Download

1 / 18

180 likes | 368 Vues

Disparate Impact Discrimination and Community Banks. March 5, 2013. Presented by Frank C. Bonaventure, Jr. Andrew F. Campbell. Introduction. What is disparate impact discrimination? Why is it especially important now? What should you do to protect your institution?.

E N D

Disparate Impact Discrimination and Community Banks March 5, 2013 Presented by Frank C. Bonaventure, Jr. Andrew F. Campbell

Introduction • What is disparate impact discrimination? • Why is it especially important now? • What should you do to protect your institution?

Prohibited Bases under ECOA and FHA Equal Credit Opportunity Act • race or color • religion • national origin • sex • marital status • age • applicant receives public assistance • applicant exercises a right under the Consumer Credit Protection Act • Fair Housing Act • race or color • religion • sex • handicap • familial status • national origin

Covered Transactions ECOA – All aspects of a credit transaction for consumer and commercial loans • Applications • Customer assistance during the application process • Underwriting • Servicing • Collections • May apply to assignees under certain circumstances • May also cover real estate brokers, automobile dealers, home builders, and home-improvement contractors • FHA – • Loans to purchase, construct, improve, repair, or maintain a dwelling • The sale or rental of housing • brokering or appraising residential real property

Types of Discrimination • 1994 Policy Statement issued by 11 Federal agencies outlined 3 types of discrimination • Overt Discrimination • Disparate Treatment • Disparate Impact

Overt and Disparate Treatment Overt Discrimination– Examples • Credit Offer – lender offers a credit card with a limit of up to $750 for applicants age 21–30 and $1,500 for applicants over 30. • Fees and Pricing – lender charges minority applicants a higher application fee than it charges non-minority applicants, and loans that it makes to minority applicants carry interest rates that are 2 to 3 points higher than loans made to non-minority borrowers with similar credit profiles. Disparate Treatment – occurs when a lender treats a credit applicant differently on the basis of one of the prohibited factors • Different levels of effort and assistance to applicants • Offering different products and services • Redlining – an example of a non-neutral policy

Disparate Impact Discrimination Disparate impact. A disparate impact occurs when a lender applies a neutral policy or practice equally to all credit applicants but the effect of the policy or practice can be shown by statistical analysis to disproportionately exclude or burden applicants on a prohibited basis. Example • A lender’s policy is to deny loan applications for single-family residences for less than $60,000. The policy has been in effect for ten years. This minimum loan amount policy is shown to disproportionately exclude potential minority applicants from consideration because of their income levels or the value of the houses in the areas where they live. Generally, if a borrower can show that a lender’s policy has a statistically significant disparate impact on a protected class, the lender then must show that the policy or practice is justified by a business necessity and that there is not a readily available non-discriminatory alternative that would accomplish the same purpose.

Recent Disparate Impact Cases Disparate impact cases have typically involved neutral policies that result in higher prices and fees for individuals protected by ECOA and FHA • Countrywide – policy gave loan officers and mortgage brokers discretion over interest rate and fees. Statistical analysis allegedly showed that over 200,000 African-American and Hispanic borrowers were charged higher fees and interest rates and were steered into subprime loans. $335 million settlement is the largest in history. • Wells Fargo – mortgage brokers were given pricing discretion; statistical analysis allegedly showed that African-Americans and Hispanic borrowers in the Chicago area were charged an average of $2,937 and $2,187, respectively, than nonminority applicants with the same credit profile. Wells Fargo settled to avoid a costly legal battle. • SunTrust - loan officers and mortgage brokers in SunTrust’s 200 retail offices were allowed to vary a loan’s interest rate and other fees from the price it set based on the borrower’s objective credit-related factors. DOJ’s investigation lasted 2 ½ years and analyzed more than 850,000 loans originated between 2005 and 2009.

Other Disparate Impact Scenarios • Most recent ECOA cases involve discretionary pricing policies • Other uses of subjective, rather than objective, criteria in the loan approval process, e.g., • Loan Committee • Analyses of business plans • Steering • Establishment of interest reserves and other conditions to approval • Loan minimums • Geographical grading systems • Collections • (FHA) – • mobile home occupancy limits • Land use, zoning, and withdrawal from the Section 8 program

Heightened Regulatory Attention Consumer Financial Protection Bureau • Disparate Impact Analysis in Fair lending Cases • CFPB Bulletin 2012-04 (Fair Lending) (April 18, 2012) • Fully embraces the use of disparate impact analysis in lending discrimination cases • December 6, 2012 Memorandum of Understanding with the Department of Justice for information sharing and joint enforcement; coordination with DOJ on enforcement priorities • Active participation in Federal Financial Fraud Enforcement Task Force’s Non-Discrimination Working Group and Federal Interagency Task Force on Fair Lending with bank regulators • Data-driven examination procedures • State of the art consumer complaint system • Fair lending staff member assigned to each examination of banks and non-banks

CFPB Enforcement “CFPB’s Fair Lending and Enforcement offices have a number of pending fair lending investigations, including matters arising from the CFPB’s supervisory activity and joint investigations with other federal agencies. While the details of ongoing investigations are confidential, the CFPB’s conclusions will typically be made public if an enforcement action is filed at the conclusion of an investigation.” Fair Lending Report of the Consumer Financial Protection Bureau (December 2012) • Next area of enforcement may be discretionary pricing by auto dealerships involved in originating auto loans • CFPB has shown a willingness to set new universally applicable policy through enforcement action • “Tornado” approach to enforcement gives defendants little choice but to enter into settlements

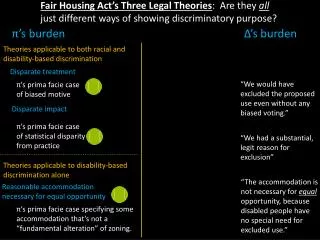

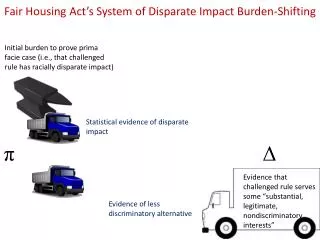

HUD On February 8, 2013, issued a Final Rule formalizing “HUD’s long-held interpretation of the availability of [disparate impact] liability under the Fair Housing Act.” 78 Fed. Reg. 11460 (Feb. 15, 2013) • formally establishes the three-part burden-shifting test currently used by HUD and some federal courts • Fair Housing Act is violated by facially neutral practices that have an unjustified discriminatory effect on the basis of a protected characteristic, regardless of intent • makes clear that a lender’s facially neutral policy allowing employees and mortgage brokers the discretion to price loans may be actionable under the Fair Housing Act • does not explain the degree to which a practice must disproportionately impact one group over another; leaves open the possibility that statistically small variances may still lead to liability

HUD Final Rule • Discriminatory effect – A practice has a discriminatory effect where it actually or predictably results in a disparate impact on a group of persons or creates, increases, reinforces, or perpetuates segregated housing patterns because of race, color, religion, sex, handicap, familial status, or national origin • Three-part burden-shifting test – • charging party bears the burden of proving its prima facie case that a practice results in, or would predictably result in, a discriminatory effect on the basis of a protected characteristic • If the charging party proves a prima facie case, the burden of proof shifts to the respondent or defendant to prove that the challenged practice is necessary to achieve one or more of its substantial, legitimate, nondiscriminatory interests • If the respondent or defendant satisfies this burden, then the charging party or plaintiff may still establish liability by proving that the substantial, legitimate, nondiscriminatory interest could be served by a practice that has a less discriminatory effect

The Supreme Court – Gallagher • Magner v. Gallagher – Plaintiffs sued St. Paul, Minnesota under the FHA, alleging that City’s aggressive and targeted housing code enforcement against rental properties reduced the availability of such housing and had a disparate impact upon African-Americans • Issue in the case is whether disparate impact discrimination is a valid claim under the FHA; St. Paul argued that the statutory text of the FHA prohibits intentional discrimination only • The Supreme Court has signaled that disparate impact claims are only permitted in employment cases brought under Title VII of the Civil Rights Act, which prohibits both intentional discrimination in the employment context and actions that may have a discriminatory effect on an employee or applicant. Smith v. City of Jackson, 544 U.S. 228 (2005) • The FHA and ECOA lack this “discriminatory effects” language • Magner v. Gallagher was scheduled to be heard by the Supreme Court but the City of St. Paul withdrew its appeal before oral argument

The Supreme Court – Mt. Holly • Township of Mount Holly v. Mt. Holly Gardens Citizens in Action, Inc. – Township proposed a redevelopment plan that would eliminate the existing homes in a neighborhood occupied predominantly by low-income residents, and replace them with significantly more expensive housing units • Issues Presented – • Whether disparate impact claims are cognizable under the FHA • if such claims are cognizable, what is the appropriate burden-shifting test • what is he correct test for determining whether a prima facie case of disparate impact has been made • how should the statistical evidence be evaluated; and • what the correct test is for determining when a defendant has satisfied its burden in a disparate impact case • Currently before the Court; a finding for the Township would be a direct refutation of HUD and its final rule

An ounce of prevention . . . Self-Assessment • Does your institution have policies relating to – • Qualification standards? • Application procedures and processing? • Customer service? • Underwriting? • Branch management and autonomy? • Loan servicing? • Collections? • Are there any aspects of these policies that might adversely affect a protected class of borrowers? Remember to consider all protected classes • At what points in the credit process do subjective factors come into play? • Do any individuals have discretion to make exceptions to policy? How is that discretion exercised?

Regular Reviews Conduct regular reviews, through the compliance and audit functions, of • Internal controls • Policies • Branch operations and LO compensation • Data collection and integrity • Records • Training

Self-testing • Analysis of HMDA data, either internally or through third-party vendor • Regression analysis to look for disparities in denials, pricing • Analyze activity by branch and LO • If problems are found, take appropriate corrective action • Maintain confidentiality and limited access to reports and work papers in order to maintain privilege