Download

1 / 32

390 likes | 1.18k Vues

Learn about factors of production, costs, economic vs. accounting profits, and production functions in this interactive economics chapter.

E N D

http://interactiveeconomicslearning.weebly.com/ economicsCHAPTER 4 : THEORY OF PRODUCTION and cost

INTRODUCTION • This part is focuses on the supply side of the market • So, the agent for supply is producer • Factors of production is very important as the input in a production process • What is production? • Production is defined as a process of transforming the factors of production to output

FACTORS OF PRODUCTION Using conventional perspectives there are 4 types of factors of production: a) Land • Natural resources b) Capital • 2 types of capital: i) Capital goods ii) Consumer goods (finished/final goods)

Labor • Physical and mental talents of men and women d) Entrepreneurship • Specific human resources that is responsible in ensuring the smooth flow in the production process 2. Islamic perspectives • Land • Wherever Man can work on this globe • Labour • To extract most of the goods of earth as well as getting wealth • Capital - Continuation of work obtaining wealth

PRODUCTION AND COSTS Production cost • Production: is a process of transforming production factors or inputs into goods and services. • Costs: are payments to inputs used in the production process. • Inputs are classified into fixed inputs and variable inputs. • Costs are classified into explicit and implicit costs. Explicit cost is visible, out of pocket cost. Explicit cost is further classified into fixed and variable costs.

PRODUCTION AND COSTS Production Cost • Implicit cost is the opportunity cost of producer’s own inputs used in the production process. TotalFixed Cost (TFC) and Variable Cost (TVC) • TFC is incurred on fixed inputs, for example the cost of a business premise. TVC is incurred on variable inputs, for example the wages of the workers.

PRODUCTION AND COSTS Production Cost Costs are also categorized into accounting and economic costs • i) Economic Costs (EC) = Explicit cost (ExC) + Implicit cost (IC) or Opportunity cost (OC). • Since ExC = TFC + TVC, therefore, EC = TFC + TVC + IC/OC • ii) Accounting cost (AC) refers to only explicit cost. Thus, AC= ExC =TFC + TVC. So, economic cost > accounting cost.

PRODUCTION AND COSTS Economic profit and accounting profit • A rational producer aims to maximize profits from production. • There are 2 different concepts of profits; Economic Profit (EP) and accounting profit (AP). • Total profit (TP) = Total revenue (TR) – Total cost (TC). • So, • Economic profits (EP) = Total revenue – (Explicit + Implicit Costs) = TR – (TFC + TVC + IC/OC) • Accounting profits (AP) = TR – (TFC + TVC). Thus, AP is < EP

PRODUCTION AND COSTS ILLUSTRATION: Accounting and Economic Profit

THEORY OF PRODUCTION • Theory of production explains the relationship between output and input. • Production can be defined as an activity to convert inputs into outputs which can be used by the ultimate user. • The main objective of producer engaging in production activities: • To maximize the profit and minimize costs. • To maximize sale • To maximize total revenue • To acquire largest market share • To ensure company’s growth and stability

PRODUCTION FUNCTION • Production process involves utilization of various inputs combination. • In the short-run, there are 2 types of input: • Variable input – any resource for which the quantity can change during the period of time under consideration. • Fixed input – any resource for which the quantity cannot change during the period of time under consideration

Production Function in the Short-Run • Production function refers to the relationship between input and output. • Production function refers to the relationship between the maximum amounts of output that a firm can produce and various quantities of inputs. • Assumptions: • In the production of a good (Q), we used only 2 types of factors of production, land (L) and labor (K) Q = f (L,K) • Labor must be of the same level of efficiency (equal job skills) • Constant/fixed technology level

Total product (TP) Total product is the output that can be produced using certain level of variable input.

Average product (AP) - AP is output per labor (also called as labor productivity). - AP is calculated by dividing TP (column 3) by the number of labor (column 2). • Marginal product (MP) - MP shows the change in total product produced by adding one unit of a variable input (labor). - MP is calculated by dividing change in TP by the change in number of labor.

Stages of Production • These stages of production will be related to the efficiency of using inputs of production.

Stage 1 (increasing returns to a factor) • Stage 2 (decreasing returns to a factor) • Stage 3 (negative returns to a factor) • Relationship between TP and MP: • When MP is increasing, TP is increasing at an increasing rate • When MP is falling, TP is increasing at a decreasing rate • When MP is at zero, TP is at the maximum • When MP is negative, TP is falling • Relationship between AP and MP: • When MP is increasing, AP is increasing • MP cuts AP at the latter’s maximum point • When MP is above AP, AP is rising • When MP is below AP, AP is falling

Law of Diminishing Returns • It is also called the law of diminishing marginal product. • The law states that beyond some point the marginal product decreases as additional units of a variable input are added to a fixed input.

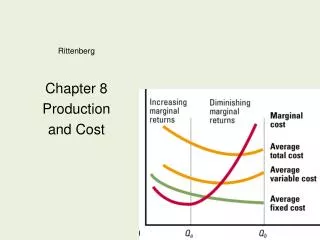

COST OF PRODUCTION AND REVENUE • Cost of production is an expense incurred by a firm due to the utilization of economic resources in production activities. SHORT-RUN COST • Total fixed cost (TFC) Costs that do not vary as output varies and that must be paid even if output is zero. Examples are factory, machinery, tools, insurance premium, rent and utility bills. TFC = TC - TVC

Total variable cost (TVC) Costs that are zero when output is zero and vary as output varies. Examples include wages for workers, electricity, fuel and raw materials. TVC = TC – TFC • Total cost (TC) TC is the sum of TFC and TVC at each level of output. TC = TFC + TVC TC = ATC x Q

Average fixed cost (AFC) AFC can be defined as total fixed cost per unit of output. AFC = TFC/Q AFC = ATC – AVC • Average variable cost (AVC) AVC can be defined as the total variable cost per unit of output. AVC = TVC/Q AVC = ATC - AFC

Average total cost (ATC) ATC can be defined as the total cost per unit of output. ATC = TC/Q ATC = AFC + AVC • Marginal cost (MC) MC can be defined as the change in TC when one additional unit of output is produced. MC = change in TC change in Q

MC curve ↓ at first, then reaches a minimum, and then increases as output increases. • MC curve intersects both AVC curve & ATC curve at the minimum point on each of these cost curves, A & B respectively. • AVC and ATC are U-shaped due to law of diminishing return. • The AFC curve declines continuously as output expands. • The TC at each level of output is the sum of TVC and TFC • Because the TFC curve does not vary with output, the shape of the TC curve is determined by the shape of the TVC curve. • The vertical distance between the TC and the TVC curves is TFC.

The relationships between ATC and MC are: • When ATC is falling, MC is below it • When ATC is rising, MC is above it • When ATC is falling, MC is falling, then rising • When MC cuts ATC, it is at the minimum point of ATC

LONG-RUN PRODUCTION COSTS • The long run is a time period long enough to change the quantity of all fixed inputs. • The long run is a period where there are only variable factors. There is no fixed factor. Long-Run Average Cost Curves

ECONOMIES AND DISECONOMIES OF SCALE • We can explain the U-shaped LRAC curve in terms of economies and diseconomies of large-scale production. Economies of Scale • Economies of scale refer to a situation in which the LRAC curve declines as the firm increases output. • As plant size increases, average costs production decreases.

Economies of scale can be divided into 2 types: • Internal economies of scale - benefits enjoyed by the firm because the growth and efficiency in the firm itself • External economies of scale - benefits enjoyed by the firm because of the growth in the entire industry

Internal economies of Scale • Labor specialization • Financial economies • Marketing economies External economies of scale • Economies of concentration • Marketing economies • Economies of information

Diseconomies of Scale • Diseconomies of scale refer to a situation in which the LRAC curve rises as the firm increases output. • As plant size increases, average costs production increases.

Diseconomies of scale can be divided into 2 types: • Internal diseconomies of scale - inefficiency experienced by the firm because of the problems in the firm itself • External diseconomies of scale - inefficiency experienced by the firm because of the problems in the entire industry

Internal diseconomies of scale: • Managerial problems • Technological problems • Input problems External diseconomies of scale • Social problems • Wage differential

THANK YOU! THE END