Capital Budgeting Overview

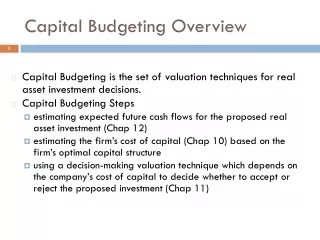

Capital Budgeting Overview. Capital Budgeting is the set of valuation techniques for real asset investment decisions. Capital Budgeting Steps estimating expected future cash flows for the proposed real asset investment (Chap 10)

Capital Budgeting Overview

E N D

Presentation Transcript

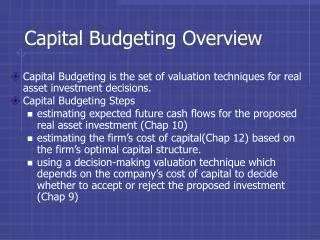

Capital Budgeting Overview • Capital Budgeting is the set of valuation techniques for real asset investment decisions. • Capital Budgeting Steps • estimating expected future cash flows for the proposed real asset investment (Chap 10) • estimating the firm’s cost of capital(Chap 12) based on the firm’s optimal capital structure. • using a decision-making valuation technique which depends on the company’s cost of capital to decide whether to accept or reject the proposed investment (Chap 9)

Chapter 12 The Cost of Capital Merck & Co. Jordan Air (#23)

Chapter 12 Learning Objectives • Describe the concepts underlying the firm’s cost of capital (known as weighted average cost of capital) and the purpose for its calculation. • Calculate the after-tax cost of debt, preferred stock and common equity. • Calculate a firm’s weighted average cost of capital. • Adjust the firm’s cost of capital on a by division or by project basis. • Use the cost of capital to evaluate new investment opportunities.

Cost of Capital • The firm’s cost of raising new funds that primarily reflects the investor’s required rate of return. • The weighted average of the cost of individual types of funding to the firm. • Differences between investor’s required rate of return and cost of capital arise from taxes and flotation costs. • One possible decision rule is to compare a project’s expected return (IRR) to the cost of the funds that would be used to finance the purchase of the project. • Accept if : project’s IRR > cost of capital.

Cost of Capital Terms • Capital Component = type of financing such as debt, preferred stock, and common equity • kd = cost of new debt, before tax • kd(1-T) = after-tax component cost of debt • kps = component cost of new preferred stock • kcs or kc = component cost of internal equity (retained earnings), same as what was used Chapters 6 and 8

More Cost of Capital Terms • kncs = cost of new common stock. • WACC or kwacc = the weighted average cost ot capital which is the weighted average of the individual component costs of capital. • wi = the proportion of financing type i used in the firm’s planned capital structure,

Component Cost of Debt • Remember, a corporation can deduct their interest expense for tax purposes. • Therefore, the component cost of debt is the after-tax interest rate on new debt. • kd(1-T). • Where T is the company’s marginal tax rate. • If a company raises new debt capital through bank loans, kd is the interest rate on new debt. • If a company sells new bonds…

Component Cost of Debt • The estimate of kd can be based by finding the expected YTM on the company’s new bonds. • NPd = $It(PVIFA kd,n) + $M(PVIF kd,n) • Where NPd = net proceeds per bond = market value less flotation costs.

Cost of Debt Example • We want to estimate the cost of debt for Merck which has a marginal tax rate of 35%. Let’s assume Merck would issue 10 year bonds at the current market price with flotation costs equal to 1.5% of the par value, and we find the following bond quote. Bond Cur Yld Vol Close Net Chg Merck 6s12 6.1 25 98 +1/4 • Annual coupon rate = 6%, n = 2012-2002 = 10 years , Price = 98% of par value, Semiannual coupons, Assume $1000 par value. • Find YTM = kd

Merck’s cost of debt • Expected Net Proceeds = 98% - 1.5% = 96.5% of par value = 96.5%($1000) = $965 • Annual coupon = 6%($1000) = $60, N = 10. • Semi-annual coupons: • 965 = 60/2 (PVIFAYTM/2,2(10)) +1000(PVIFYTM/2,2(10)) • 965= 30(PVIFAYTM/2,20) +1000(PVIFYTM/2,20) • -965 = PV, 1000 = FV, 30 = PMT, 20 = N, SOLVE FOR I/Y = YTM/2 = 3.24% • YTM = kd = 6.5%, kd(1-T) = 6.5%(1-.35) = 4.2%

Cost of Preferred Stock, kps • Cost of new preferred stock • kps= Dps / NPps • Dp = annual preferred stock dividend • NPps =net proceeds per share from sale of preferred stock • Preferred Stock Characteristics • Par Value, Annual Dividend Rate(% of Par) • generally: no voting rights; must be paid dividends before common dividends can be paid

Cost of Preferred Stock Example • Merck wants to sell new preferred stock. The par value will be $25 a share. Merck decides they will pay an annual dividend yield of 8%. Merck’s advisors say the stock will sell for the $25 par value if the dividend yield is 7.6% and flotation costs will be $1 a share. What is the cost of this new preferred stock. • Dps = .08($25) = $2 • NPps = $25 - $1 = $24 • kps = $2/$24 = 8.3%

Cost of Common Equity (Retained Earnings), kcs • 2 different approaches can be used to estimate the cost of equity. • The two approaches assume that the company’s stock price is in equilibrium. • Theoretically, they should equal each other.

The Dividend Growth Model • The expected return formula derived from the constant growth stock valuation model. • kcs = D1 / Pcs + g = D0(1+g)/Pcs + g • In practice: The tough part is estimating g. • Security analysts’ projections of g can be used. • According to the journal, Financial Management, these projections are a good source for growth rate estimates. • Possible Sources for g: Value Line Investment Survey and Institutional Brokers’ Estimate System (I/B/E/S)

Dividend Growth estimate for the Cost of Common Equity for Merck • Recent Stock Price (P0): $53.60 • Current Dividend (D0): $1.40 • According to Value Line Investment Survey, earnings are expected to grow by 10%, and their dividend growth estimate is 8%. • What to do? Why not go with higher one to be conservative. • Our growth estimate(g): 10% • kcs = ($1.40(1.1)/$53.60) + 10% = 12.9%

Merck’s estimated cost of new common stock, kncs • If Merck decides to sell new common stock to raise additional capital, then • Kncs = D1/NPcs + g = D0(1+g)/NPcs + g • P0: $53.60, D0: $1.40, g = 10% • Assume new stock can be sold at the current market price and Merck will incur a 15% flotation cost per share. NP = $53.60(1-.15) = $45.56 • kncs = $1.40(1.1)/$53.60(1-0.15) + 10% = $1.54/$45.56 + 0.1 = 0.133 = 13.4%

The CAPM Approach to the Cost of Common Equity • The CAPM Approach: is the required rate of return from Chapters 6 and 8. • kc = kRF + β(kM - kRF) • kRF = risk-free rate, • Β = stock’s beta, market risk. • (kM - kRF) = market return minus risk-free rate = market risk premium.

Issues in Implementing CAPM: • Must obtain estimates of kRF, B, and kM – kRF. • Can use Treasuries to estimate kRF. But what time to maturity? • Since capital budgeting involves long-term investments, 10 or 20 year T-bond rates make sense. • Many published sources of B estimates. • Value Line Investment Survey, Standard & Poor’s, and Merrill Lynch. • For kM – kRF, can use historical difference between market return and long-term T-bonds.

Merck’s CAPM Estimate for the Cost of Equity. • Example: The recent 10-yr T-bond rate is 5.2% (risk-free rate ), historical difference between S&P 500 and long-term T-bonds is 7.8% (market risk premium), and Merck’s beta from Value Line is 0.95. What is Merck’s CAPM cost of common equity? • kc = 5.2% + 0.95(7.8%) = 12.6%

Weighted Average Cost of Capital, WACC • WACC = wdkd(1-T) + wps kps + wcs kcs • wi = the fraction of capital component i used in the firm’s capital structure • What is Merck’s WACC if Merck’s target capital structure of 20% debt, 10% preferred stock, and 70% common equity financing through retained earnings?

Merck’s Weighted Average Cost of Capital, WACC with RE • Recall our previous estimates for Merck • kd(1-T) = 4.2% , kps = 8.3% , kcs = 12.9% • wd = 20% or 0.2, wps = 10% or 0.1, wcs = 70% or 0.7 • WACC = wdkd(1-T) + wps kps + wcs kcs • WACC = 0.2(4.2%) + 0.1(8.3%) + 0.7(12.9%) = 10.7%

Merck’s Weighted Average Cost of Capital, WACC with new Common Stock • What if Merck had to sell new common stock to raise common equity financing? • Recall our previous estimates for Merck • kd(1-T) = 4.2% , kps = 8.3% , kncs = 13.4% • wd = 20% or 0.2, wps = 10% or 0.1, wcs = 70% or 0.7 • WACC = wdkd(1-T) + wps kps + wcs kcs • WACC = 0.2(4.2%) + 0.1(8.3%) + 0.7(13.4%) = 11.1%

How to determine when a firm has to sell new common stock. • This depends on the amount of retained earnings (RE) available and the size of the company’s capital budget. • Maximum Capital that can be Raised with RE = RE/proportion of common equity (wcs). • If the firm’s capital budget exceeds this amount, then new common stock has to be sold and the firm incurs a higher WACC for this excess amount of capital.

How to determine when Merck has to sell new common stock. • Merck’s projected net income = $7.2 billion, projected dividend payout ratio = 45% • Merck’s available retained earnings = $7.2B (1-.45) = $4 billion. Target proportion of common equity financing = 70% or 0.7. • Maximum total financing with RE = $4 billion/0.7 = $5.7 billion. • Merck’s WACC for 0 to $5.7 billion of new capital = 10.7%. • Merck’s WACC for more than $5.7 billion of new capital = 11.1%.

Adjusting for project risk • The WACC is for average risk projects. • A company should adjust their WACC upward for more risky projects and downward for less risky projects = project’s Risk-Adjusted Cost of Capital. • A company can also make this adjustment on a divisional basis as well.

Jordan Air Inc.: a Divisional Cost of Capital Example • Jordan Air is a sporting goods apparel company which has recently divested itself from the sports franchise ownership business. • Jordan Air is starting a golf equipment division to go along with its sports apparel division. • The company uses only debt and common equity financing and thinks they should use a different cost of capital for each division.

Jordan Air Inc.: a Divisional Cost of Capital Example • The company has a 40% tax rate and uses the CAPM method for estimating the cost of equity. • Apparel Division: 35% debt and 65% equity financing. Before-tax cost of debt is 8%. Beta = 1.2. • Golf Division: 40% debt and 60% equity financing. Before-tax cost of debt 8.5%. Estimated beta = to Callaway Golf’s beta of 1.6.

Jordan Air’s Apparel Division’s Cost of Capital Calculation • The company has a 40% tax rate and uses the CAPM method for estimating the cost of equity with Krf = 4.5%, Km = 11%. • Apparel Division: 35% debt and 65% equity financing. Before-tax cost of debt is 8%. Beta = 1.2. • Kc = 4.5% + 1.2(11%-4.5%) = 12.3%. • WACC = WdKd(1-T) + WcsKc • WACC = .35(8%)(1-.4) + .65(12.3%) = 9.7%

Jordan Air’s Golf Division’s Cost of Capital Calculation • The company has a 40% tax rate and uses the CAPM method for estimating the cost of equity with Krf = 4.5%, Km = 11%. • Golf Division: 40% debt and 60% equity financing. Before-tax cost of debt 8.5%. Estimated beta = to Callaway Golf’s beta of 1.6. • Kc = 4.5% + 1.6(11%-4.5%) = 14.9% • WACC = WdKd(1-T) + WcsKc • WACC = .4(8.5%)(1-.4) + .6(14.9%) = 11.0%