WORKSPACE GROUP PLC

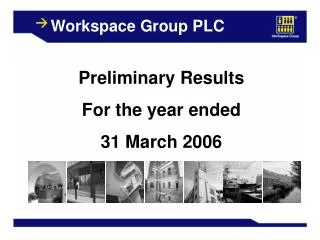

WORKSPACE GROUP PLC. Preliminary Results For the year ended 31 March 2005. Headline results. Valuation Surplus £67m 10.4% Total Property Valuation £718m Up 14.3% Net Asset Value per share £2.24 Up 21.7% Turnover £55.0m Up 7.8% Trading pre-tax profit £14.5m Up 2.6%

WORKSPACE GROUP PLC

E N D

Presentation Transcript

WORKSPACE GROUP PLC Preliminary Results For the year ended 31 March 2005

Headline results • Valuation Surplus £67m 10.4% • Total Property Valuation £718m Up 14.3% • Net Asset Value per share £2.24 Up 21.7% • Turnover £55.0m Up 7.8% • Trading pre-tax profit £14.5m Up 2.6% • Trading EPS per share 6.3p Up 3.3% • Profit before Tax £14.4m Down 4.7% • Annual Rent Roll £42.3m Up 11% • Gearing 88% • Dividend 3.41p Up 10%

Ten Year Results Five Year Ten Year Compound Growth Compound Growth Trading PBT 11.7% 19.6% Trading EPS 9.5% 12.1% Dividend per share 10.2% 13.1% Net Assets (per share) 19.9% 21.6% Property at Valuation 18.7% 24.2%

The Business – A Simple Model • To achieve profit and capital growth from: • Providing workspace to SMEs • Investing in properties with potential • - Income growth • - Capital growth • - Alternative use • Increasing scale of portfolio, spreading overheads and • developing the brand • The right financial platform

Our Business – A Reminder • “ We provide affordable, flexible space for new and small businesses in London and the South East ” • c.4,000 customers over 103 estates; 5.2 million sq .ft • Over 7,700 enquiries a year; market leading brand in • fragmented market • A simple product offer • Superior service from in-house management • Customer focused

Customer Profile Typical Workspace tenant: Rent under 5% of turnover Source: Kingston University survey of over 200 customers. Spring 2004

Trading: Occupancy & Rents • Continuing occupancy improvements • 31 March - core occupancy 90.5% • - overall occupancy 88.3% • - 46% estates at occupancy of 95%+ • 7,764 enquiries in year; 1,012 lettings • Occupancy improving at Barley Mow and Quality Court • Like-for-like average rents up 2.9% (from £8.57 to £8,82) • Rolling rent review/lease renewals programme on 5.8% opening rent roll secured 16.7% uplift on previous passing rentals

Acquisitions & Disposals Disposals Hooley Lane, Redhill Union Street Sites, SE1 Three Mills, E3 £34.8m 2.5% Acquisitions Quadrangle, Fulham, SW6 Southbank House, SE1 Southgate Office Village, N14 Chiswick Studios, W4 Lombard House, Croydon Lewis House, Park Royal, NW10 Homesdale Business Centre, Bromley Total £43.4m Net Yield 7.3%

Recent Acquisitions The Quadrangle, SW6 Chiswick Studios, W4 Southgate Office Village, N14 Homesdale Business Centre, Bromley Southbank House, SE1 Lombard House, Croydon

Progress on Adding Value: Changes of Use • Wharf Road Planning consent achieved. Replacement of 43,000 sq. ft business centre with 77 residential units and new 32,500 sq. ft business centre • Thurston Road 46,400 sq. ft industrial estate to be replaced by 75,000 sq. ft retail warehouse and up to 290 residential units • Aberdeen Studios Planning application in for replacement of existing centre 65,000 sq. ft and up to 96 residential units • Greenheath Planning consent being sought for replacement of existing business centre and 100 residential units • Longer Term Work

2005 Results: Balance Sheet Immediate Investment Capacity = £49.2m (Gearing 102%) (£115.6m to 120%)

Key Elements on Valuation • Income up 4.1%, ERV up 3.3% (like-for-like) • ERV £57.6m; 90% ERV = £51.8m; Current net rental income £42.3m • Net initial yield 5.9%, reversionary yield 8.0%, equivalent yield 7.1% • Valuation surplus after £14.3m impact of stamp duty change • Valuation surplus: 40% rent, 60% yield • Capital value £139 per sq. ft

International Financial Reporting Standards • First impacts annual accounts to 31 March 2006 • Continued quarterly reporting • Q1 August – External Valuation • Impact on EPS and NAV computations (deferred tax, valuation surpluses, financial instruments)

REITs • Origin of Group – earnings focus with high dividend distribution. • On right terms, Group may fit into a REIT environment. • Recent consultation document - thoughts

Looking Forward: The Same Business Model • As stated September 2003 • - 5% per annum rental increases • - No movement in yields/occupancy • - Conservative gearing • - Annual investment £50m - £60m • Aim: - Doubling value in 5 years to September 2008 - £1bn portfolio • On track

Looking Forward: Occupancy and Rents • SME confidence • The London Economy • Short and Longer Term • See: Investor Relations/Company Presentations • section of www.workspacegroup.co.uk

Recent Trends - Starts During 2004, London & South East continue to lead the way in business starts Source: Barclays ‘Starts and Closures’ 2004

Recent Trends – Starts (2) Rise in starts across the Capital during 2004,Though down slightly across the South East Source: Barclays ‘Starts and Closures’ 2004

SME Prospects Expected change during first quarter of 2005(Q1 2005 on Q4 2004) Source: SERT, ‘Quarterly Survey of Small Businesses in Britain’, Q1 2005

Other Longer Term Features • Olympics – decision 6 July • Regeneration Areas • Infrastructure Improvements: Crossrail, East London Line. • Tracking of acquisition targets – our database • Stepping up the added value programme – 45% of estates

Priorities and Performance Performance Priorities Deliver enhanced shareholder value NAV up 21.7%, EPS up 3.3%, TSR 34% per annum over last 5 years To improve occupancy to 90% Occupancy 90% To continue with a further £60m acquisitions in a year Acquisitions - £43m / Disposals - £35m Continue to identify and implement added value schemes Planning/sale achieved: Hooley/Union St Planning achieved: Wharf Road Good Planning Progress: Aberdeen, Thurston Road Strengthen brand awareness as Leader in marketplace Re-launch of Group website, continued link with Kingston University. 7,764 enquiries, 1,012 new lettings

Summary • Good enquiry levels; occupancy high and robust • Rental focus in 2005/06 • Added value programme gaining momentum • Business plan on target • Growth opportunities Workspace – Leader in a Growing Marketplace