### Accounting for Long-Lived Asset Impairment and Disposal Issues: Insights from Industry Experts ###

Join a panel of experts, including Julie Erhardt from Arthur Andersen, Richard Stock from Exxon Mobil, and Ed Trott from the Financial Accounting Standards Board, as they discuss the latest perspectives on accounting for obligations linked to the retirement of long-lived assets. This session will cover recent literature on asset impairment and disposals, emphasizing regulatory changes, including the introduction of ED and its implications for the accounting landscape. Key comparisons with existing statements and practical issues faced by preparers and auditors will also be addressed, ensuring a comprehensive understanding of these critical topics. ###

### Accounting for Long-Lived Asset Impairment and Disposal Issues: Insights from Industry Experts ###

E N D

Presentation Transcript

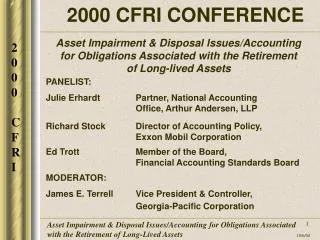

2000 CFRI CONFERENCE Asset Impairment & Disposal Issues/Accounting for Obligations Associated with the Retirement of Long-lived Assets PANELIST: Julie Erhardt Partner, National Accounting Office, Arthur Andersen, LLP Richard Stock Director of Accounting Policy, Exxon Mobil Corporation Ed Trott Member of the Board, Financial Accounting Standards Board MODERATOR: James E. Terrell Vice President & Controller, Georgia-Pacific Corporation

KEY CURRENT LITERATURE REGARDING LONG-LIVED ASSET IMPAIRMENTS AND DISPOSALS: • Statement 121 • EITF 94-3 • SAB 100 • APB 30 / EITF 95-18 Discontinued Operations • APB 29- Spin-offs and Certain Exchanges • EITFs 87-11, 90-6, and 95-21 - Assets Purchased that are to be Disposed of

THE ED ON LONG-LIVED ASSET IMPAIRMENTS AND DISPOSALS: • Replaces Statement 121 • Nullifies Most of EITF 94-3 • Replaces APB 30 / EITF 95-18 Discontinued Operations • Provides Guidance for Applying APB 29 • Nullifies EITFs 87-11, 90-6, and 95-21 • Will Impact Consolidation Policy Regarding “Temporary Control” • Does Not Affect EITF 95-3 - - Purchasing Accounting • Effective for Fiscal Years Beginning after December 15, 2001

COMPARISONS WITH STATEMENT 121: • What is the Same… • Two Step Process for Assets to be Held and Used • Recoverability (Does Undiscounted Cash Flow Recover the Carrying Amount?) • Fair Value (Is the Current Fair Value Below Carrying Amounts?) • Grouping Assets at the Lowest Level for Identifiable / Independent Cash Flows

COMPARISONS WITH STATEMENT 121 (continued): • What is the Same... • Use of Events to Trigger Testing • Write-down to Fair Value if Held and Used Assets are Impaired • Lower of Carrying Amount or Fair Value for Assets Held for Sale • No Depreciation for Assets for Held Sale

COMPARISONS WITH STATEMENT 121 (continued): • What has Changed... • Use of “Expected” Cash Flow Approach -- Probability-weighted - - for Recoverability Testing and Fair Value • More Guidance on Cash Flow Estimates (Repairs, Maintenance, and Replacements, Interest to be Capitalized, Life of Primary Asset) • More Guidance on when an Asset is Held for Sale (Available for Immediate Sale on Normal Delivery Terms, Probable of Being Sold within a Year, Etc.)

COMPARISONS WITH STATEMENT 121 (continued): • What has Changed… • Guidance Provided for Events after Balance Sheet Date • Guidance Provided for Changes to a Plan of Sale • Separate Guidance for Disposals Other Than by Sale • Abandonments (Don’t Stop Depreciation While in Use) • Spin-offs (See APB 29 Guidance) • Exchanges of Similar Productive Assets (See APB 29 Guidance)

ISSUES: PREPARER PERSPECTIVE • Fair Value of Initial Measurement • Applies to Measurement of Both ARO and Impairment • Market-oriented • Required by CON 7 • Differs from FAS 5 • Inconsistent with Business Plans • Requires the Elimination of Contractual Relationships- Example 2 Impairment ED

ISSUES: PREPARER PERSPECTIVE • Expected Cash Flows • Differs from Best Estimate Concept of FAS 5 • Requires Risk-free Rate (Credit Adjusted for ARO) Applied to Probability Weighted Cash Flows • Differs from Traditional Approach in FAS 121 • Inconsistent with Business Plans

ISSUES: PREPARER PERSPECTIVE • Other Issues (Impairment ED) • Impairment of Assets at the Entity Level • Consideration of Cash Flows and Capital Expenditures of Future Development

ISSUES: AUDITOR’S PERSPECTIVE • Projected Cash Flows • Completeness of the Cash Flow Scenarios • Accuracy of the Assumed Cash Flows based only on the asset’s existing service potential • Validity of the Probabilities of each Cash Flow Scenario • What constitutes “Available Evidence” related to each of the above items

ISSUES: AUDITOR’S PERSPECTIVE • Assets Held for Sale: • Probability of a Sale Within One Year • Validity of “Unlikely Events” Driving a Later Decision Not to Sell an Asset • Appropriateness of an Impairment Charge (Asset Held for Sale) Versus Depreciating the Asset Over a Shortened Remaining Life (Asset to be Abandoned) • Verifiability of a Decision to Sell an Asset Being Made at, Not After, the Balance Sheet Date

COMPARISONS WITH EITF 94-3: • What is the Same… • Requirements for a One-time Termination Plan • Most Disclosure Requirements • Covers Only One-time Benefit Arrangements -- Not On-going Plans that are Covered by Statement 112

COMPARISONS WITH EITF 94-3 (continued): • What is Changed… • Employee Termination Benefits Recognized like a Stay-bonus Rather than as a Payment for Past Services (If Future Service Required) • Operating Lease Cost Spread over Revised Utilization Period Rather than All Pushed Back • Delay in Recognition of Other Liabilities (Other than Terminations of Existing Contractual Obligations Other than Operating Leases)

ISSUES: PREPARER PERSPECTIVE • Termination Benefits (ImpairmentED) • Does Not Recognize Service • Differs from FAS 5 and EITF 94-3 that a Liability Arises when the Entity Commits to the Employees • Differs from the Treatment of Nominal Service Periods Under FAS 106 • Differs from Lease Termination Penalties

ISSUES: PREPARER PERSPECTIVE • Termination Benefits (ImpairmentED) • Does Not Recognize Service • Differs from FAS 5 and EITF 94-3 that a Liability Arises when the Entity Commits to the Employees • Differs from the Treatment of Nominal Service Periods Under FAS 106 • Differs from Lease Termination Penalties

ISSUES: AUDITOR’S PERSPECTIVE • Termination Benefits • Verifiability of a Termination Payment Stemming From: • A Pre-existing FAS 112 Plan (Accrue when Payment is Probable), • Or • A One-time Arrangement (Accrue Over the Employee’s Remaining Service Period)

MAJOR CHANGES TO APB 30 / EITF 95-18 DISCONTINUED OPERATIONS (DO): • What is the Same… • The Display of DO on a Net of Tax Basis Below Continuing Operations

MAJOR CHANGES TO APB 30 / EITF 95-18 DISCONTINUED OPERATIONS (DO)--(continued): • What is Changed… • Criteria for what can be Displayed as a DO (Operations of a Significant Component of an Entity: (a) that Either has been Disposed of by Sale or Otherwise or is Classified as Held for Sale and; (b) Where Activities, Operations and Assets have been or will be Eliminated in the Disposal Transaction) will Allow for More DO Presentations • Prohibition of Accruing for Future Losses at Measurement Date

MAJOR CHANGES TO APB 30 / EITF 95-18 DISCONTINUED OPERATIONS (DO)--(continued): • What is Changed… • Assets and Related Liabilities Held for Sale shown Broad Rather than Net • No Pushback of Decision to DO if After Balance Sheet Date

ISSUES: AUDITOR’S PERSPECTIVE • Discontinued Operations • Validity of and Consistency of Conclusions that Discontinued Operations are “Significant”; a Judgmental Criterion • Verifiability of a Decision to Discontinue an Operation Being Made At, Not After, the Balance Sheet Date

WHAT GUIDANCE IS GIVEN FOR APB 29: • At the Spin-off Date, the Spinee Operations is to be Written Down (Through the P&L) to its Lower of Carrying Amount or Fair Value • At the Exchange Date of a Similar Productive Asset, the Transferred Asset is Written Down (Through the P&L) to its Lower Carrying Amount or Fair Value

ISSUES: PREPARER PERSPECTIVE • Other Issues (Impairment ED) • Exchanges of Similar Productive Assets and Spin-offs • Subject to Measurement at Fair Value Without Recognition Test • Held for Sale Criteria • Definition of Normal Delivery Terms (Para 30b) • Assets to be Sold as a Group (Para 30e)

WHAT GUIDANCE IS GIVEN IN PLACE OF EITFS 87-11, 90-6, AND 95-21: • Assets and Related Liabilities Displayed Broad Rather than Net • Results of Operations Recognized as they Occur Rather than Being Absorbed in the Purchase Price Allocation

WHAT IS THE IMPACT ON CONSOLIDATION POLICY - “TEMPORARY CONTROL”: • The Exemption to Consolidation for Entities Where Control is Temporary will be Deleted • Assets and Related Liabilities will be Treated Like Other Net Asset Groups Held for Sale

TREATMENT OF GOODWILL: • ED Approach is Like that in Statement 121 • Input Received on Business Combinations ED will Affect this Area

KEY CURRENT LITERATURE REGARDING ASSET RETIREMENT OBLIGATIONS: • Statement 19 - Oil and Gas Operations • SOP 96-1 - Environmental Remediation Liabilities

THE ED ON LONG-LIVED ASSET RETIREMENT OBLIGATIONS: • Replaces Guidance in Statement 19 • Impacts all Companies that have a Retirement Obligation for Long-lived Assets (This is Not Just for Utilities, Landfill, Mining or Oil and Gas) • Will Increase Leverage by Requiring a Retirement obligation be Recognized as a Liability Rather than as Part of Depreciation

THE ED ON LONG-LIVED ASSET RETIREMENT OBLIGATIONS (continued): • Will Require that a Liability be Recognized for a Retirement Obligation Sooner than Current Practice • Will have the Initial Liability Recognition be Based on Fair Value Rather than Accumulated Costs (Examples in the ED Show the Impact of this Measurement) • Effective for Fiscal years Beginning after June 15, 2001

KEY PROVISIONS IN THE ED: • Retirement Obligations are those that are Unavoidable as a Results of the Acquisition or Normal Operations of a Long-lived Asset • The Initial Amount Recorded as a Liability is Added to the Long-lived Asset’s Cost Basis • Accretion of the Time Value of Money (Discount) is a Period Expense and Not Subject to Capitalization Under Statement 34

KEY PROVISIONS IN THE ED (Continued): • Fair Value of the Liability is Expected to be Determined by an Expected Present Value Technique (Concept Statement 7, Probability-weighted; Includes Inflation, Overhead, Profit Margin, Market Risk Premiums, Etc., Discounted Using A Credit-adjusted Risk-free Rate) • Changes in Estimates Adjust the Liability and Capitalized Cost

ISSUES: PREPARER PERSPECTIVE • Constructive Obligations (ARO ED) • AROs for Constructive Obligations-F/N 27 • Do All Assets have Retirement Obligations that are Not Conditional? • Or • When Retirement Obligations Exist are They Not Conditional? • AROs for Interim Property Retirements (Para. 53)

ISSUES: PREPARER PERSPECTIVE • Oil & Gas Industry (ARO) • Matching of Revenues Generated by Production with Accrual of ARO • Transition • Will have the Effect of Reversing Previous Accruals and Re-accruing in the Future • Costly to Implement. Need to Research Historical Data to Determine Accumulated Depreciation • Grouping of Assets

ISSUES: AUDITOR’S PERSPECTIVE • Scope • Obligations for Interim Property Retirements (Within the ED’s Scope), • Vs. • Obligations for Ongoing Operation of the Asset (Outside the ED’s Scope) • Example: • Replace a Section of a Gas Pipeline

ISSUES: AUDITOR’S PERSPECTIVE • Recognition • Applying the “Probable Future Sacrifice … that an Entity has Little or No Discretion to Avoid” Criterion • Examples: • Asset Removal Laws are Not Enforced and No Removals have ever taken Place • Asset Removal is Merely General Practice (No Laws); Non-removal Yields Adverse Publicity

ISSUES: AUDITOR’S PERSPECTIVE • Measurement • “Expected Cash Flow” Model - Same Issues as with the Impairment ED • Meshing the ED’s Anticipatory “Fair Value” Measurement Guidance With Its “Present Responsibility” Recognition Guidance • Example - Pending Law Changes • Example - “Cut and Cover” Strip Mine