SWIFT for Payment Market Infrastructures

210 likes | 703 Vues

SWIFT for Payment Market Infrastructures . An efficient platform to support your payment systems transformation . Mr. Paul Landvogt, Equens Mr. Ed Kelsey, Bank of England Mr. Stéphane Ernst, SWIFT 27 October 2010 14:00 – 14:45. Agenda.

SWIFT for Payment Market Infrastructures

E N D

Presentation Transcript

SWIFT for Payment Market Infrastructures An efficient platform to support your payment systems transformation Mr. Paul Landvogt, Equens Mr. Ed Kelsey, Bank of England Mr. Stéphane Ernst, SWIFT 27 October 2010 14:00 – 14:45

Agenda SWIFT for PMIs - 27 October 2009

Key challenges of the payments market infrastructure ecosystem How to mitigate systemic risk? How to manage my collateral efficiently? Central bank Do I have the right risk/cost balance per payment? CSD Govt Entities High-value payment MI How to secure settlement finality? How to achieve cost reduction & scale business? ACH How to reach my counterpart? Participants Participants Direct Participants Direct Participants How to transfer funds quickly at low cost? Low-value payment MI Indirect Participants How to optimise my liquidity? Corporates Consumers SWIFT for PMIs - 28 October 2009

Trends in Payments Market Infrastructures SWIFT response… • High operational availability for messaging & RTGS • Liquidity and collateral control • Security, non-repudiation, delivery notification, • Role-based access control • Regulatory reporting • Global reach • Single platform • Direct and indirect • Bilateral or multilateral • Copy services (Y-/T) • SWIFT messaging MT or MX • Standards ISO2022 • Market Practice groups • E2E business modeling • Standards validation • Multi-payment scheme and instrument support • Any format & channels (m-/e- payments) • Payment instructions, cash management and reporting • Application-to-application or user-to-application • Reference data • Message price reduction by an average 20% • Reduced TCO – standard messaging protocol • Services to ease implementation SWIFT for PMIs - 28 October 2009

SWIFT’s 5-pillars offering for Payment Market Infrastructures Your Payment Market Infrastructure system Standards Messaging Security Integration Services MT messages MX (ISO20022) Market practices Consulting Implementation Project Management Training Customer support FIN, InterAct FileAct, Browse Copy PKI HSM Delivery notification Multi-site Alliance Interfaces Integration tools Alliance Connect Bronze/Silver/Gold A comprehensive solution SWIFT for PMIs - 28 October 2009

Mr. Paul Landvogt, Equens Payment factories to optimize the processing flow & manage liquidity risk An end-to-end payments processing service challenge

Leading the way to the future • From 3.4 to 5 billion card transactions • From 9.4 to 13 billion payment transactions • Retain current clients (BE, DE, FI, FR, GR, IT, LUX, NL, SE, UK) and attract new clients • Maintain top position in Europe (DE, FI, IT, NL) • Expand presence in Europe through partnerships, mergers and acquisitions Strategy • Card processing: merchant acquiring, acquiring processing and issuing services • Domestic and cross-border payment processing services • From generic Clearing & Settlement to tailor made Bank Payment Processing services • Innovative solutions: eInvoicing, mobile payments, healthcare information, biometric • Supporting services: connectivity, risk, management information, customer services Portfolio • Europe’s first truly pan-European cards & payments processor (EACHA, IPFA) • Lowest possible processing and routing costs • Highest standards of quality, reliability and security • Distinctive range of modular, innovative and future-proof processing services • One-stop-shopping for customisable packages and practical advice Core value SWIFT for PMIs - 28 October 2009

Payments servicing banks Payments servicing banks From core payments processing towards extended bank-to-bank supporting services • Cost efficiency • Reliability • Security • Availability • Scalability • Bulk transfer • Any instrument/ scheme • Standard • Reach • Regulations • Community rules Correspondent banking Bilateral Clearing RTGS (High value payment) ACHs Core Back-office processing Clearing & Settlement Back-office processing Extended Cash and liquidity risk management, treasury reconciliation Payment exceptions and investigation

Payments servicing banks Supporting banks in servicing their customers Consumers • Near-real time execution • m- & e- channels • Information on fees • Payment tracking • Common interface to ERP • Real-time access • Standards • Payment E&I • Cash optimisation • Liquidity risk management Financial institutions Corporates Core Payment services Extended Cash and liquidity risk management, treasury reconciliation Payment exceptions and investigation

End-to-end payments factories (“cockpits”) to optimise processing & manage liquidity risk • Basic payments processing services for communities • Extended centralised data flow management • Addressing all market players requirements • Automation to optimise processing end-to-end • On-line exposure visibility to reduce liquidity risk • Standard connectivity, formats and business flows • Cooperation with key global partners • EACHA, IPFA • SWIFT (global service partner) Core Payment capture Back-office processing Clearing & Settlement Back-office processing Payment delivery Extended Cash and liquidity risk management, treasury reconciliation Payment exceptions and investigation

Conclusion and key points • Extension of service portfolio from core payments processing to a payments factory and a centralized control center covering the complete value chain with all the different aspects and requirements • This needs partners join hands while concentrating on their core competence under the condition of a collaborative and cooperative approach • SWIFT is one important partner both in the way of offering product & services (communication, …) and the area of defining standards based on best market practice SWIFT for PMIs - 28 October 2009

Bank of England and SWIFT for High-Value Payment Systems Mr. Ed Kelsey, Bank of England 27 October 2010 14:00 – 14:45

History • RTGS was launched in 1996 as a platform to effect real-time payments in central bank money • Driven by the goal to remove risk from the settlement process • Inter-bank payments are made through the CHAPS payments scheme, operated by CHAPSCo. • The communications network was upgrade to SWIFT in 2001 • DvP link to Crest introduced in 2001 SWIFT for PMIs - 28 October 2009

What We Do • RTGS settled, on average, £744bn per day, and £908bn on its busiest day last year • Through RTGS, the Bank of England provides payment facilities to: • CHAPS Sterling payment system • CREST settlement system • Lower value net clearings: • BACS • Cheque and Credit • The Faster Payments Service • LINK • RTGS also plays a key role in the implementation of monetary policy, with the voluntary remunerated reserve accounts which sit at the heart of the Bank’s Sterling Monetary Framework held in the RTGS processor SWIFT for PMIs - 28 October 2009

Why SWIFT? • Used to transmit the payment messages via SWIFT FIN Y-Copy made between banks: • Security • Availability • Non-repudiation • Also used for the RTGS Enquiry Link to enable: • Activity on a bank’s account to be monitored • A bank to receive information about their account • And, in certain circumstances, transfer funds between their accounts SWIFT for PMIs - 28 October 2009

Future Developments: Drivers • Liquidity Savings Mechanisms • Financial crisis means more liquidity is required, and that already available will need to be used more efficiently • Management/Business Information • Financial crisis means the banks need to see what liquidity they are using, and when • Enquiry Link Upgrade • Technology is dated and costs are incurred by the banks when implementing a “fat GUI” in their premises • Market Infrastructure Resiliency Service (MIRS) • Enhancing the resiliency of RTGS, to bring it into line with best international practice SWIFT for PMIs - 28 October 2009

Future Developments: The Bank’s response • Liquidity Savings Mechanisms • We are looking to implement changes to the settlement algorithms within RTGS, to be introduced in 2011/12 • Management/Business Information • We upgraded to SWIFT FIN full Y-Copy in September 2010 and will implement a payments database for members in 2011/12 • Enquiry Link Upgrade • We are exploring using SWIFT browse with full SWIFT Interact messages • Market Infrastructure Resiliency Service (MIRS) • We are working with SWIFT and other central banks to build a “generic” RTGS system which could act as our 3rd site SWIFT for PMIs - 28 October 2009

SWIFT supports Payment Market Infrastructure to address future challenges SWIFT for PMIs - 28 October 2009

Benefits for Payments Market Infrastructures A comprehensive messaging solution • Guaranteed payment execution • Traffic and duty segregation • 99,999% operational uptime/ disaster recovery • 24/7 dedicated support for critical infrastructures • Monitor and control liquidity positions • Reliable and efficient exceptions management • 8000+ banks in +200 countries • Access indirect participants through Service Bureaus • Best industry practices • Business model and physical representation (XML) • Tools / partners for message conversion and application integration • Reference data for payments routing • Messaging price adapted to market conditions • Single messaging platform for all financial businesses • Support bilateral models with no need of investment for a ACH • Cope with legacy and innovations • Support any industry standard • Payments and reporting SWIFT for PMIs - 28 October 2009

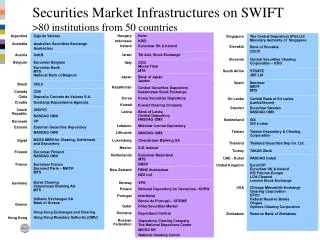

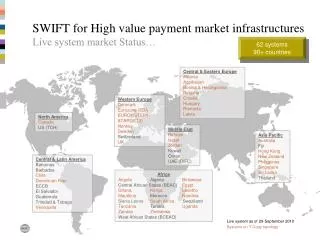

Thank YOU Q&A Payment Market InfrastructuresLive system status as of September 2010 Western Europe Denmark Norway Sweden Switzerland UK Eurozone Target 2 EBA Clearing Austria Germany Greece Ireland Italy Netherland Spain Central & Eastern Europe Albania Azerbaijan Bosnia & Herzegovina Bulgaria Croatia Hungary Slovenia Romania Poland 62 high-value MIs 240+ million payments/year 21 low-value MIs 5+ billion payments/year 2000+ banks 90+ countries North America Canada US (TCH) Middle East Bahrain Israel Jordan Kuwait UAE (DIFC) Qatar Asia Pacific Australia Fiji Hong Kong New Zealand Philippines Singapore Sri Lanka Thailand Central & Latin America Bahamas Barbados Chile Dominican Rep. Guatemala Trinidad & Tobago Venezuela Africa Angola Algeria Botswana Central African States (BEAC) Egypt Ghana Kenya Lesotho Mauritius Morocco Namibia South Africa Swaziland Tanzania Tunisia Uganda Zambia Zimbabwe West African States (BCEAO) Legend Both HVP and LVP MI LVP MI only HVP MI only

Payment Market InfrastructuresSWIFT Contacts High-Value Payment Market Infrastructures Low-Value Payment Market Infrastructures • Stephane Ernst • Market Manager • Mobile : +32-476-896087 • stephane.ernst@swift.com • Marie-Christine Diaz • Market Manager • Mobile : + 32 474 99 10 65 • marie-christine.diaz@swift.com SWIFT for PMIs - 28 October 2009