Download

1 / 20

240 likes | 469 Vues

Capacity Markets Investment in Generation Capacity Payments. October 31, 2005 J. W. Charlton. Objective. Advocate an organized capacity market in the form of a formal capacity market versus an energy only market. NYISO Overview. NYISO formed December 1, 1999.

E N D

Capacity Markets Investment in Generation Capacity Payments October 31, 2005 J. W. Charlton

Objective Advocate an organized capacity market in the form of a formal capacity market versus an energy only market

NYISO Overview • NYISO formed December 1, 1999. • Utility generation divestiture rate makes it one of the most divested markets in nation. • NYISO market volume about $7.5 billion in 2004 and over $30 billion since inception. Highest market volume in East. • Unique challenge: New York City is the world’s biggest and most complex load pocket. World finance and communications capital.

New York ISO"Hub of the Northeast" Hydro Quebec 35,137 MW* ISO - New England 26,922 MW* IESO 26,160 MW* New York ISO 32,075 MW* PJM 135,000 MW* PJM 135,000 MW* * = Peak Load in Megawatts

NY Markets • Day-Ahead Energy Market • Real-Time Energy Market • Ancillary Service Markets • Installed Capacity (ICAP/UCAP) Market

Buying Power in New York Bilateral (forward) Contracts 50% NYISO Day-Ahead Market 45 – 50% Real Time <5% Bilateral Contracts outside the NYISO 50% NYISO Day-Ahead Market 45 - 50% NYISO Real-Time Market <5% 100%

Day-Ahead Energy Market • Security Constrained Unit Commitment software simultaneously co-optimizes energy and ancillaries for the least cost solution • Hourly Locational Marginal Prices (LMP) • Binding forward contracts to Suppliers/Loads • Bilateral transactions accommodated concurrently with supply and load bids • Deviations settled against Real-Time Market • Installed capacity suppliers are required to bid in the Day-Ahead Energy market

Real-Time Energy Market • Real-Time Commitment (RTC) • Multi-period security constrained unit commitment & dispatch • Co-optimizes to simultaneously solve load, reserves & regulation • Runs every 15 minutes, optimized over 10 1/4hour periods – total 2 ½ hours • RTC15 posts at time 15 and optimized from T30 through T180 • Issues binding commitments for units to start at T30 and T45 • Real-Time Dispatch (RTD) • Multi-period security constrained dispatch • Co-optimizes to simultaneously solve load, reserves & regulation • Runs approximately every 5 minutes • Optimizes over a 60 minute period • RTD15 posts at T15 and optimizes from T15 through T75

Ancillary Service MarketsHighlights • Market-Based Services • Regulation • 10-Minute Spinning Reserve • Total 10-Minute Reserve • 30-Minute Reserve • Cost-Based Services • Scheduling, Control and Dispatch • Voltage Support • Black Start

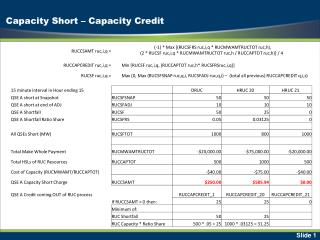

NYISO Installed Capacity Market • ICAP Requirements: • are set in advance for the upcoming Capability Year by the New York State Reliability Council (NYSRC). • Load Serving Entities (LSEs) meet their NYISO-allocated ICAP requirements by: • Self-Supply or Bilateral Transactions with Suppliers. • Purchasing in the Capability Period Auctions (6-month strip). • Purchasing in the Monthly Auctions (for balance of Capability Period). • Paying for the balance of their obligation procured on their behalf in the Spot Market Auction (1-month) using a Demand Curve. • All supply is certified/checked out monthly.

NY Market Revenue Stream • The New York Energy market: • allows suppliers to recover their variable costs and to compete for profits. • The New York Ancillary Services market: • allows suppliers to recover lost opportunity costs when providing ancillary services. • The New York Installed Capacity (ICAP) market: • is intended to promote Resource Adequacy and; • allow suppliers to recover a portion of their fixed (capital) costs. • The total revenue from these markets is the total revenue stream for suppliers.

Revenue Sources • Potential sources of revenues for generating resources are: • Revenue from the energy market during non-shortage hours, net of fuel and operating costs • Revenue generated in periods of shortage when prices can “spike” to levels 20 times higher than the average annual energy price. • Revenue received in the capacity market. • Ancillary services revenues • The economic value of these sources of revenue governs investment and retirement decisions in wholesale electricity markets

Substitutes • Capacity revenues and energy revenues are essentially substitutes. • Under any combination of energy and capacity markets, it is ultimately the market participants that determine the prices in both markets. • Markets with higher capacity revenues generally sustain higher capacity margins and, hence, exhibit less frequent price spikes associated with shortages. • Conversely, markets that generate lower capacity revenues will result in lower capacity margins and more frequent price spikes associated with shortages. • In the limit, energy-only markets that have no capacity revenues rely almost exclusively on severe price spikes to establish long-term economic signals.

History and Political Reality • The Northeastern U.S. Markets are a product of: • the history of power system operation • planning practices • historic grid topology • limitations on offer prices to limit market power abuse • eliminating “seams” issues as barriers to trade, and • the need to provide rational long-term price signals that would encourage investment in new generation and transmission where needed • The political reality is that energy prices will not be allowed to “spike” to the levels necessary to encourage new generator investments. • Even if market design did not limit offer prices, regulatory uncertainty would discourage investment in new generating resources

Insuring Reliability • Several proposals have been entertained to move to an “energy- only” market design. • Simply cannot be made to work with offer caps of $1000 or less • Regulators and many Stakeholders will not support higher offer caps • Suppliers will forever face regulatory uncertainty • Traditional utility owners have divested, or are divesting, their generation portfolios or spinning them off to unregulated generating companies. • There has been significant debate over how to maintain an adequate reserve margin. • Minimum installed capacity requirements were imposed on the regulated utilities in the Northeast long before divestiture. • To guarantee the same level of reliability under a market scenario, all load serving entities are simply required to contract for sufficient capacity to meet their installed capacity obligations.

Installed Capacity Markets in the Northeastern U.S. • ICAP Requirements are set for the upcoming capability year. • Load serving entities can meet their ICAP requirements by: • Self-Supply • Bilateral Transactions with Suppliers • Forward Auctions • Deficiency/Spot Market Auctions • After-the-fact penalty procurement

Locational ICAP • Due to transmission constraints into certain localities, areas or zones, some LSE’s must procure at least some of their ICAP requirements from resources electrically located within that locality. • New York (NY) has had locational requirements since inception. There are two such transmission constrained zones: • New York City and • Long Island • PJM and ISO-NE have proposals pending before FERC to introduce locational ICAP to their control areas.

Summary/Conclusion • The design of the Northeastern installed capacity markets was born of the pre-existing planning and operating practices of the power pools in the northeast. • The market structures and design features recognize the need for: • system reliability (insured through installed capacity requirements) • overall market designs coordinating energy, capacity and ancillary services • reining in potential market power • encouraging robust competition • mitigating potential barriers to trade • certainty, market stability, and • recognizing the political realities of energy price caps and regulatory oversight. • The designs presently employed with installed capacity markets uniquely balances all of the market needs while appropriately recognizing the value of capacity to meet reliability criteria.