less

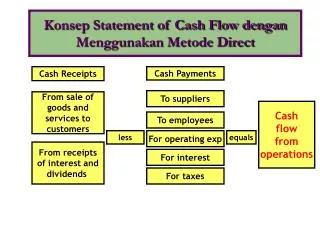

Cash Receipts. Cash Payments. From sale of goods and services to customers. To suppliers. To employees. For operating exp. From receipts of interest and dividends . For interest. For taxes. Konsep Statement of Cash Flow dengan Menggunakan Metode Direct. Cash flow from operations.

less

E N D

Presentation Transcript

Cash Receipts Cash Payments From sale of goods and services to customers To suppliers To employees For operating exp From receipts of interest and dividends For interest For taxes Konsep Statement of Cash Flow dengan Menggunakan Metode Direct Cash flow from operations less equals

Contoh Penyusunan Statement of Cash Flows Berikut adalah Laporan Keuangan PT Surya Citra Media Tbk selama tahun 2005 – 2004 sebagai berikut : PT Surya Citra Media Tbk Comparative Balance Sheet As of December 31, 2005 and 2004 20052004 Cash $ 1,800 $ 1,150 Receivables $ 1,750 $ 1,300 Inventory $ 1,600 $ 1,900 Plant assets $ 1,900 $ 1,700 Accumulated depreciation $ (1,200) $ (1,170) Long term investments (held to maturity) $ 1,300$ 1,420 $ 7,150$ 6,300 Accounts payable $ 1,200 $ 900 Accrued liabilities $ 200 $ 250 Bonds payable $ 1,400 $ 1,550 Capital stock $ 1,900 $ 1,700 Retained earnings $ 2,450$ 1,900 $ 7,150$ 6,300

Contoh Penyusunan Statement of Cash Flows PT Surya Citra Media Tbk Income Statement For the year ended December 31, 2005 Sales $ 6,900 Cost of goods sold _ 4,700 Gross margin $ 2,200 Selling and administrative expense 930 Income from operations 1,270 Gain on sale of investments _ 80 Income before tax $ 1,350 Income tax expense _ 540 Net income $ 810 Cash dividends _ 260 Income retained in business $ 500 Informasi Tambahan : Selama tahun berjalan perusahaan menerbitkan Common Stock dengan nilai $ 70. Common stock tsb diterbitkan untuk membeli Plant Asset. Selama tahun 2005 tidak ada Plant Asset yang dijual. Diminta : Susun Statement of Cash Flows dengan menggunakan Metode Direct.

Perhitungan Cash Receipt From Customer Cash receipts from customers: = Revenue from credit sales + Decrease in A/Rec balances - Increase in A/Rec balances Dengan menggunakan rumus diatas, kita dapat menghitung cash receipts from customer sbb : Revenue from credit sales 6,900 Account Receivable Dec 31, 2004 1,300 Account Receivable Dec 31, 2005 1,750 + Increase A/R _450 - Cash Receipt from customer 6,450 (a)

Perhitungan Cash Payments to Suppliers Cash payments to suppliers: = Cost of goods sold + Increase in inventory - Decrease in inventory + Decrease in accounts payable - Increase in accounts payable Dengan menggunakan rumus diatas, kita dapat menghitung cash payments to suppliers sbb : Cost of goods sold 4,700 Inventory Dec 31, 2004 1,900 Inventory Dec 31, 2005 1,600 + Decrease in Inventory _300 - Account Payable Dec 31, 2004 900 Account Payable Dec 31, 2005 1,200 + Increase in Account Payable _300 - Cash payments to suppliers 4,100 (b)

Perhitungan Cash Payment for Operating Cash payments for operating and other expenses: = Operating expenses + Increase in prepaid expenses - Decrease in prepaid expenses + Decrease in accrued expenses payable - Increase in accrued expenses payable Dengan menggunakan rumus diatas, kita dapat menghitung cash payments for operating and other expenses sbb : Operating expenses 900 Selling & administrative expense Selling administrative expense sebesar $ 930 sudah termasuk beban depreciation expense yang merupakan non cash. Sehingga depreciation expense harus dikurangi dari saldo tsb. Depreciation expense dapat dihitung dari perubahan saldo Accumulated depreciation. Jadi selling & administrative expense yang merupakan cash adalah $ 930 – (1,200 – 1,170) = 900 Accrued Liabilities Dec 31, 2004 250 Accrued Liabilities Dec 31, 2005 200 - Decrease in Accrued Liabilities _50 + Cash payments for operating and other expenses 950 (c)

From sales of goods or services From returns on loans (interest) and returns on equity securities (dividends) To suppliers for inventory To employees for services To government for taxes To lenders for interest To others for expenses Perhitungan Cash Payment Untuk Pajak Inflows Outflows Dari laporan Income Statement diketahui adanya pembayaran pajak kepada pemerintah (income tax expense) sebesar $ 540 (d)

Perhitungan Investing Activities Untuk menghitung Net Cash Flow dari Investing Activities, kita harus memperhatikan perubahan pada Fixed Asset. 20052004PerubahanCash Plant Assets 1,900 1,700 Naik 200 (130) Long Term Investment 1,300 1,420 Turun 120 200 Cash in flows (e) 70 Dari tambahan informasi dijelaskan bahwa perusahaan menerbitkan Common Stock sebesar $ 70 untuk membeli Plant Asset, dengan demikian cash yang digunakan untuk pembelian Plant Asset adalah sebesar $ 1,900 - $ 1,700 - $ 70 = $ 130. Selama tahun 2005, perusahaan melakukan penjualan Long Term Investment dengan mendapatkan Gain sebesar $ 80, dengan demikian cash yang diterima dari penjualan Long Term Investment adalah sebesar $ 1,420 - $ 1,300 + $ 80 = $ 200.

Perhitungan Financing Activities Untuk menghitung Net Cash Flow dari Financing Activities, kita harus memperhatikan perubahan pada Long Term Liabilities dan Owner’s Equity. 20052004PerubahanCash Bonds Payable 1,400 1,550 Turun 150 (150) Capital Stock 1,900 1,700 Naik 200 130 Retained Earnings 2,450 1,900 Naik 550 (260) Cash out flows (f) (280) Dari tambahan informasi dijelaskan bahwa perusahaan menerbitkan Common Stock sebesar $ 70 untuk membeli Plant Asset, dengan demikian cash yang diterima dari penerbitan Common Stock adalah sebesar $ 1,900 - $ 1,700 - $ 70 = $ 130. Dari Laporan Income Statement diperoleh informasi bahwa Cash Dividend yang dibayarkan adalah sebesar $ 260 dan tambahan Retained Earning dari Net Income adalah sebesar $ 550, dengan demikian kenaikan saldo Retained Earnings sebesar $ 550 seluruhnya berasal dari Net Income.

Format Statement of Cash Flows dengan menggunakan Metode Direct Cash flows from operating activities: Cash receipts (individually): Inflows $ XXX Cash payments to suppliers (separately): outflows ($ XXX) Net cash flow from operating activities $ XXX Cash flows from investing activities: (List of individual inflows and outflows) $ XX Net cash flow from investing activities $ XXX Cash flows from financing activities: (List of individual inflows and outflows) $ XX Net cash flow from financing activities $ XXX

Penyusunan Statement of Cash Flow Dengan Menggunakan Metode Direct PT Surya Citra Media Tbk Statement Of Cash Flows For the Year Ended December 31, 2005 Cash Flows From Operating Activities Cash receipts from customers $ 6,450 (a) Cash payments to suppliers $ (4,100) (b) Cash payments for operating & other expenses $ ( 950) (c) Cash paid for income taxes $ ( 540)(d) Net cash provided by operating activities $ 860 Cash flows from investing activities Sale of held-to-maturity investments $ 200 Purchase of plant assets $ (130) Net cash provided by investing activities (e) $ 70 Cash flows from financing activities Issuance of capital stock $ 130 Retirement of bonds payable $ (150) Payment of cash dividends $ (260) Net cash used by financing activities (f) $ (280) Net increase in cash $ 650 Cash, January 1, 2005 $ 1,150 Cash, December 31, 2005 $ 1,800 Non-cash investing and financing activities Issuance of common stock for plant assets $ 70

Perbedaan Metode Direct Dengan Metode Indirect • Perbedaan antara Metode Direct dengan Metode Indirect ada pada komponen Cash Flow From Operating Activities. • Apabila menggunakan Metode Indirect, diperlukan penyesuaian terhadap Net Income karena saldo Net Income tsb termasuk komponen yang bukan cash (bukan out of pocket cost) seperti Depreciation Expense, Amortization Expense, Depletion Expense. • Selain itu, Net Cash Flow From Operating Activities juga dipengaruhi oleh perubahan pada Current Asset dan Current Liabilities

Format Statement of Cash Flows Dengan Menggunakan Metode Indirect Cash flows from operating activities: Net Income $ XXX Adjustments (to arrive at cash flow from operations) $ XX (List of individual inflows and outflows) Net cash flow from operating activities $ XXX Cash flows from investing activities: (List of individual inflows and outflows) $ XX Net cash flow from investing activities $ XXX Cash flows from financing activities: (List of individual inflows and outflows) $ XX Net cash flow from financing activities $ XXX

Penyusunan Statement of Cash Flow Dengan Menggunakan Metode Indirect PT Surya Citra Media Tbk Statement Of Cash Flows For the Year Ended December 31, 2005 Cash Flows From Operating Activities Net income $ 810 Adjustments to reconcile by operating activities: Depreciation expenses ($ 1,200 – $ 1,170) $ 30 Gain on sale of investments $ (80) Decrease in inventory $ 300 Increase in accounts payable $ 300 Increase in receivables $ (450) Decrease in accrued liabilities $ (50) 50 Net cash provided by operating activities $ 860 Cash flows from investing activities Sale of held-to-maturity investments $ 200 Purchase of plant assets $ (130) Net cash provided by investing activities (e) $ 70 Cash flows from financing activities Issuance of capital stock $ 130 Retirement of bonds payable $ (150) Payment of cash dividends $ (260) Net cash used by financing activities (f) $ (280) Net increase in cash $ 650 Cash, January 1, 2005 $ 1,150 Cash, December 31, 2005 $ 1,800 Non-cash investing and financing activities Issuance of common stock for plant assets $ 70