What is GST ??

E N D

Presentation Transcript

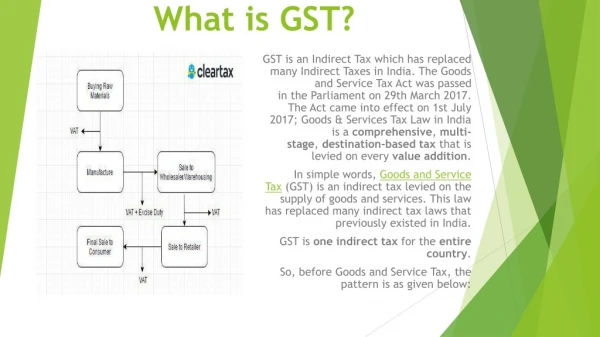

What is GST? GST is an Indirect Tax which has replaced many Indirect Taxes in India. The Goods and Service Tax Act was passed in the Parliament on 29th March 2017. The Act came into effect on 1st July 2017; Goods & Services Tax Law in India is a comprehensive, multi-stage, destination-based tax that is levied on every value addition. In simple words, Goods and Service Tax (GST) is an indirect tax levied on the supply of goods and services. This law has replaced many indirect tax laws that previously existed in India. GST is one indirect tax for the entire country. So, before Goods and Service Tax, the pattern is as given below:

Journey of GST in India The GST journey began in the year 2000 when a committee was set up to draft law. It took 17 years from then for the Law to evolve. In 2017 the GST Bill was passed in the LokSabha and RajyaSabha. On 1st July 2017 the GST Law came into force.

Advantages Of GST • GST has mainly removed the Cascading effect on the sale of goods and services. Removal of cascading effect has impacted the cost of goods. Since the GST regime eliminates the tax on tax, the cost of goods decreases. GST is also mainly technologically driven. All activities like registration, return filing, application for refund and response to notice needs to be done online on the GST Portal; this accelerates the processes.

What are the components of GST? • There are 3 taxes applicable under this system: CGST, SGST & IGST. • CGST: Collected by the Central Government on an intra-state sale (Eg: transaction happening within Maharashtra) • SGST: Collected by the State Government on an intra-state sale (Eg: transaction happening within Maharashtra) • IGST: Collected by the Central Government for inter-state sale (Eg: Maharashtra to Tamil Nadu) • Illustration: • Let us assume that a dealer in Gujarat had sold the goods to a dealer in Punjab worth Rs. 50,000. The tax rate is 18% comprising of only IGST. • In such case, the dealer has to charge Rs. 9,000 as IGST. This revenue will go to the Central Government.The same dealer sells goods to a consumer in Gujarat worth Rs. 50,000. The GST rate on the good is 12%. This rate comprises of CGST at 6% and SGST at 6%. • The dealer has to collect Rs. 6,000 as Goods and Service Tax. Rs. 3,000 will go to the Central Government and Rs. 3,000 will go to the Gujarat government as the sale is within the state.

Tax Laws before GST • In the earlier indirect tax regime, there were many indirect taxes levied by both state and centre. States mainly collected taxes in the form of Value Added Tax (VAT). Every state had a different set of rules and regulations. Interstate sale of goods was taxed by the Centre. CST (Central State Tax) was applicable in case of interstate sale of goods. Other than above there were many indirect taxes like entertainment tax, octroi and local tax that was levied by state and centre. This led to a lot of overlapping of taxes levied by both state and centre. For example, when goods were manufactured and sold, excise duty was charged by the centre. Over and above Excise Duty, VAT was also charged by the State. This lead to a tax on tax also known as the cascading effect of taxes. The following is the list of indirect taxes in the pre-GST regime:Central Excise Duty • Duties of Excise • Additional Duties of Excise • Additional Duties of Customs • Special Additional Duty of Customs • Cess • State VAT • Central Sales Tax • Purchase Tax • Luxury Tax • Entertainment Tax • Entry Tax • Taxes on advertisements • Taxes on lotteries, betting, and gambling

What is GST Registration • In the GST Regime, businesses whose turnover exceeds Rs. 40 lakhs* (Rs 10 lakhs for NE and hill states) is required to register as a normal taxable person. This process of registration is called GST registration. • For certain businesses, registration under GST is mandatory. If the organization carries on business without registering under GST, it will be an offence under GST and heavy penalties will apply. • GST registration usually takes between 2-6 working days. We’ll help you to register for GST in 3 easy steps. • *CBIC has notified the increase in threshold turnover from Rs 20 lakhs to Rs 40 lakhs. The notification has come into effect from 1st April 2019

Who Should Register for GST? • Individuals registered under the Pre-GST law (i.e., Excise, VAT, Service Tax etc.) • Businesses with turnover above the threshold limit of Rs. 40 Lakhs* (Rs. 10 Lakhs for North-Eastern States, J&K, Himachal Pradesh and Uttarakhand) • Casual taxable person / Non-Resident taxable person • Agents of a supplier & Input service distributor • Those paying tax under the reverse charge mechanism • Person who supplies via e-commerce aggregator • Every e-commerce aggregator • Person supplying online information and database access or retrieval services from a place outside India to a person in India, other than a registered taxable person • *CBIC has notified the increase in threshold turnover from Rs 20 lakhs to Rs 40 lakhs.

Documents Required for GST Registration • PAN of the Applicant • Aadhaar card • Proof of business registration or Incorporation certificate • Identity and Address proof of Promoters/Director with Photographs • Address proof of the place of business • Bank Account statement/Cancelled cheque • Digital Signature • Letter of Authorization/Board Resolution for Authorized Signatory

GST Registration Process • The GST Registration looks like this: • The applicant needs to submit his PAN, Mobile number and E-mail address in Part Aof Form GST REG-01 on GSTN Portal. • The PAN is then verified on the GSTN Portal while the Mobile number and the E-mail address are verified through an OTP (One-time-password). An acknowledgment will be issued to the applicant in the Form GST REG-02. • The Applicant then needs to fill the Part B of Form GST REG-01 and specify the application reference number. The form can be submitted after attaching the required documents. The authentication would be done by signature through DSC or E-Signature. • If any additional information is required, Form GST REG-03 will be issued. The Applicant needs to respond in Form GST REG-04 with the required information within 7 working days from the date of the receipt of Form GST REG-03. • If applicant has provided all the required information via Form GST REG-01 or Form GST REG-04, the registration certificate in Form GST REG-06 for the principal place of the business as well as for every additional place of business will be issued. If, however, the details submitted are not satisfactorily, the registration application will be rejected using Form GST REG-05. • The applicant who is required to deduct TDS or collect TCS shall, however, submit an application in Form GST REG-07 for the purpose of registration.

Penalty for not registering under GST • An offender not paying tax or making short payments (genuine errors) has to pay a penalty of 10% of the tax amount due subject to a minimum of Rs.10,000. • The penalty will at 100% of the tax amount due when the offender has deliberately evaded paying taxes