Download

1 / 19

190 likes | 303 Vues

This document provides an in-depth analysis of bond pricing, incorporating key concepts like coupon payments, yield to maturity, and holding period returns. It discusses how bond prices fluctuate based on interest rates, including the distinction between premium and discount bonds. The framework of expectations theory and liquidity premium further elucidates the complexities in the bond markets. Alongside numerical examples, it helps investors understand the implications of bond yields, risks, and pricing mechanisms, equipping them to make informed investment decisions.

E N D

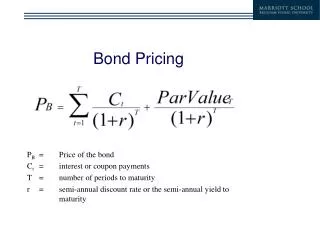

Bond Pricing PB = Price of the bond Ct = interest or coupon payments T = number of periods to maturity r = semi-annual discount rate or the semi-annual yield to maturity

Price of 8%, 10-yr. with yield at 6% Coupon = 4%*1,000 = 40 (Semiannual) Discount Rate = 3% (Semiannual) Maturity = 10 years or 20 periods Par (Face) Value = 1,000

Holding Period Return • What is the price of the bond in 6 months time (ex-coupon), and what was the holding period return over that time?

Premium and Discount Bonds • Premium Bond • Coupon rate exceeds yield to maturity • Bond price will decline to par over its maturity • Discount Bond • Yield to maturity exceeds coupon rate • Bond price will increase to par over its maturity

Prices and Yield to Maturity • YTM is discount rate that sets PV of bond cash flows equal to current market price Price Yield

Yield to Maturity Yield to maturity = interest rate that equates today’s value with present value of all future payments • Need Today’s Price or ‘Value’ to find implicit interest rate • Like Internal Rate of Return

Current YieldCoupon Bonds • Is better approximation to yield to maturity, nearer price is to par and longer is maturity of bond • Change in current yield always signals change in same direction as yield to maturity

Yield to Maturity Yield on a Discount Basis or Bank Discount Yield Yields on Discount Instruments Yield Measure Annualization

Alternative Measures of Yield • Yield to Call • Call price replaces par • Call date replaces maturity • Holding Period Yield (actual return) • Considers actual reinvestment of coupons • Considers any change in price if the bond is held less than its maturity • Realized Compound Yield • Reinvestment rate of coupons

Default Risk • Agency Assessment • Coverage ratios • Leverage ratios • Liquidity ratios • Profitability ratios • Cash flow to debt • Company’s Protection Against • Sinking funds • Subordination of future debt • Dividend restrictions • Collateral

Term Structure of Interest Rates • Relationship between yields to maturity and maturity • Yield curve - a graph of the yields on bonds relative to the number of years to maturity • Usually Treasury Bonds • Have to be similar risk or other factors would be influencing yields

Expectations Hypothesis Key Assumption: Bonds of different maturities are perfect substitutes Implication: Expected Return on bonds of different maturities are equal For n-period bond: yt + yt+1 + yt+2 + ... + yt+(n–1) ynt = n In words: Interest rate on long bond = average short rates expected to occur over life of long bond Numerical example: One-year interest rate over the next five years 5%, 6%, 7%, 8% and 9%: Interest rate on two-year bond: (5% + 6%)/2 = 5.5% Interest rate for five-year bond: (5% + 6% + 7% + 8% + 9%)/5 = 7% Interest rate for one to five year bonds: 5%, 5.5%, 6%, 6.5% and 7%.

Liquidity Premium Theory Key Assumption: Bonds of different maturities are substitutes, but are not perfect substitutes Implication: Modifies Expectations Theory with features of Segmented Markets Theory Investors prefer short rather than long bonds must be paid positive liquidity (term) premium, lnt, to hold long-term bonds Results in following modification of Expectations Theory yt + yet+1 + yet+2 + ... + yet+(n–1) ynt = + lnt n

Relationship Between the Liquidity Premium and Expectations Theories

Theories of Term Structure • Expectations • Long term rates are a function of expected future short term rates • Upward slope means that the market is expecting higher future short term rates • Downward slope means that the market is expecting lower future short term rates • Liquidity Preference • Upward bias over expectations • The observed long-term rate includes a risk premium

Innovations in the Bond Market • Reverse floaters • Asset-backed bonds • Pay-in-kind bonds • Catastrophe bonds • Indexed bonds • TIPS (Treasury Inflation Protected Securities)