued Depreciation • Lump-sum age/life method • Easy to apply • Does not explicitly account for each particular type of depreciation (esp. econ. obsolescence) • Breakdown method • Complex and time consuming to apply • Explicitly considers each type of depreciation • Helps to avoid “double counting” Real Estate Appraisal

Age/Life Method • This method estimates depreciation as a lump sum based on assumed straight-line depreciation • Economic life is estimated using rules of thumb based on past experience or published sources • Effective age is usually used in place of actual age, but this varies Real Estate Appraisal

Age/Life Method Example Reproduction cost new $245,000 Total economic life 55 years Effective age 20 years % accrued depreciation = 20/55 = 36.4% Accrued depreciation 89,180 Depreciated value of improvements 155,820 Land value 39,000 Estimated market value $194,820 Real Estate Appraisal

Modified Age/Life Method • Sometimes the age/life method is modified by subtracting out curable physical and functional depreciation before calculating the lump sum depreciation of the rest • The idea is that the owner will cure these problems because it adds more value than it costs Real Estate Appraisal

Modified Age/Life Method Example Reproduction cost new $245,000 Physical and functional depreciation, curable 12,500 Adjusted cost $232,500 Total economic life 55 years Effective age 17 years % accrued depreciation = 17/55 = 30.9% Accrued depreciation 71,843 Depreciated value of improvements 160,657 Land value 39,000 Estimated market value $199,657 Real Estate Appraisal

Comments on Age/Life Method • The general relationship between age and depreciation varies from market to market • Use local patterns, not national ones • Although this method assumes straight line depreciation, this is not typically accurate • The amount of depreciation changes from year to year • Location of a property within a given market area does not appear to affect depreciation rates Real Estate Appraisal

Comments on Age/Life Method • Effective age (based on subjective appraiser judgment) appears to be more accurate than physical age • Depreciation rates of between 0.70 and 1.25 percent per year seems to be a useful benchmark for properties that are not too old • Depreciation rates can be estimated from comparable sales (market extraction) Real Estate Appraisal

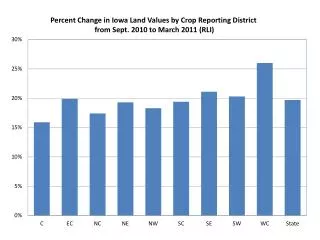

Market Extraction Example Sale price of property $1,520,000 Less: Land value 300,000 Less: Contributing value of site improvements 150,000 Depreciated value of improvements $1,070,000 Reproduction cost of improvements $1,500,000 Less: Depreciated value of improvements 1,070,000 Accrued depreciation $430,000 Depreciation = 430,000 / 1,500,000 = 28.67% Annual depreciation rate (20 years old) 1.43% Real Estate Appraisal

Breakdown Method • In the breakdown method, the physical, functional and external factors contributing to the loss in value of the improvements are isolated and estimated separately • This is particularly important for external obsolescence, which may vary for a property over time Real Estate Appraisal

Categories of Depreciation • Physical deterioration • Curable (deferred maintenance) • Incurable • Short-lived • Long-lived Real Estate Appraisal

Categories of Depreciation • Functional obsolescence • Curable • Deficiencies • Defects • Superadequacies • Incurable • Deficiencies • Defects • Superadequacies Real Estate Appraisal

Categories of Depreciation • External obsolescence • Locational • Economic Real Estate Appraisal

Steps in Breakdown Method • Identify each component cost and total cost new; classify as short- or long-lived • Estimate cost of deferred maintenance (curable physical deterioration) • Estimate cost of curable functional obsolescence • Estimate impact of incurable physical deterioration on short-lived items Real Estate Appraisal

Steps in Breakdown Method • Estimate the impact of long-lived incurable physical deterioration • Estimate cost of incurable functional obsolescence • Estimate the impact of external obsolescence • Add up total depreciation and estimate property value Real Estate Appraisal

Curable Physical Deterioration • The depreciation associated with deferred maintenance is simply the cost of curing the item • Generally, deferred maintenance will apply to short-lived components • In some cases, long-lived components may have deferred maintenance as well; treat these the same way Real Estate Appraisal

Incurable Physical Deterioration of Short-lived Components • For each component, depreciation is calculated using the age/life method based on the effective age and useful life of the component • Make sure you subtract off the cost of deferred maintenance from each component before you calculate depreciation (avoid double counting) Real Estate Appraisal

Incurable Long-lived Physical Deterioration • Use the age/life method to estimate the depreciation due to physical deterioration of the long-lived components • Begin with the total reproduction cost of the improvements • Subtract off the cost of curing deferred maintenance • Subtract off the adjusted cost (after curing deferred maintenance) of short-lived components Real Estate Appraisal

Curable Functional Obsolescence • Deficiencies are items or features that are missing and would be required by the market • The loss from a deficiency is the difference between the cost of installing the item today and what it would have cost to include the item when the building was constructed Real Estate Appraisal

Curable Functional Obsolescence • Defects are items that are present but do not meet modern standards • The loss in value due to a defect is the cost of the item new less the undepreciated cost of the existing item (the part of the cost that has not yet been depreciated) Real Estate Appraisal

Curable Functional Obsolescence • Superadequacies are features or components that exceed modern standards • Excess cost adjustment method – Loss equals the added cost associated with the item less the depreciation already taken • Rent loss method – Loss equals the capitalized difference in NOI between what it would take to support the item compared to market rent, less depreciation already taken Real Estate Appraisal

Incurable Functional Obsolescence • The loss associated with incurable functional obsolescence is calculated using the rent loss method Real Estate Appraisal

Incurable External Obsolescence • This, too, is calculated using the rent loss method, with some modifications • Use the difference between the building’s rent and market rent for comparable properties • No need to subtract off depreciation already taken because external obsolescence relates to factors outside the property • The loss is generally allocated between land and building Real Estate Appraisal

Add Up Total Depreciation and Calculate Market Value Physical deterioration + Incurable short-lived components + Incurable long-lived components + Functional obsolescence + External obsolescence Total depreciation Real Estate Appraisal

Add Up Total Depreciation and Calculate Market Value Reproduction cost new – Total depreciation Depreciated value of improvements + Contributing value of site improvements + Land value Value indication from cost approach Real Estate Appraisal