BALANCED SCORECARD

BALANCED SCORECARD. Contents. Introduction about BSC Four perspectives Financial Customer Internal business Learning and growth Evaluation of BSC Cause and effect relationship Performance drivers. Diagnostic V/S Strategic measures Sufficiency of perspectives

BALANCED SCORECARD

E N D

Presentation Transcript

Contents Introduction about BSC Four perspectives Financial Customer Internal business Learning and growth Evaluation of BSC Cause and effect relationship Performance drivers

Diagnostic V/S Strategic measures Sufficiency of perspectives Strategic balance scorecard Implementation of SBSC Problems faced Conclusion

INTRODUCTION The Balanced Scorecard Approach has been developed at the Harvard Business School by Kaplan and Norton in 1992 in an article by Robert Kaplan and David Norton entitled "The Balanced Scorecard - Measures that Drive Performance” Due to the shortcomings of traditional management control systems, Kaplan and Norton designed the BSC as a result of a one year research project with 12 companies.

It works on the principle of “Management By Objective” It was developed to communicate the multiple, linked objectives that companies must achieve . It translates mission and strategy into objectives and measures.

This innovative tool is unique in two ways compared to the traditional performance measurement tools. They are– It considers the financial indices as well the non-financial ones in determining the corporate performance level. It is not just a performance measurement tool but is also a performance enhancing tool.

The framework tries to bring a balance and linkage between the : Financial and the Non-Financial indicators Tangible and the Intangible measures Internal and the External aspects Leading and the Lagging indicators.

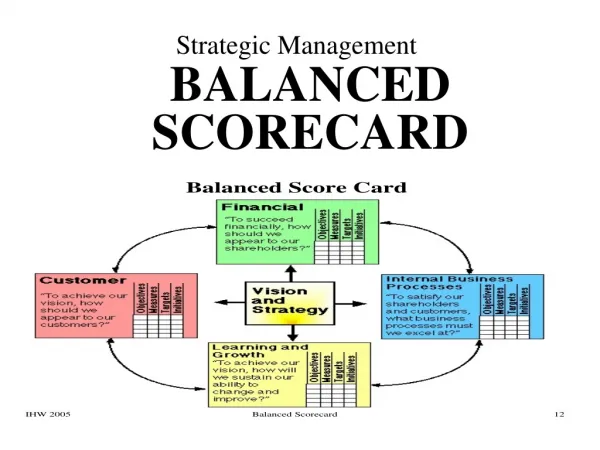

Clarifying and Translating • the Vision and Strategy • Clarifying the vision • Gaining consensus Balanced Scorecard • Communicating and Linking • Communicating and educating • Setting goals • Linking rewards to performance • measures • Strategic Feedback and • Learning • Articulating the shared vision • Supplying strategic feedback • Facilitating strategy review and • learning • Planning and Target Setting • Setting targets • Aligning strategic initiatives • Allocating resources • Establishing milestones

It is organized into 4 perspectives:- Financial Perspective - How do we look at shareholders? 2. Customer Perspective - How should we appear to our customers? 3. Internal Business Processes Perspective - What must we excel at? 4. Learning and Growth Perspective - Can we continue to improve and create value?

Objectives, Measures, Targets, and Initiatives Objectives: Major objectives to be achieved, for example, profitable growth. Measures: The observable parameters that will be used to measure progress toward reaching the objective. For example, the objective of profitable growth might be measured by growth in net margin. Targets: The specific target values for the measures. For example, 7% annual decline in manufacturing disruptions. Initiatives: Projects or programs to be initiated in order to meet the objective.

Financial perspective Kaplan and Norton do not disregard the traditional need for financial data. It indicates wheather the company strategy, implementation and execution are contributing to bottom line improvement. Financial objectives are typically related to Profitability, Rapid sales growth, Generation of cash flows.

For different stages there are different objectives and measures: Growth: Increased sales volumes, acquisition of new customers, growth in revenues etc. Sustain: Calculating the return on investment, the return on capital employed, etc. Harvest: Payback periods and revenue volume

Customer perspectives Managers identify the customer and market segments in which business unit will compete and measures of the business unit’s performance in these segments. It includes various core or generic measures of the successful outcomes from a well formulated and implemented strategy

Core measures: Customer satisfaction Customer retention New customer acquisition Customer profitability Market and account share

Strategy becomes unique due to value proposition the business unit decides to deliver to attract customers. Common set of attributes that organizes the value proposition are Product and services attributes Customer relationship Image and reputation

Customer perspective Net share Customer Acquisition Customer Retentions Customer Satisfaction Customer Profitability

Internal business process perspective This perspective show the managers how well their business is running, and whether its products and services conform to customer requirements. Executives identify the critical internal processes in which organization must excel. It enables the business unit to: Deliver value proposition Satisfy shareholders expectations of excellent financial returns.

Two kinds of business processes may be identified: Mission-oriented processes. Unique ; problems are encountered in these processes. Support processes. The support processes are more repetitive in nature, and hence easier to measure and to benchmark. Generic measurement methods can be used.

Each business unit has its unique set for creating value for customers. Generic value chain model encompasses 3 principal business process: Innovation Operations Postal services

Learning and growth perspective Identifies the infrastructure that the organization must build to create long term growth and improvement. Organizational learning and growth come from 3 principal sources People System Organizational procedures

Key performance indicators Financial Cash flows ROI Financial result Return on capital employed Return on equity Customer Customer satisfaction rate Customer retention rate Delivery performance to customers

Internal business process Number of activities Opportunity success rate Accidental ratios Defect rates Learning and growth Investment rate Illness rate Employee turnover Gender ratio

EVALUATION OF BALANCE SCORECARD ADVANTAGES It aligns everyone within an organization so that all employees understand how they support the strategy. It provides a basis for compensation for performance. It translates vision and strategy into action.

It defines the strategic linkages to integrate performance across organizations. It communicates the objectives and measures to a business unit. It aligns the strategic initiatives in order to attain the long-term goals. The scorecard provides a feedback to the senior management if the strategy is working

Linking multiple scorecards measures to a single strategy Multiple measures should consist of a linked series of objectives and measures that should be consistent and mutually reinforcing. It should be viewed as the instrumentation for a single strategy. It should incorporate the complex set of cause and effect relationships among the critical variables.

Cause and Effect Relationships Return on capital employed Customer loyalty On-time delivery Process quality process cycle time Employee skills

Properly constructed balance scorecard should tell the story of the business unit’s strategy. It should identify and make explicit the sequence of hypotheses about the cause and effect relationship between outcome measures and performance drivers of those outcomes.

Performance drivers BSC should have a mix of outcome measures and performance drivers. Scorecard translates the business unit’s strategy into a linked set of measures that define both long term strategic objectives and the mechanism for achieving those objectives.

Diagnostic V/S Strategic measures Diagnostic measures It monitors whether the business remains “in control” and signal unusual events. Strategic measures It defines a strategy designed for competitive excellence and future success.

Diagnostic measures capture vital signs that enable the company to operate but are not basis for competitive breakthrough. Measures of BSC are chosen to direct managers and employee to those factors for which superb performance can be expected. It is subject to extensive and intensive interaction among top and middle level managers

Are 4 perspective sufficient? They should be considered a template, not a straitjacket. No mathematical theorem exists that 4 perspective are both necessary and sufficient. Use depend upon industry circumstances and business unit’s strategy.

Some people have concern that these perspective consider only shareholders and customer perspective Interest of shareholders through financial perspective and customer through customer perspective. Measures for employee, suppliers and community appear on BSC when there outstanding performance lead to breakthrough performance.

In recent years many corporations have implemented environmental and/or social management systems (such as ISO 14000, EMAS or SA 8000) in order to manage and control sustainability-related issues. These management systems often fall short in companies’ practice for two reasons. Management systems are run on the operating level Management systems are mostly executed separately from the traditional general management systems

These two problems of sustainability management have been the motivation for a qualitative research project at the Institute for Economy and the Environment at the University of St. Gallen. In the project, the management tool and methodology of the traditional Balanced Scorecard (Kaplan & Norton1997) have been developed further towards the „Sustainability Balanced Scorecard“ (SBSC) integrating ecological, social as well as economic aspects. The co-operation with six companies has made it possible to gather valuable experiences when developing and implementing a SBSC.

Concept of SBSC The SBSC-concept is based on the “traditional” Balanced Scorecard (BSC). In SBSC fifth perspective is included in order to explicitly address stakeholders issues. The SBSC may help to detect important strategic environmental and/or social objectives of the company, a single SBU or department and to illustrate causal relationships between qualitative “soft facts” and the financial performance.

Implementing SBSC In implementing a SBSC strategic, cultural, structural as well as methodological aspects seem to be most relevant. Define suitable strategies within a strategic planning process. From there, strategic goals, key performance indicators as well as appropriate measures can be deduce Corporate culture should be considered .

Sustainability-oriented competitivestrategies Visions, strategies and concrete objectives are difficult to link to each other because of following reasons: Strategies do not exist at all or are at least not explicit. The strategies are very similar to visions which are rather broad and not understood by employees. Lack of support from the strategic development department.

Economy and the Environment at the University of St. Gallen over the past decade, revealed an empirical body of evidence that sustainability strategies can be classified according to their strategic orientation (market or society) and strategic behavior (reactive or proactive) Strategy “safe” aims at reducing and managing risks. Strategies of the type “credible” are tackling issues of image and reputation.

The improvement of productivity and efficiency is possible by implementing the strategy type “efficient”. The “innovative” strategy aims at differentiating corporation’s products and services in the market. “Transformative” strategies aim at creating new markets by shifting existing institutional frameworks.

Prashant Desai, senior manager-knowledge management, Pantaloon Retail India Ltd said that pay per performance had a lot of subjectivity and the focus was only on rewarding the employees if he/she met the financial targets. “The crux is to capture the health of the company holistically taking all parameters into consideration. Therefore the balanced score card factors in all considerations which go on to measure the employees performance,” said Mr Desai. He added that the Balanced score card aimed at moving into variable pay or bonuses on the basis of the company’s performance.

Conclusion “The application of this tool ensures the consistency of vision and action which is the first step towards the development of a successful organization. However, it is not easy to implement this tool because it involves a lot of subjectivity.”