Accounting in Action

Accounting in Action. Lecture Objectives:. State the accounting equation and define each element of the equation Explain how business transactions can be stated in terms of the resulting change in the basic elements of the accounting equation.

Accounting in Action

E N D

Presentation Transcript

Lecture Objectives: State the accounting equation and define each element of the equation Explain how business transactions can be stated in terms of the resulting change in the basic elements of the accounting equation. Describe the financial statements of a proprietorship and explain how they interrelate.

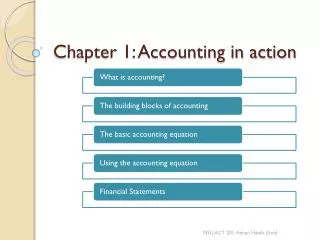

Accounting in Action What is Accounting? The Building Blocks of Accounting The Basic Accounting Equation Using the Basic Accounting Equation Financial Statements Three activities Who uses accounting data Ethics in financial reporting Generally accepted accounting principles Assumptions Assets Liabilities Owner’s equity Transaction analysis Summary of transactions Income statement Owner’s equity statement Balance sheet Statement of cash flows

The Elements of Accounting Assets Liabilities Owner’ Equity (Capital) Revenues Expenses

The Accounting Equation Assets = Liabilities + Owner’s Equity The resources owned and controlled by a business entity

The Accounting Equation Assets = Liabilities + Owner’s Equity The rights of the creditors, which represent debts of the business

The Accounting Equation Assets = Liabilities + Owner’s Equity The rights of the owners

What is a business transaction? A business transaction is an economic event or condition that directly changes an entity’s financial condition or directly affects its results of operations.

On November 1, 2005, Chris Clark begins a business that will be known as NetSolutions.

Assets Owner’s Equity = Chris Clark, Capital 25,000 Investment by Chris Clark Cash 25,000 = a. • Chris Clark deposits P25,000 in a bank account in the name of NetSolutions.

Bal. 5,000 20,000 25,000 • NetSolutions bought land, P20,000 for cash Assets Owner’s Equity = Chris Clark, Capital 25,000 Cash + Land 25,000 Bal. = b. (20,000) +20,000

Bal. 5,000 1,350 20,000 1,350 25,000 • During the month, NetSolutions purchased supplies for P1,350 and agreed to pay the supplier in the near future (on account). Owner’s Liabilities + Equity Assets = Accounts Chris Clark, Cash + Supplies + Land Payable Capital = Bal. 5,000 20,000 25,000 c. 1,350 1,350

Bal. 12,500 1,350 20,000 1,350 32,500 • NetSolutions provided services to customers, earning fees of P7,500 and received the amount in cash. Owner’s Liabilities + Equity Assets = Accounts Chris Clark, Cash + Supplies + Land Payable Capital Bal. 5,000 1,350 20,000 1,350 25,000 = Fees earned d. 7,500 7,500

e. ( 3,650) (2,125) ( 800) ( 450) ( 275) Wages Rent Util. Misc. • Bal. 8,850 1,350 20,000 1,350 28,850 • NetSolutions paid the following expenses: wages-P2,125; rent-P800; utilities-P450; and miscellaneous-P275. Owner’s Liabilities + Equity Assets = Accounts Chris Clark, Cash + Supplies + Land Payable Capital Bal. 12,500 1,350 20,000 1,350 32,500 =

Bal. 7,900 1,350 20,000 400 28,850 • NetSolutions paid P950 to creditors during the month. Owner’s Liabilities + Equity Assets = Accounts Chris Clark, Cash + Supplies + Land Payable Capital = Bal. 8,850 1,350 20,000 1,350 28,850 f. ( 950) ( 950)

Bal. 7,900 550 20,000 400 28,050 • At the end of the month, the cost of supplies on hand is P550, so P800 of supplies were used. Owner’s Liabilities + Equity Assets = Accounts Chris Clark, Cash + Supplies + Land Payable Capital = Bal. 7,900 1,350 20,000 400 28,850 Supplies expense g.( 800) ( 800)

Bal. 5,900 550 20,000 400 26,050 • At the end of the month, Chris withdrew P2,000 in cash from the business for personal use. Owner’s Liabilities + Equity Assets = Accounts Chris Clark, Cash + Supplies + Land Payable Capital = Bal. 7,900 550 20,000 400 28,050 With-drawal h.(2,000) (2,000)

Decreased by Increased by Owner’s withdrawals Expenses Owner’s investments Revenues Net income Effects of Transactions on Owner’s Equity Owner’s Equity

Accounting reports, called financial statements, provide summarized information to the owner.