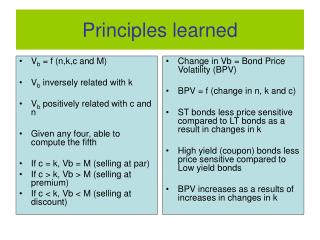

Principles learned

This article explores the relationships between bond price volatility (Vb) and various factors including yield (k), coupon rate (c), and time to maturity (n). It details how Vb is inversely related to k, while it positively correlates with c and n. By understanding these dynamics, one can compute the fifth element when given any four variables. The document explains scenarios for bonds selling at par, premium, or discount based on the relationships between these factors, highlighting the sensitivity of short versus long-term bonds and their yield characteristics.

Principles learned

E N D

Presentation Transcript

Vb = f (n,k,c and M) Vb inversely related with k Vb positively related with c and n Given any four, able to compute the fifth If c = k, Vb = M (selling at par) If c > k, Vb > M (selling at premium) If c < k, Vb < M (selling at discount) Change in Vb = Bond Price Volatility (BPV) BPV = f (change in n, k and c) ST bonds less price sensitive compared to LT bonds as a result in changes in k High yield (coupon) bonds less price sensitive compared to Low yield bonds BPV increases as a results of increases in changes in k Principles learned