Comprehensive Course on PDE and Numerical Methods for Financial Engineering

This course employs an incremental approach to build on existing knowledge of Partial Differential Equations (PDE) and numerical methods. The structure includes five blocks covering the basics of PDE, finite difference methods (FDM) for one-factor and two-factor Black-Scholes models, and advanced issues such as approximating Greeks and parabolic variational inequalities. Students will learn algorithm implementation, performance evaluation, and integration with Excel, culminating in a deep understanding of both theoretical and practical aspects of numerical solutions in financial engineering.

Comprehensive Course on PDE and Numerical Methods for Financial Engineering

E N D

Presentation Transcript

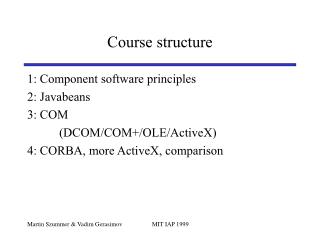

Structure of Course • Incremental approach • Build on expertise already gained • Start with model problems; understand thoroughly • Generalise to more advanced and difficult problems

Course Buildup • Block 1: Basics of PDE and numerical methods • Block 2: FDM for one-factor Black-Scholes PDE model • Block 3: FDM for two-factor models • Block 4: Advanced issues • Block 5: Algorithms

Block 1 • Classification of options and PDE • Motivating FDM for ODE and SDE • Method of Lines • Standard difference schemes for Black Scholes

Block 2 • Special schemes for special problems • Approximating the Greeks • Comparing FDM with binomial and trinomial methods • How good are our schemes?

Block 3 • ADI and splitting method for two-factor models • Stability and convergence • Applications in financial engineering • Comparisons with other methods

Block 4 • An introduction to parabolic variational inequalities (PVI) • Numerical solution of PVI • An introduction to spectral methods • An introduction to Finite Element Method (FEM)

Block 5 • Algorithms and documentation • Mapping algorithms to code • Performance • Coupling with Excel