Download

1 / 25

280 likes | 777 Vues

Acquisition of Assets. TEXT CHAP 10. Objectives. Prepare the entries in the acquiring company for the acquisition of assets . Applicable accounting standards. AASB 1015 Acquisition of Assets AASB 1013 Accounting for Goodwill. Acquisition of Assets. Single asset Set of Assets

E N D

Acquisition of Assets TEXT CHAP 10

Objectives • Prepare the entries in the acquiring company for the acquisition of assets

Applicable accounting standards • AASB 1015 Acquisition of Assets • AASB 1013 Accounting for Goodwill

Acquisition of Assets • Single asset • Set of Assets • Acquisition of an entity (collection of net assets)

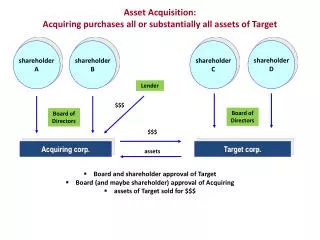

Acquisition of an entity • A company is allowed to acquire the net assets of another company and is also allowed to indirectly acquire the net assets by purchasing the shares of another company • Their are 4 principal forms of acquisition of net assets of a company

Four principal forms of acquisition of an entity • A Ltd purchases the net assets of B Ltd. B Ltd continues with its assets and liabilities replaced with purchase consideration • A Ltd acquires the net assets of B Ltd . B Ltd liquidates • C Ltd is formed to acquire the net assets of A Ltd & B Ltd. Both A Ltd & B Ltd are liquidated • A Ltd acquires the issued shares of B Ltd , B Ltd continues with its shares owned by A Ltd

Acquisition of Assets • Accounting entries for acquisition • cost of acquisition ie Assets given up • fair value of assets acquired • in the case of purchase of an entity whether goodwill/discount on acquisition AASB 1013

Cost of acquisition • The cost of acquisition consists of the purchase consideration & any incidental costs incurred • The purchase consideration is rarely in a single form usually it consists cash, shares and other assets (e.g. Land & Buildings) • These assets given up as per AASB 1015 must be valued at their fair value

Fair Value of Assets Given Up • Cash - normally equivalent but if settlement date deferred - discount to present value • Non-monetary assets • e.g. Land & Buildings (valued by use of experts) • Securities • listed companies (current market price) • unlisted (various techniques but may have to use a surrogate eg fair value of assets acquired) • Liabilities • Present value of future amount • Acquisition Date • Important -(date rights & obligations exchange)

Accounting entries • Single asset • entry recorded at the cost of acquisition • Set of asset • Where the asset consists of more than one asset then the cost of the asset is apportioned over the assets acquired. • The process is to allocate in proportion to fair values of assets acquired eg Purchased for $300 000 Land FV 40 000 Buildings FV 200 000 Furniture FV 80 000 $320 000

Accounting entries • Single asset • entry recorded at the cost of acquisition • Set of asset • Where the asset consists of more than one asset then the cost of the asset is apportioned over the assets acquired. • The process is to allocate in portion to fair values of assets acquired eg Purchased for $300 000 Land FV 40 000 Buildings FV 200 000 Furniture FV 80 000 $320 000 Entry Dr Land (40/320*300) 37 500 Dr Blgds (200/320*300) 187 500 Dr Furn (80/320*300) 75 000 Cr Cash 300 000

Accounting requirementsAcquisition of an entity Assets acquired $ x (fair values) less:: Cost of acquisition $ x (fair values of assets given up) ----- Difference$ x (goodwillor discount on acquisition) (AASB 1013 ACCOUNTING FOR GOODWILL)

Accounting entries • entry:: Dr Assets acquired (at their fair values) CR Liabilities (acquired) Dr Goodwill Cr Share Capital (shares given up)

AASB 1013 Accounting for Goodwill • Goodwill • has to be written off using straight line method over 20 years or at director’s discretion provided less than 20 years • Discount on acquisition • is to be written off the non-monetary assets in proportion to their fair values non-monetary assets not defined but • monetary assets as per AASB 1010 cash & receivables • Therefore allocate against assets other than cash & receivables

Example RABBIT LTD TRIAL BALANCE AS AT 1/1/92 ASSUME:: *WOLF LTD TAKES OVER NET ASSETS OF RABBIT LTD *COSTS WOLF LTD $2050 *SHAREHOLDERS TO RECEIVE I SHARE FOR EVERY 1 SHARE HELD (M.V. $2) *DEBENTURE HOLDERS TO BE PAID IN CASH +2% PAID UP CAPITAL $1 36,000 RETAINED PROFITS 21,500 EQUIPMENT 42,000 ACC. DEPRECIATION 10,000 INVENTORY 18,000 DEBTORS 10,000 BILLS RECEIVABLE 6,000 PATENTS 3,500 DEBENTURES 4,000 CREDITORS 8,000 $79,500 $79,500

Example RABBIT LTD TRIAL BALANCE AS AT 1/1/92 ASSUME:: *WOLF LTD TAKES OVER NET ASSETS OF RABBIT LTD *COSTS WOLF LTD $2050 *SHAREHOLDERS TO RECEIVE I SHARE FOR EVERY 1 SHARE HELD (M.V. $2) *DEBENTURE HOLDERS TO BE PAID IN CASH +2% PAID UP CAPITAL $1 36,000 RETAINED PROFITS 21,500 EQUIPMENT 42,000 ACC. DEPRECIATION 10,000 INVENTORY 18,000 DEBTORS 10,000 BILLS RECEIVABLE 6,000 PATENTS 3,500 DEBENTURES 4,000 CREDITORS 8,000 $79,500 $79,500 COST OF ACQUISITION CASH:: COSTS 2,050 DEBENTURES 4,080 SHARES(36,000* $2) 72,000 $78,130 (also have to pay the GST ignored for our examples)

COST $78,130 ASSUME FAIR VALUE ASSETS ACQUIRED:: EQUIPMENT 36,000 INVENTORY 20,000 DEBTORS 9,000 PATENTS 4,000 BILLS REC. 6,000 CREDITORS (8,000) $67,000 EXAMPLE RABBIT LTD TRIAL BALANCE AS AT 1/1/92 PAID UP CAPITAL $1 36,000 RETAINED PROFITS 21,500 EQUIPMENT 42,000 ACC. DEPRECIATION 10,000 INVENTORY 18,000 DEBTORS 10,000 BILLS RECEIVABLE 6,000 PATENTS 3,500 DEBENTURES 4,000 CREDITORS 8,000 $79,500 $79,500

COST $78,130 ASSUME FAIR VALUE ASSETS ACQUIRED:: EQUIPMENT 36,000 INVENTORY 20,000 DEBTORS 9,000 PATENTS 4,000 BILLS REC. 6,000 CREDITORS (8,000) $67,000 EXAMPLE RABBIT LTD TRIAL BALANCE AS AT 1/1/92 PAID UP CAPITAL $1 36,000 RETAINED PROFITS 21,500 EQUIPMENT 42,000 ACC. DEPRECIATION 10,000 INVENTORY 18,000 DEBTORS 10,000 BILLS RECEIVABLE 6,000 PATENTS 3,500 DEBENTURES 4,000 CREDITORS 8,000 $79,500 $79,500 ASSETS ACQUIRED 67,000 COST 78,130 CASH 6,130 SHARES 72000 (36,000 *$2) GOODWILL $11,130

COST $78,130 ASSUME FAIR VALUE ASSETS ACQUIRED:: EQUIPMENT 36,000 INVENTORY 20,000 DEBTORS 9,000 PATENTS 4,000 BILLS REC. 6,000 CREDITORS (8,000) $67,000 EXAMPLE RABBIT LTD TRIAL BALANCE AS AT 1/1/92 GOODWILL EXAMPLE:::entry DR EQUIPMENT 36,000 DR INVENTORY 20,000 DR DEBTORS 10,000 CR PROV D, DEBTS 1,000 DR PATENTS 4,000 DR BILLS REC 6,000 DR GOODWILL 11,130 CR CREDITORS 8,000 CR RABBIT LTD 72,000 CR CASH 6,130 DR RABBIT LTD 72,000 CR SHARE CAPITAL 72 000 PAID UP CAPITAL $1 36,000 RETAINED PROFITS 21,500 EQUIPMENT 42,000 ACC. DEPRECIATION 10,000 INVENTORY 18,000 DEBTORS 10,000 BILLS RECEIVABLE 6,000 PATENTS 3,500 DEBENTURES 4,000 CREDITORS 8,000 $79,500 $79,500 ASSETS ACQUIRED 67,000 COST 78,130 CASH 6,130 SHARES 72000 (36,000 *$2) GOODWILL $11,130

Amortisation of Goodwill • Goodwill- $11 130 • Assume that the goodwill is written off over 10 years • Journal Entry Dr Amortisation of Goodwill 1 113 CR Goodwill 1 113 (or Provision for Goodwill) • Balance Sheet Intangibles (Note x) 10 017

COST $78,130 ASSUME FAIR VALUE ASSETS ACQUIRED:: EQUIPMENT 45,000 INVENTORY 25,000 DEBTORS 9,000 PATENTS 5,000 BILLS REC. 6,000 CREDITORS (8,000) $82,000 EXAMPLE RABBIT LTD TRIAL BALANCE AS AT 1/1/92 PAID UP CAPITAL $1 36,000 RETAINED PROFITS 21,500 EQUIPMENT 42,000 ACC. DEPRECIATION 10,000 INVENTORY 18,000 DEBTORS 10,000 BILLS RECEIVABLE 6,000 PATENTS 3,500 DEBENTURES 4,000 CREDITORS 8,000 $79,500 $79,500 DISCOUNT EXAMPLE

COST $78,130 ASSUME FAIR VALUE ASSETS ACQUIRED:: EQUIPMENT 45,000 INVENTORY 25,000 DEBTORS 9,000 PATENTS 5,000 BILLS REC. 6,000 CREDITORS (8,000) $82,000 EXAMPLE RABBIT LTD TRIAL BALANCE AS AT 1/1/92 PAID UP CAPITAL $1 36,000 RETAINED PROFITS 21,500 EQUIPMENT 42,000 ACC. DEPRECIATION 10,000 INVENTORY 18,000 DEBTORS 10,000 BILLS RECEIVABLE 6,000 PATENTS 3,500 DEBENTURES 4,000 CREDITORS 8,000 $79,500 $79,500 ASSETS ACQUIRED 82,000 COST 78,130 CASH 6,130 SHARES 72000 (36,000 *$2) DISCOUNT $3.870

COST $78,130 ASSUME FAIR VALUE ASSETS ACQUIRED:: EQUIPMENT 45,000 INVENTORY 25,000 DEBTORS 9,000 PATENTS 5,000 BILLS REC. 6,000 CREDITORS (8,000) $82,000 EXAMPLE RABBIT LTD TRIAL BALANCE AS AT 1/1/92 DISCOUNT:: NON-M F.V. ALLOCATION COST EQUIP 45,000 2,322 (45/75) 42,678 INVENT 25,000 1,290 (25/75) 23,710 PATENTS 5,000 258 ( 5/75) 4,742 -------- ------- -------- $75,000 $3,870 $71,130 DR EQUIP 42,678 DR INVENT 23,710 DR PATENTS 4,742 DR BILLS REC 6,000 DR DEBTORS 10,000 CR PROV D. DEBTS 1,000 CR CREDITORS 8,000 CR CASH 6,130 CR RABBIT LTD 72,000 PAID UP CAPITAL $1 36,000 RETAINED PROFITS 21,500 EQUIPMENT 42,000 ACC. DEPRECIATION 10,000 INVENTORY 18,000 DEBTORS 10,000 BILLS RECEIVABLE 6,000 PATENTS 3,500 DEBENTURES 4,000 CREDITORS 8,000 $79,500 $79,500 ASSETS ACQUIRED 82,000 COST 78,130 CASH 6,130 SHARES 72000 (36,000 *$2) DISCOUNT $3.870

Buying Company Purchases the Shares • Where the buying company purchases the net assets of another company indirectly by purchasing the issued shares of that company entries • in selling company nil entries • - in the buying company • DR INVESTMENT CR SHARE CAPITAL

Tutorial Questions Exercise 10.2 (Part B only) Exercise 10.3 Exercise 10.4 ( Amend ARR $140 000) Problem 10.1 (Part A only) Problem 10.5 (parts B & C only)