Chapter 23 Bond Pricing

Chapter 23 Bond Pricing. Fabozzi: Investment Management Graphics by. Learning Objectives. You will learn how to calculate the price of a bond. You will understand why the price of a bond changes in the direction opposite to the change in required yield.

Chapter 23 Bond Pricing

E N D

Presentation Transcript

Chapter 23Bond Pricing Fabozzi: Investment Management Graphics by

Learning Objectives • You will learn how to calculate the price of a bond. • You will understand why the price of a bond changes in the direction opposite to the change in required yield. • You will study why the price of a bond changes. • You will be able to calculate the yield to maturity and yield to call of a bond. • You will explore and evaluate the sources of a bond’s return.

Learning Objectives You will discover the limitations of conventional yield measures. You will calculate two portfolio yield measures and explain the limitations of these measures. You will be able to calculate the total return for a bond. You will study why the total return is superior to conventional yield measures. You will learn how to use scenario analysis to assess the potential return performance of a bond.

Introduction Bonds make up one of the largest markets in the financial world. In the previous chapter we discussed the myriad types of bonds. Here we will discover how to price them and their relationships to yield and return. Since bonds usually have clear beginning and ending times, they can be easier to value than stocks.

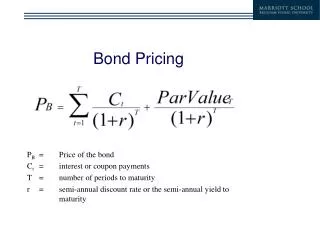

Pricing of bonds In order to determine the present value of the future cash flows it is necessary to have an estimate of those flows, and an estimate of the appropriate required yield. Required yield = reflects yield of alternative or substitute investments and is determined by looking at the yields of comparable bonds in the market (quality and maturity) Non-callable bond consists of coupon and maturity value, which translates to calculating the annuity value of the coupon plus the maturity value. We will employ the following assumptions: -Coupons are payable every 6 months -Next coupon payment is exactly 6 months from now -Coupon interest is fixed for life of bond

Pricing of bonds We need to find 1) the present value of the coupons and 2) the present value of the par value. Given: P = price (in $) n = number of periods (number of years x 2) C = semiannual coupon payment (in $) r = periodic interest rate (required annual yield x 2) M= maturity value t = time period when the payment is to be received with the present value of the coupon payments found by the following annuity formula

Pricing of bonds: an example A 20-year, 10% bond has a required yield of 11%.. Therefore, there will be 40 semiannual coupon payments of $50, with a maturity value of $1,000 to be received 40 six-month periods from now. r = 5.5% (11%/2) C = $50 n = 40 Bond price = 802.31 + 117.46 = $919.77

Pricing of bonds: zero-coupon bonds Zero-coupon bonds do not make any periodic payments. The following adjustments must be made: n = doubled r = required annual yield/2

Price/yield relationship There is an inverse relationship between a bond price and yield. Recall that a bond price equals the present value of its cash flows. As r increases, the present value decreases, with a corresponding increase in price. This relationship results in a convex or bowed out shape. Insert Figure 23-1

Relationship between coupon rate, required yield, and price Since coupon rates and maturity terms are fixed, the only variable is the price of the bond which moves in response to changes in the relationship between the coupon and the required yield. Coupon = required yield sells at par Coupon < required yield sells at a discount to par Coupon > required yield sells at a premium to par

Relationship between bond price and time if interest rates are unchanged Bond at par – continues to sell at par towards maturity Discount bond – price rises as bond approaches maturity Premium bond – price falls as bond approaches maturity At maturity, all bonds will equal par.

Reasons for the change in the price of a bond 1.Required yield changes due to changes in the credit quality of the issuer 2.As bond moves toward maturity, yield remain stable but price changes if selling at a discount or premium 3.Required yield changes due to a change in market interest rates

Complications Assumptions: 1.Next coupon payment is exactly 6 months away 2.Cash flows are unknown 3.One discount rate for all cash flows What if these assumptions did not hold?

Assumption #1 To compute the value of this bond, we use the following formula: where v = days between settlement and next coupon days in six month period

Assumption #2 & #3 Assumption #2 Issuer may call bond before maturity date If interest rates are lower than the coupon rate, it is to the issuer’s benefit to retire the debt and reissue at the lower rate. Assumption #3 Technically, each cash flow should have its own discount rate.

Price quotes Prices are quoted as a value of par. Converting a price quote to a dollar quote: (Price per $100 of par value/100) x par value Price quote of 96 ½, with a par value = $100,000 (96.5/100) x $100,000 = $96,500 Price quote of 103 19/32, with a par value = $1 million (103.59375/100) x $1 million = $1,035,937.50

Accrued interest If bond is bought between coupon payments, the investor must give the seller the amount of interest earned from the last coupon till the settlement date of the bond. Bonds in default are quoted without this accrued interest, or at a flat price.

Conventional yield measures Current yield Yield to maturity Yield to call

Current yield Current yield = annual dollar coupon interest Price This method ignores any capital gain or loss as well as the time value of money.

Yield to maturity Yield to maturity (y)- the interest rate that makes the present value of remaining cash flows = price (plus accrued interest). The formula for a semiannual y is To annualize it either double the yield or compound the yield. The popular bond-equivalent yield uses the former method. This formula requires a trial and error approach, where you plug in different rates until the equation balances. Insert Table 23-2

Yield to call Callable issues have a yield to call in addition to a yield to maturity. The yield to call assumes the bond will be called at a particular time and for a particular price (call price). Yield to first call – assumes issue will be called on first call date Yield to par call – assumes issue will be called when issuer can call bond at par value Yield to call formula given: M * = call price (in $) at assumed call date n* = number of periods until assumed call date yc = yield to call The lowest yield based on all possible call dates and the yield to maturity is the yield to worst

Potential sources of a bond’s dollar return 1.periodic coupon payments 2.income from reinvestment of interest payments (interest-on-interest) 3.capital gain (loss) when bond matures, is called, or is sold Yield to maturity is only a promised yield and is realized only if Bond is held to maturity Coupon payments are reinvested at the yield to maturity Yield to call considers all three sources listed above and is subject to the assumptions inherent in them.

Determining the interest-on-interest dollar return Given r= semiannual investment rate, the formula is With total coupon interest = nC, the final formula looks like

Determining the interest-on-interest dollar return: an example Consider a 15 year, 7% bond with yield to maturity of 10%. Annual reinvestment rate = 10% (semiannual = 5%). What is the interest-on-interest?

Yield to maturity and reinvestment risk An investor can achieve the yield to maturity only if the bond is held to maturity and then the proceeds are reinvested at the same rate. Reinvestment risk occurs when rates are lower when the bond is sold than the yield to maturity when it was purchased. Greater reinvestment risk if there is… Long maturity – bond’s return heavily dependant on interest-to-interest High coupon – bond is more dependent on interest-tointerest Zero coupon bond has no reinvestment risk.

Portfolio yield measures Weighted average portfolio yield Internal rate of return

Weighted average portfolio yield Using the weighted average to calculate portfolio yield is a flawed, yet common method. Given: wi = the market value of bond i relative to the total market value of the portfolio y i = the yield on bond i K = the number of bonds in the portfolio The formula is = w 1y 1 + w 2 y 2 + w3 y 3 + …+ w K y K

Weighted average portfolio yield w1 = 9,209,000/57,259,000 = 0.161 y1 = 0.090 w2 = 20,000,000/57,259,000 = 0.349y2 = 0.105 w3 = 28,050,000/57,259,000 = 0.490 y3 = 0.085 Weighted average portfolio yield = 0.161(0.090) + 0.349(0.105) + 0.490(0.085) = 0.0928 = 9.28% Insert Table 23-4

Portfolio internal rate of return Compute the cash flows for all bonds in the portfolio and then using trial and error, find the rate that makes the present value of the flows equal to the portfolio’s market value. Using the example in Table 23-4, we find the rate to be 4.77%. On a bond-equivalent basis, the portfolio’s internal rate of return = 9.54%. This method assumes that cash flows can be reinvested at the calculated yield and that the portfolio is held until the maturity of the longest bond in the portfolio.

Total return Total return = measure of yield that assumes a reinvestment rate Insert Table 23-6 Which bond has the best yield? The answer depends upon the rate where proceeds can be reinvested and on investor’s expectations.

Computing the total return for a bond Step 1: Compute total coupon payments + interest-on-interest based on the assumed reinvestment rate (1/2 the annual interest rate that is predicted to be reinvestment rate) Step 2: Determine projected sale price which depends on the projected required yield at the end of the investment horizon Step 3: Sum steps 1 and 2. Step 4: Semiannual total return computation given h = number of 6 month periods in the investment horizon Step 5: Annualize results of step 4 to obtain the total return on an effective rate basis. (1 + semiannual total return)2 - 1

Computing the total return for a bond: an example Step 1: Assume annual reinvestment rate = 6%, coupon payments = $40/six months for 3 years. Total coupon interest plus interest-on-interest =$258.74 Step 2: Assume required yield to maturity for 17 year bonds = 7%. Calculate present value of 34 coupon payments of $40 each, plus maturity value of $1,000 discounted at 3.5%. Sale price = $1,098.51 Step 3: $1,098.51 + $258.74 = $1,357.25 Step 4: Semiannual total return = (1,3725/828.40) 1/6 – 1= 8.58% Step 5: 8.58% x 2 = 17.16% (1.0858)2 –1 = 17.90%

Applications of total return (horizon analysis) Horizon analysis is the use of total return to assess performance over an investment horizon. The resulting return is called the horizon return. Horizon analysis allows the money manager to analyze the performance of a bond under various scenarios, given different market yields and reinvestment rates. Insert Table 23-7