Financial Analysis and Investment Decision Making Tutorial

This tutorial provides solutions to homework problems involving cash flows, operating and terminal values, salvage, depreciation adjustments, and profitability index for investment decisions.

Financial Analysis and Investment Decision Making Tutorial

E N D

Presentation Transcript

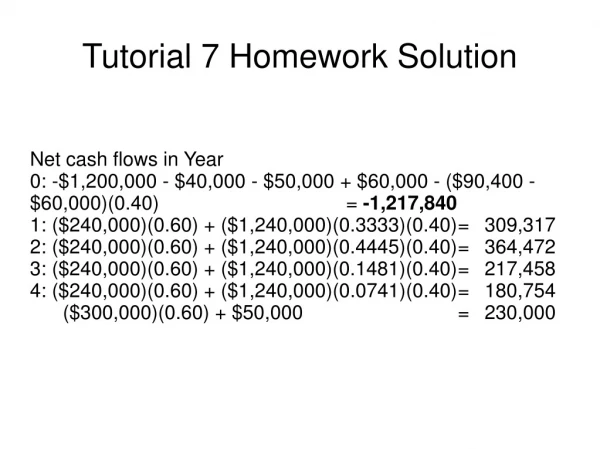

Net cash flows in Year 0: -$1,200,000 - $40,000 - $50,000 + $60,000 - ($90,400 - $60,000)(0.40) = -1,217,840 1: ($240,000)(0.60) + ($1,240,000)(0.3333)(0.40) = 309,317 2: ($240,000)(0.60) + ($1,240,000)(0.4445)(0.40) = 364,472 3: ($240,000)(0.60) + ($1,240,000)(0.1481)(0.40) = 217,458 4: ($240,000)(0.60) + ($1,240,000)(0.0741)(0.40) = 180,754 ($300,000)(0.60) + $50,000 = 230,000 Tutorial 7 Homework Solution

Initial CF • Cost -1,200,000 • Installation -40,000 • NWC inc. -50,000 • Sale old asset +60,000 • Dep,n (90,400 – 60,000)(0.40) = +12,160 • - 1,217,840

Operating CF 1: ($240,000)(0.60) + ($1,240,000)(0.3333)(0.40) = 309,317 2: ($240,000)(0.60) + ($1,240,000)(0.4445)(0.40) = 364,472 3: ($240,000)(0.60) + ($1,240,000)(0.1481)(0.40) = 217,458 4: ($240,000)(0.60) + ($1,240,000)(0.0741)(0.40) = 180,754 Terminal CF Salvage value 300,000 x 0.6 = 180,000 NWC recovered = 50,000

Notes: • Salvage value is the amount the “new” asset can be sold for less tax because asset is fully written down for depreciation purposes • Depreciable value of the new asset is $1,240,000 (1,200,000 + 40,000) • Depreciation on old asset in its final year was $90,400, but the asset was worth just $60,000. Therefore there is a tax adjustment needed for the loss of $30,400 (i.e. 90,400 – 60,000)

Text book Ch 12, problem # 3 (p.320) • Period Rockbuilt Bulldog Savings Bulldog truck • 0 ($74,000) ($59,000) ($15,000) • 1 (2,000) (3,000) 1,000 • 2 (2,000) (4,500) 2,500 • 3 (2,000) (6,000) 4,000 • 4 (2,000) (22,500) 20,500 • 5 (13,000) (9,000) (4,000) • 6 (4,000) (10,500) 6,500 • 7 (4,000) (12,000) 8,000 • 8 5,000* (8,500)** 13,500 • * $4,000 maintenance cost plus salvage value of $9,000. • ** $13,500 maintenance cost plus salvage value of $5,000.

Tutorial 8 • 4. The Cardinal Machine Tool Company is considering the purchase of a new drill press to replace the one currently being used. • The present machine should last another seven years and have no salvage value. • The current drill press has a book value of $700 and can be sold for $400. • Cardinal pays $300 a year maintenance on the press. • The new drill press will cost $1,500 and is expected to last seven years, at which time it will be sold for $100. • The maintenance cost of the new machine is expected to be $150 a year. • Cardinal depreciates its assets on the straight-line basis and pays 40% taxes. • If its opportunity cost of funds is 10%, should it buy the new machine?

Initial cost = $1,500 - $400 + ($700 - $400)(0.40) = $980 • Annual savings after tax = ($300 - $150)(0.60) = $90 • Change in depn = ($1,500 - $100)/7 - $700/7 = $100 per yr • Tax saving on depn change = ($100)(0.40) = $40 • NPV at 10%: • = ($90 + $40)(4.868) + ($100)(0.513) - $980 = -$295.86 • Since the NPV is negative, we would REJECT this project.

Text book Ch 13, problem # 8 (p.348) • Selecting those projects with the highest profitability index values would indicate the following: • Project Amount PI NPV* • 1 $500,000 1.22 $110,000 • 3 350,000 1.20 70,000 • $850,000 $180,000 • * NPV = (Amount x PI) - Amount • = (500,000 x 1.22) – 500,000 = 110,000

However, utilising “close to” full budgeting will be better. • Project Amount PI NPV • 1 $500,000 1.22 $110,000 • 4 450,000 1.18 81,000 • $950,000 $191,000

b. No. The resort should accept all projects with a positive NPV. If capital is not available to finance them at the discount rate used, a higher discount rate should be used, which more adequately reflects the costs of financing.