Download

1 / 124

1.24k likes | 1.27k Vues

Understand the roles of construction and permanent lenders in real estate financing, their procedures, risks, and liability considerations. Learn how retainage, bonds, and loan administration protect lender interests.

E N D

Construction Lender vs. Permanent Lender(Text p. 587) • Construction lender— “usually a commercial bank primarily interested in making short term, floating rate loans” • “Construction lending is labor-intensive and construction loan departments are usually well-staffed with loan administrators, architects, engineers and inspectors to monitor loan disbursements at every stage of a construction project.” Donald J. Weidner

Construction Lender vs. Permanent Lender (cont’d) • Permanent lender– “usually an insurance company primarily interested in a long term loan, possibly with an equity participation feature.” • “Although two separate sets of instruments . . . may be used, the terms of the permanent loan are often embodied in the construction note and mortgage so that, when construction is completed, the original note will pass from construction lender to permanent lender with no need for execution of a new note by a possibly recalcitrant borrower.” Donald J. Weidner

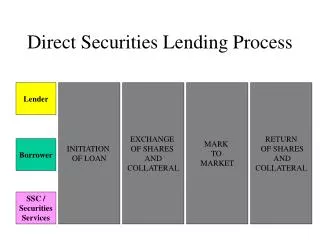

Weller on Fundamentals of Construction Lending (p. 589) • Essence: the construction lender advances funds incrementally, usually on a monthly basis, as construction of improvements is completed. • As materials are purchased and construction proceeds, the contractor will (monthly) submit to the CL an application for progress payments. • “These are typically signed by both the contractor and the contractor’s architect and are reviewed and approved by the owner, lender, and perhaps an inspecting architect.” • Construction “lender funds the amount requested, subject to the retainage requirements and obtaining lien waivers and title insurance” Donald J. Weidner

Weller piece (cont’d) • Lenders do many things to protect their interest. • Retainage—portion of the contract price that is retained by the lender until a certain period of time after work is completed • May be required to minimize the rights of mechanics’ lien claimants • Bonds. An owner and lender may protect their positions with respect to mechanics liens by bonding the job or bonding against specific liens. Properly bonding an entire job at the beginning of a project “generally precludes a mechanic’s lien claimant from filing a suit against the owner or the owner’s property, and relieves the owner of its obligation to retain.” Donald J. Weidner

Weller piece (cont’d) • If a project is bonded and a lien is filed, the specific lien may be bonded against. • Loan Administration. The lender should require lien waivers from all parties receiving proceeds of a loan advance and an affidavit of the general contractor that the loan proceeds have been and will be properly applied. • The lender may also issue dual-payee checks, naming both the general contractor and the subcontractor who should be paid. • We shall consider cases involving the lien priority of disbursements under a construction loan mortgage--a special kind of mortgage for future advances. Donald J. Weidner

Some Lender Liability IssuesConstruction Lender as the disburser of funds is expected to deploy its specialized staff to assure the project is being constructed as planned and that those contributing services and materials are being paid. Permanent Lender – classically, drafts itself as a notepurchaser who takes free of most defenses Borrower Construction Lender Its Draw Inspector Monitors Construction Landseller Fixture financers Mechanics Lien Claimants Members of public Construction Lender Surrounded by Potential Plaintiffs Donald J. Weidner

B Note for $12,000 CL M on bldg. to be constructed partly with loan proceeds B CL CL charges B a fee for “inspection and supervision” [1% of loan proceeds] Rice v. First Federal S & L(Text p. 220) Borrowers are appealing from a judgment of foreclosure on a mortgage they gave to construction lender. Building begins to crumble (shortly after completion) B CL Defaulted on note B CL Sued to foreclose Counterclaimed for damages for negligent inspection B CL [the building began to crumble because of construction defects] Donald J. Weidner

Rice v. First Federal (cont’d) • Court: a construction lender “has an interest in the progress and quality of the construction of its security proportional to the amount of the money invested and would reasonably be expected to inspect the construction and be entitled to additional compensation for its additional costs in making such inspection.” • Does this cut for or against imposing a duty on the lender in favor of the borrower? • Court’s apparent rationale: it is not necessary to impose liability to induce the lender to prevent losses because the lender is already under an economic incentive to engage in loss-avoiding behavior. • Here, the Lender’s agent did inspect the project. Donald J. Weidner

Rice v. First Federal (cont’d) • Did Lender, “by undertaking the inspection of the construction site and requiring [borrowers] to pay a fee therefor, impliedly [contract] with [borrowers] to make such inspection for their benefit?” • See note p. 595 suggesting this might be an “absurd” notion that should be drafted away—specifying that lender’s procedures are for its own benefit and not the benefit of others • If a Lender has a duty to its own shareholders to behave a certain way, should that duty extend to others who may suffer from its breach? • Such as Borrowers • If you expand the beneficiaries of the duty, the shareholders lose, at least in the short run. Donald J. Weidner

Agency • Court concluded that the Lender was not acting as an agent of the Borrower. • Rest. Agency (3d)(2006) suggests the court was correct: “Agency is the fiduciary relationship that arises [a] whenone person (a “principal”)manifests assentto another person (an “agent”) [b] that the agent shall act on the principal’s behalf and [c] subject to the principal’s control, and [d] the agent manifests assent or otherwise consents so to act.” Donald J. Weidner

Fiduciary vs. Contractual Duties • The overarching mandatory obligation in contract is to act in “good faith.” • Stated somewhat differently, contractual provisions must be carried out “in good faith” • In general, the UCC defines good faith as “honesty in fact” • In the case of a merchant , however, the UCC states that good faith requires both: • “[a] honesty in fact and • [b] the observance of reasonable commercial standards of fair dealing in the trade.” Donald J. Weidner

Fiduciary vs. Contractual Duties (cont’d) • The primary fiduciary duties are (a) care and (b) loyalty, with loyalty being very powerful. • It is often easier to establish a breach of a fiduciary duty than of a contractual duty • Burdens are often shifted against those who are classified as fiduciaries • There may be greater remedies for breachof a fiduciary duty than of a contractual duty • Tort remedies, and not merely contract remedies, are often available for breach of fiduciary duties • Including punitive damages. Donald J. Weidner

Good Faith as Gap-Filler Only • In Kham & Nates Shoes (Text p. 218) , Judge Easterbrook stated: “Firms that have negotiated contracts are entitled to enforce them to the letter, even to the great discomfort of their trading partners, without being mulcted for lack of ‘good faith.’ Although courts often refer tothe obligation of good faiththat exists in every contract . . . thisis not an invitation to the court to decide whether one party ought to have exercised privileges expressly reserved in the document. (emphasis added) Donald J. Weidner

Kham & Nates Shoes (cont’d) • Kham & Nates Shoes (continuing the Easterbrook quote): • ‘Good faith’ is a compact reference to an implied undertaking not to take opportunistic advantage in a way that could not have been contemplated at the time of drafting, and which therefore was not resolved explicitly by the parties. When the contract is silent, principles of good faith…fill the gap. Theydo not block use of terms that actually appear in the contract.” (emphasis added) 2. See also Penthouse (Text p. 604). Donald J. Weidner

Jeminson v. Montgomery Real Estate (1973)(Text p. 221) • Lender (“mortgage corporation”) in 1970 “loaned” a member of the “urban poor” the $11,800 purchase price for a home. Lender knew she was on welfare and uneducated. • She gave Lender her note and mortgage, which the Federal Housing Administration insured. • Shortly after she moved in, she realized that the seller had fraudulently misrepresented the condition and value of the property. • She abandoned the house as uninhabitable, stopped paying on the mortgage, whereupon the mortgage was foreclosed. Donald J. Weidner

Jeminson v. Montgomery Real Estate (cont’d) • She then sued Lender, arguing she was unemployed and uneducated, and that Lender “knew or should have known” of the seller’s notorious and unscrupulous business practices. • She argued two lines of authority: 1. The precedent of the Connor case; and 2. The cases that denied holder in due course status to parties who accepted notes either in bad faith or when a legal defect appeared on the face of the instrument • Some of these are known as the “close connectedness” cases. • Consider first the precedent of the Connor case. Donald J. Weidner

Connor v. Great Western S & L( 1968 California case discussed in Jemison at pp. 222 ff.) Homebuyers purchased new homes from a Developer and the homes started to crumble. Homebuyers sued the S & L that provided the construction financing alleging, inter alia, negligent supervision of construction (the design of the homes was inadequate for the soil conditions). • S & L provided Developer land acquisition financing, construction financing and permanent financing for the home buyers. • Developer had no large-scale tract experience. • S & L inspected the construction site at least once a week Donald J. Weidner

Connor v. Great Western S & L (cont’d) • S & L had many sources of return from financing this new development: • Sale/buyback of property by developer to and from the S & L gave the S & L a return on the site acquisition financing • Developer paid S & L a financing charge and interest on the site acquisition loan • Developer paid S & L a financing charge and interest on construction loan. • Homebuyers paid S & L origination fees and interest on the permanent financing (their purchase money mortgages) • Developer paid S & L penalties from the developer if the home buyers obtained their purchase money mortgages elsewhere Donald J. Weidner

Connor v. Great Western S & L (cont’d) • Court concluded: 1) that the Lender had a duty to the homeowners to properly supervise the construction (unlike Rice); and 2) the Lender breached. • Connor was an outlier case. • Jemison distinguished Connor, stating that liability arose in Connor “because lender voluntarily assumed the duty to inspect, andhad become involved in the overall transaction to a far greater extent than the usual lender of money . . . .” Donald J. Weidner

Jeminson (Court of Appeals on Connor) • The Court of Appeals distinguished Connor as follows: • Because Lender in Connor had become an active participantAND either knew or should have known certain facts, Lender came under a duty “to the individual purchasers to exercise reasonable care to prevent them from damages caused by major structural defects.” • Connor sought “imposition of a duty at the point of effective financial control.” Donald J. Weidner

Jemison (Court of Appeals on Connor Cont’d) • Connor imposed liability “because the lender voluntarily assumed the duty to inspect, and had been involved in the overall transaction to a far greater extent than the usual money lender in such transactions.” • Connor, in effect, held the Lender liable as a principal • Interestingly, Connor rejected the idea that the Lender was a partner (or “joint venturer”) with the Developer • There was no division of profits. Donald J. Weidner

Jeminson (Court of Appeals on Connor Cont’d) • There are no facts in Jeminson that suggest that the Lender took an extraordinarily active part. • Indeed, the Jeminson Lender never inspected. Lender had no incentive to inspect: • “[The mortgagee had no real interest in the actual sales transaction. The mortgagee was merely a source of funds, and in the usual course of prudent business practice took a mortgage for the sole purpose of securing its monetary advance to the [borrower]. Given the existence of an FHA insurance policy, the value of the collateral was inconsequential.” • The lender did not “retain any risk”—it had no “skin in the game.” • Should a court impose tort liability to give Lenders an incentive to inform themselves? Donald J. Weidner

Legislative Response to Connor • See the California legislature’s response to Connor (Text p. 226). • “A lender who makes a loan . . . to finance the . . . improvement of . . . property for sale or lease to others, shall not be held liable to third persons for any loss or damage occasioned by any defect in the . . . property . . . unless such loss or damage is a result of an act of the lenderoutside the scope of the activities of a lender of money or unless the lender has been a party to misrepresentations with respect to such . . . property.” Donald J. Weidner

Jeminson (Court of Appeals on whether Lender was on Notice of Seller’s Conduct) • Borrower’s second line of authority was cases denying a note purchaser holder in due course status. • The foreclosed homeowner asserted many allegations of facts that the Lender “knew or should have known”, including • Seller had a notorious reputation for unscrupulous practices; and • Seller charged more than twice what Seller had recently paid for the property. • In holding for the Lender, the Court of Appeals stated: “[T]he transaction in this matter was not unitary, but binary”: there were two transactions, not one: a sale followed by a mortgage. • Recall Professor Barnett’s “Bifurcated Transaction” analysis of Tufts Donald J. Weidner

Jeminson (Court of Appeals on whether Lender on Notice of Seller’s Conduct) • Given that the sale and the mortgage are separate, “any fraud or unconscionability attributable to the purchase agreement cannot be ascribed to the subsequent mortgage agreement.” • The mortgage “itself is neither fraudulent nor unconscionable; for good and valuable consideration, defendant mortgage corporation took a mortgage equal in value to the money advanced to the plaintiff.” Donald J. Weidner

Jeminson Ct. App. Rejects Close-Connectedness Analogy to Put Lender on Notice • Recall that a Holder in Due Course is a holder who takes an instrument: • “(i) for value, and • (ii) in good faith, * * * and • (vi) without notice that any party has a defense or claim in recoupment.” • UCC 3-302(a)(2) (Supplement p. 51) • Arguably, knowledge of shoddy business practices of the seller means that you either • fail to take “in good faith” or • you take with “notice that [a] party has a defense.” Donald J. Weidner

Jeminson Ct. App. Rejects Close-Connectedness Analogy to Put Lender on Notice (cont’d) • It is possible to argue that a “holder” who takes an instrument is so closely connected with the payee that the holder either does not take “in good faith” or takes with “notice” of a defense. • Jeminson cited authority that, to prevail against the holder under the “close connectedness doctrine,” two things are necessary: • (1) an extraordinary discount; and • (2) knowledge by the holder • such as through an infirmity on the face of the instrument. Donald J. Weidner

Jeminson Ct. App. Rejects Close Connectedness (cont’d) • Jeminson said that there was no allegation that the lender was so intimately affiliated with the real estate company that the real estate company’s “fraud could be chargeable against” the lender. • There was “no allegation” that the Lender • Acted as a subsidiary of the [seller], or • Was the Mortgagee of all property sold by the [seller], or • Was otherwise somehow viewable as the alter ego of the [seller]. Donald J. Weidner

Jeminson Ct. App. Rejects Close Connectedness (cont’d) • Finally: “It might be argued that, if the [Lender] did not extend a loan to the plaintiff because she was an uneducated black person, buying a house in an allegedly deteriorating neighborhood, it might incur some legal liability under the Federal Housing Administration Act.” • Recall the much more recent (2001) Associates case. Is this “predatory lending”—a loan that is not suitable for the borrower because there is little chance the borrower will be able to repay? Donald J. Weidner

The Dissent in Jeminson and On Appeal The Dissent made two Major Points: 1. There were allegations that Lender knew, as a result of repeated dealings with the seller, that the seller had a reputation for unscrupulous practices • suggesting a duty to warn or at least to refrain from taking action that would increase the plaintiff’s peril 2. Because there was a subject to financing clause, it was impossible to conclude that the transaction was binary, not unitary. • Citing the reasons in the dissent, the Supreme Court of Michigan in 1976 (p. 225) reversed the award of summary judgment for defendant and remanded. Donald J. Weidner

Jeminson on Remand • From FSU Law Student Mike Fidrych, 2/12/09: I spoke with the attorney who argued the case for the lender (Albert Holtz) earlier today. He explained that the Michigan Supreme Court remanded for fact finding, basically to see "if plaintiffs unsupported allegations were true" and capable of establishing a "close connectedness" style relationship between the lender and the seller of the property. On remand the judge ruled that plaintiff did not establish facts to support the alleged relationship between the lender and seller, and subsequently dismissed the case. Mr. Holtz said "the only evidence the plaintiff had to offer were a few loans made by the lender to the seller over a period of several months." That was the end of the line for Jeminson v. Montgomery Real Estate and Co. Donald J. Weidner

Jeminson: Lender with No Skin in the Game • If a court does not impose tort liability on lenders to give them an incentive to monitor, should regulators provide an incentive to Lenders by requiring them to have some “skin in the game?” • Recall the “misaligned incentives” that gave rise to the mortgage crisis • “Risk retention” has been a part of reform Donald J. Weidner

Shorthand Liability for Construction Defects • Connor and the Supreme Court’s remand in Jeminson are exceptional cases. • In general, the Lender is liable for defects in the premises only in limited circumstances (see Text p. 246): • If Lender and Developer are joint venturers • If a construction lender continues to disburse funds after receiving complaints about defects • If Lender takes over construction upon a default and completes the project • The lender will not become liable for defects in construction simply by taking a deed in lieu of foreclosure and then selling the property. Donald J. Weidner

Buy-Sell Agreements between Construction Lender and Permanent Lender (Text p. 601) Buy-sell agreements usually provide: • Construction lender agrees to sell to the permanent lender, and permanent lender agrees topurchase from the construction lender, a Note and a Mortgage. • Permanent Lender consents to the assignment by the borrower to the Construction Lender of the proceeds to be forthcoming under the permanent loan commitment; • Construction Lender agrees to sell the Note and Mortgage to no one except to the Permanent Lender and to refuse to accept prepayment; • Permanent Lender agrees to buy the Note and Mortgage at par, subject to compliance with the commitment; Donald J. Weidner

Usual Provisions in Buy-Sell Agreements (Cont’d) • The remedies in the event the borrower defaults under the construction loan agreement or under the permanent loan commitment; and • Borrower agrees to comply with the permanent loan commitment and to amend the Mortgage documents if the Permanent Lender requests it, • and the Construction Lender agrees to obtain such amendments from the borrower. Donald J. Weidner

Penthouse Int’l, Ltd. v. Dominion Federal S & L(Text p. 604) Overview Suit is primarily by the Developer, Penthouse, against a participating lender, Dominion, and the Law Firm that represented Dominion. Dominion refused to fund its participation loan and Penthouse sued to enforce Dominion’s loan commitment. • 6/01/83—Penthouse had invested at least $65 million of its own money in a hotel and casino project that was 40% complete. • 6/20/83—Queen City S&L agreed to loan Penthouse $97million forconstructionandpermanent loans, for a ten year term, provided it could get other lenders to participate to the tune of $90 million. • Commitment Expiration Date and Latest Closing Date: in 120 days (roughly 4 months) • 10/20/83—Queen City’s Commitment Expiration Date and Latest Closing Date passed—yet no closing. • 11/21/83—a month later, Dominion S & L decided to participate to extent of $35M. Donald J. Weidner

Penthouse Overview (cont’d) • November 21, 1983—with Dominion deciding to participate, Penthouse and Queen City agree to extend the Commitment Expiration Date to 12/1/83 [for only 10 days?], stating also that the loan Closing Date shall be no later than March 1, 1984 (in a little more than three months) • The court was required to interpret the meaning of a Closing Date that was later than the Commitment Expiration date. • February 9, 1984—Preclosing Meeting: The Melrod Law Firm, acting through its partner, Gorelick, represented participating lender Dominion S & L in a gratuitously caustic way. • March 1, 1984—The March 1 Extended Final Closing Date agreed to by Penthouse and Queen City passed without a closing • Nevertheless, the parties kept trying to work things out. Court Below held: Dominion’s conduct after the February 9. 1984 Preclosing Meeting and before the March 1, 1984 Final Closing Date constituted an anticipatory breach of the loan commitment. Donald J. Weidner

Penthouse –The Specifics Penthouse assembled 5 contiguous parcels: (a) a fee in each of 3 parcels (subject to a declaration of encumbrances that needed to be modified or removed); and (b) a leasehold in each of 2 parcels. 1. The first leased parcel had a Holiday Inn on it. It was obtained from a Harry Helmsley Corporation (“the Helmsley lease”). 2. The second leased parcel had a Four Seasons Hotel on it. It was obtained from the Rothenburgs (“the Rothenburg lease”). Penthouse was going to use the Holiday Inn structure, rebuild the Four Seasons structure, and construct a 7-story building between these two towers. Donald J. Weidner

Initial Commitment Expiration and Closing • Initially, the Commitment Expiration Date was in 120 days, on Oct./20/83, unless mutually extended in writing. The Closing was to have been held on or before the Commitment Expiration Date. • If no Closing by the commitment expiration date, “Lender [Queen City] shall have no further obligation to Borrower.” • Para. 17 said “Lender’s obligation to close the loan [is] contingent upon the satisfaction” of 20 Preclosing Conditions. • Para. 19 of the Preclosing Conditions said: “Lender’s obligation to [close] is also contingent upon execution of a participation agreement between Lender and other lenders pursuant to which said other lenders will participate in making the loan . . . at least to the extent of $90 million on terms . . . satisfactory to the Lender.” • Borrower [Penthouse] was responsible for obtaining participating lenders satisfactory to Lender. Donald J. Weidner

Loan Participation Agreement • Lenders who wished to participate in the syndicate would enter into a “Loan Participation Sale and Trust Agreement” under which the participating lenders would purchase from Queen City (the “Lead Lender”) “undivided participating ownership” interests in the mortgage loan. • Lead Lender was to act, not as an agent, but as an “independent contractor” for the participating lenders and would serve “as a trustee with fiduciary duties” in connection with protecting the rights of the participating lenders. Donald J. Weidner

Dominion’s Participation • November 21, 1983, Dominion decided to participate in the $97 million loan syndicate of 12 financial institutions to the extent of $35 million. • “Dominion ‘accepted’ all of the terms and conditions of both the Loan Commitment and the Participation Agreement except that the Participation Agreement was amended to include Dominion as ‘co-lead seller’ for the syndicate.” • Although Dominion never directly entered into a written agreement with Penthouse, Penthouse paid Dominion an up-front fee of $175,000 for Dominion’s agreement to participate “as a Co-Seller.” Donald J. Weidner

Confusing Extension of “Commitment Expiration” and “Closing” Date[s] • On Nov. 21st, “Penthouse and Queen City mutually agreed to extend the Commitment Expiration Date to Dec. 1, 1983. * * * In addition, [Penthouse and Queen City] agreed that ‘we shall close the loan no * * * later than March 1, 1984.’” • How could the opportunity to close the loan continue after the expiration of Queen City’s commitment to make the loan? • 2d Circuit concluded “that not only was March 1st the closing date, but also that the commitment was extended to and expired on that date,” Donald J. Weidner

Unsatisfied Preclosing Conditions • Once the $97 million syndicate was complete, Penthouse tried to avoid some of the preclosing conditions imposed on it. • Nevertheless, Lead Lender Queen City’s attorney thought that the loan could close. • Lead Lender Queen Citydid not ask Dominion or other participating Lenders to waive compliance with the preclosing conditions. • Instead, Lead Lender Queen City sent the participating lenders a letter declaring substantial progress toward meeting the preclosing conditions and scheduled a preclosing meeting for Feb. 9. [less than a month prior to the March 1 closing deadline] • Meanwhile, Dominion was having trouble selling sub-participation interests in its $35 million share. • It could not legally lend the $35 million itself because it could not loan any borrower more than $18.5 million. • And, prior to the preclosing meeting, the title insurer raised several objections to title on the Helmsley lease. Donald J. Weidner

Basic Commitment To Lien Priority • Court: Penthouse was required to deliver to Queen City “a mortgage on the hotel and casino and the underlying properties.” • Would it be possible for Penthouse to give a mortgage on the two “underlying properties” it did not own in fee? • Or, is a leasehold estate an “underlying property?” • “Penthouse was required to deliver a note secured by a ‘valid first mortgage lien on all real estate owned by [b]orrower covering the project site’ and all improvements thereon and was required to provide a ‘valid first leasehold interest’ in the Rothenburg and Helmsley leasesand ‘a first mortgage covering the improvements thereon.’ Penthouse also was required to provide assignments of its interest in the leasehold estates to be effective in the event of Penthouse’s default.” (Text p. 606) • “Para. 6 required Penthouse to certify at closing that there were ‘no violations’ of the Helmsley or Rothenburg leases.” Donald J. Weidner

The Helmsley Lease 1. The Helmsley lease parcel, with a Holiday Inn on it, was subject to two mortgages, the McShane mortgage and the Chase mortgage, “which needed to be discharged or subordinated before Penthouse could furnish the required security.” • FO 1M McShane • FO 2M Chase • FO Lease Penthouse promise “valid first mortgage lien” • the Lease prohibited further encumbrances • Recall, Penthouse promised the new Lenders a “first mortgage lien” Court: “Unless the McShane and Chase mortgages were discharged or subordinated, if foreclosed upon, they potentially could wipe out the Helmsley lease and any security interest in that lease.” (recall our discussion of subordination in Bolger) Donald J. Weidner

The Helmsley Lease (cont’d) • The closing commitment also required Penthouse to certify that there were “no violations of the lease.” However, there was a clause in the lease prohibiting further encumbrances. Therefore, unless the Helmsley lease were modified, the closing of the loan would itself violate the lease. • In short, there could be no closing without first successfully negotiating with • the 1st Mee, • the 2nd Mee and • the Fee Owner as Lessor (unless the closing conditions were changed or waived). Donald J. Weidner

Other Title Problems/Lack of Progress • There were other title problems with respect to the Rothenburg lease (the Four Seasons Hotel parcel) and with respect to the parcels that were owned in fee (a declaration of encumbrances). • Penthouse’s outside counsel knew that there would need to be negotiations on the title problems, but no negotiations had begun prior to the February 9th pre-closing meeting. • The day before the February 9th pre-closing meeting, the Melrod law firm, through its partner Gorelick, was contacted to represent Dominion (the participating lender and “co-seller” with a $35 million share). Donald J. Weidner

Feb. 9th Preclosing Meeting and Beyond • Lipari, representing Lead Lender Queen City, circulated a “Blumberg” form for a “plain language” mortgage. • The draft mortgage included a rider requiring Penthouse to satisfy each of the preclosing conditions. • Gorelick, representing Participating Lender Dominion, called the documents “idiotic” and said the transaction was not in a position to close. • To satisfy Gorelick’s concerns, Queen City and Penthouse agreed to allow Gorelick and his firm to prepare documents and to review compliance with the conditions • they also agreed to pay his firm’s fees. • Gorelick started requesting documents and information. • March 1 (the commitment expiration and closing date) passed, but the parties kept trying to work things out. • One issue: Did this result in an implied extension of the loan commitment? Donald J. Weidner

The Final Unraveling and the Lower Court • Dominion’s Chairman of the Board said Lead Lender Queen City was in over its head. • Other loan participants started to declare that their commitments had expired. • Court below held that Dominion’s conduct during February and March was an anticipatory breach of the loan commitment. • It said the lease and title problems were “minor” and could have been worked out, in part through a waiver of conditions. • It also found a waiver of some key conditions. Donald J. Weidner

The Lower Court/Second Circuit • Lower court awarded Penthouse $128,000,000 against Dominion and its lawyer, Gorelick’s law firm, who were held jointly and severally liable. • The judgment included 10 years of lost profits on the hotel and casino project • Lower court also awarded $7,000,000 to Queen City. • The Second Circuit reversed, saying that Penthouse must honor the provisions of the contract: • In the guise of construing the terms of an agreement, “court[s] will not make a different or better contract than the parties themselves have seen fit to enter into[.]” Donald J. Weidner