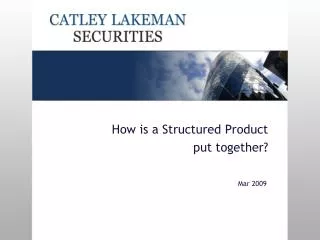

How is a Structured Product put together?

130 likes | 274 Vues

How is a Structured Product put together?. Mar 2009. Content Introduction Example 1 – Zero Coupon Bond + Call Example 2 – Zero Coupon Bond + Geared Call What determines Structured Product pricing? Option pricing summary. Introduction.

How is a Structured Product put together?

E N D

Presentation Transcript

How is a Structured Product put together? Mar 2009

Content Introduction Example 1 – Zero Coupon Bond + Call Example 2 – Zero Coupon Bond + Geared Call What determines Structured Product pricing? Option pricing summary

Introduction Using examples, this presentation aims to illustrate how seemingly complicated structured products can be decomposed into simpler component parts. Having determined the component parts of these sample products, the pricing parameters that determine the value of these Component parts are then discussed.

Example 1 – Zero coupon bond + call In Pictures Option Providing Economic Return GBP1.00 Investor’s Cash GBP1.00 Zero-coupon Bond Share Price at Issue 100.00p Zero-Coupon Bond 75.00p Aggregate Costs 1.50p Option Premium 23.50p

Example 1 – Zero coupon bond + call In Numbers Amount to spend = 100p Zero coupon bond cost = 75p Costs = 1.5p Therefore cash remaining to spend = 100 – 75 – 1.5 = 23.5p Cost of one FTSE atm call option = 23.5p Therefore number of FTSE options bought = 23.5/23.5 = 1 Therefore structured product is 1 x ZCB + 1 x FTSE call

Example 2 – Zero coupon bond + geared call In Numbers Amount to spend = 100p Zero coupon bond cost = 75p Costs = 1.5p Therefore cash remaining to spend = 100 – 75 – 1.5 = 23.5p Cost of one SPX atm call option = 11.75p Therefore number of FTSE options bought = 23.5/11.75 = 2 Therefore structured product is 1 x ZCB + 2 x SPX call

What determines Structured Product pricing? Two Price Components • Zero Coupon Bond Price • Interest rates • Credit • Option Price • Volatility • Time to expiry • Spot price • Strike price • Dividends • Interest rates

What determines Structured Product pricing? Volatility – It’s all about the bell curve!

What determines Structured Product pricing? Or in simple terms! High Implied Volatility Low Implied Volatility

What determines Structured Product pricing? Time to expiry – it’s all about the bell curve – again!

What determines Structured Product pricing? The remaining parameters are: Spot price Strike price Dividends Interest rates These are all used to generate the forward price

Option pricing summary In summary, the input parameters for option pricing break down into the three categories below: Volatility – Most important parameter • Higher vol = more expensive option Time to expiry • Longer dated = more expensive option Forward price • Found using spot, rates and expected dividends

Disclaimer The information in this document is derived from sources believed to be reliable but which have not been independently verified. Catley Lakeman Securities makes no guarantee of its accuracy and completeness and is not responsible for errors of transmission of factual or analytical data, nor is it liable for damages arising out of any person’s reliance upon this information. All charts and graphs are from publicly available sources or proprietary data. The opinions in this document constitute the present judgment of Catley Lakeman Securities, which is subject to change without notice. This document is neither an offer to sell, purchase or subscribe for any investment nor a solicitation of such an offer. This document is intended for the use of institutional and professional customers and is not intended for the use of private customers. This document is not intended for distribution in the United States of America or to US persons. This document is intended to be distributed in its entirety. No consideration has been given to the particular investment objectives, financial situation or particular needs of any recipient. Catley Lakeman Securities is a LLP registered in England and Wales, Registered Office : One Eleven Edmund Street, Birmingham, B3 2HJ. Registration Number: OC336585, Vat Number: 936371705, FSA Reference: 484826