Cost Systems Typically Pass Through Four Stages

240 likes | 539 Vues

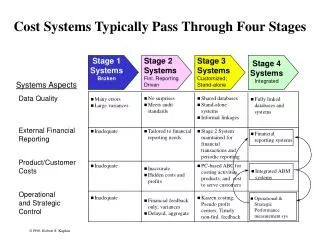

Cost Systems Typically Pass Through Four Stages. Stage 1 Systems Broken. Stage 2 Systems Finl. Reporting Driven. Stage 3 Systems Customized; Stand-alone. Stage 4 Systems Integrated. Systems Aspects. Data Quality. No surprises Meets audit standards. Shared databases

Cost Systems Typically Pass Through Four Stages

E N D

Presentation Transcript

Cost Systems Typically Pass Through Four Stages Stage 1 Systems Broken Stage 2 Systems Finl. Reporting Driven Stage 3 Systems Customized; Stand-alone Stage 4 Systems Integrated Systems Aspects Data Quality • No surprises • Meets audit standards • Shared databases • Stand-alone systems • Informal linkages • Many errors • Large variances • Fully linked databases and systems External Financial Reporting • Inadequate • Tailored to financial reporting needs • Stage 2 System maintained for financial transactions and periodic reporting • Financial reporting systems Product/Customer Costs • Inadequate • PC-based ABC for costing activities, products, and cost to serve customers • Inaccurate • Hidden costs and profits • Integrated ABM systems Operational and Strategic Control • Inadequate • Kaizen costing; Pseudo profit centers; Timely non-finl. feedback • Operational & Strategic Performance measurement sys • Financial feedback • only; variances • Delayed, aggregate • 1996 Robert S. Kaplan

Stage IV Management Reporting & Control Systems Vision: Stage IV Management Reporting and Control Systems will be fully integrated, with a common set of information, entered once and accessible to all, supporting both internal and external reporting. The management systems will provide performance information for operational and strategic control, and accurate measurement of product and customer profitability. Robert S. Kaplan

Stage 2: Yesterday’s Cost Systems were Dependent upon the External Financial Reporting Systems Financial Reporting Systems Product Costing Systems Performance Measurement and Variance Analysis

Stage 3: Today’s Cost Systems are Activity Based, and Break the Linkage from Financial Reporting Systems Financial Reporting Systems Customer Costing Product Costing Systems Operational Feedback for Learning and Improvement: Yields, Defects, Cycle Time, Throughput, Actual Resource Consumption (quantity and cost) Activity Based Management Systems

Stage III: ABC with Fungible Resources • Customer Administration Department Activities Performed • Handle Customer Orders • Process Customer Complaints • Perform Customer Credit Checks • Stage III ABC System • 1. Estimate Costs of Resources Supplied $560,000 • 2. Estimate Percentage of Time on Each Activity • 3. Determine Quantity of Activity Performed • 4. Calculate Activity Cost Driver Rates

Stage IV: Capacity Costing with Fungible Resources • Stage IV ABC System • 1. Estimate Cost of Resources Supplied $560,000 • 2. Estimate Practical Capacity of Resources Supplied 8,000 hours • 3. Calculate Cost of Unit of Capacity $70/hour • 4. Estimate Unit Times to Perform Each Activity • 5. Calculate Capacity-Based Activity-Cost Driver Rates

Activity-Based Cost Management: Strategic Decisions and Operational Improvements What activities should we perform? • Product design • Product-line and customer mix • Supplier relationships • Customer relationships - Pricing - Order size - Delivery - Packaging • Market segmentation • Distribution channel Strategic View Activity-Based Costing Operational View • Resources • Activities • Business processes • Cost drivers • Product costs • Customer costs What drives activity cost? • Activity management • Business process reengineering • Total quality • Performance measurement • 1996 Robert S. Kaplan

ABC Implementation Steps STAGE ACTION ACTIVITIES INITIATE 1 2 3 4 • Identify Purpose of ABC Project • Select Project Sponsor • Develop Executive Awareness (e.g., ABC Seminar/ Videos) • Establish Senior Management Steering Committee • Select and Train Multi-function Project Team (Operations, Finance, Engineering, Marketing, I/T) • Conduct Interviews • Choose Activities, Business Processes, Activity Cost Drivers • Access Company Data Bases; Select ABC Software • Calculate: Activity Costs, Driver Costs, Product and Customer Profitability (Whale Curves) • Change Product Pricing, Mix, and Design • Modify Customer/Channel/Supplier Relationships • Achieve Process Efficiencies • Increase Revenues • Reduce Operating Expenses ANALYZE ACT EXPLOIT

Action Implications from ABC Model • Perform fewer activities: • Pricing • Change product mix • Change customer mix • Minimum order quantities • Fewer changes (ECNs, delivery terms) • Improve product designs: • Fewer parts • More common parts

Action Implications from ABC Model (cont.) Perform activities more efficiently • Improve business processes (TQM, kaizen, JIT) • Improve quality • Reduce setup and process cycle times • Improve layout • Focus operations • Reengineer • Invest in information technologies: • Customer and supplier information systems • Computer-aided-design and engineering (CAD/CAE) • Computer integrated manufacturing (CIM) • Electronic data interchange (EDI)

Action Implications from ABC Model (cont.) Planning for the future • Budgeting: authorize spending on resources based on projected demands by products, customers, and facilities • Target costing

Organizing an ABC Project Phase Advocate Sponsor Agent Target • Analysis:ABC -- “Show me the numbers” • Action:ABM -- “Show me the Money”

Individual and Organizational Resistance to ABC Information • Threat and embarrassment caused by revelation of error: • Unprofitable products and customers • Poorly designed products and inefficient processes • Costly supplier relationships • Excess capacity • New technical theory: Contradicts teaching and experience of past 30 years • New role for finance organization: • From objective, historical scorekeeper to information provider for operational and strategic decision-making

Daily, Actual Activity-Based Costs with an Enterprise Resource Planning Package Day Activity Expense Quantitiy (of ACD) Activity-Cost Driver Rate Monday $12,468 253 $49.28 Tuesday 13,491 228 59.17 Wednesday 19,514 262 74.48 Thursday 9,882 280 35.29 Friday 14,533 239 60.81

Daily, Actual Activity-Based Costs with an Enterprise Resource Planning Package Day Activity Expense Quantitiy (of ACD) Activity-Cost Driver Rate Monday $12,468 253 $49.28 Tuesday 13,491 228 59.17 Wednesday 19,514 262 74.48 Thursday 9,882 280 35.29 Friday 14,533 239 60.81 THIS IS MADNESS!!! • Random variation in numerator (which expenses hit general ledger each day?) • Random variation in denominator (number of orders handled daily) • Random variation in process efficiency

Stage 4: Tomorrow’s Cost Systems will be integrated with each other and with Financial Reporting Systems • Financial Reporting • Systems Activity Based Management Systems Planning and Budgeting Actual Utilization and Efficiencies Operational and Strategic Performance Measurement Systems

ABB is a reversal for the relationship set up in an ABM model ABM ABB Resources Resources Resource Drivers Resource Drivers Activities Activities Activity Cost Drivers Activity Cost Drivers Products Products

Causality allows for accurate budgeting Activity Cost Drivers Activities Required Resources Products Place Order # of orders Produce Product Financial Reports # of product lines Set up & Run Machine # of production batches Pack & Ship Product # of shipments

Characteristics of ABB • Expected demands collected from forecasted product/ customer volume and mix • Determine activity cost driver quantities • Association between cost drivers and demand for activities • Linking activity demands to supply and spending on resources • Recognition of excess capacity

Spending patterns are different for different resources Customer Support Labor Supplies Building/Plant

Stage 4: Tomorrow’s Cost Systems will be integrated with each other and with Financial Reporting Systems • Financial Reporting • Systems Activity Based Management Systems Planning and Budgeting Actual Utilization and Efficiencies Operational and Strategic Performance Measurement Systems

Cost Systems Typically Pass Through Four Stages Stage 2 Systems Finl. Reporting Driven Stage 3 Systems Customized; Stand-alone Stage 4 Systems Integrated Stage 1 Systems Broken Systems Aspects Data Quality • No surprises • Meets audit standards • Shared databases • Stand-alone systems • Informal linkages • Many errors • Large variances • Fully linked databases and systems External Financial Reporting • Inadequate • Tailored to financial reporting needs • Stage 2 System maintained for financial transactions and periodic reporting • Financial reporting systems Product/Customer Costs • Inadequate • PC-based ABC for costing activities, products, and cost to serve customers • Inaccurate • Hidden costs and profits • Integrated ABM systems Operational and Strategic Control • Inadequate • Kaizen costing; Pseudo profit centers; Timely non-finl. feedback • Operational & Strategic Performance measurement sys • Financial feedback • only; variances • Delayed, aggregate • 1996 Robert S. Kaplan