Download

1 / 19

190 likes | 372 Vues

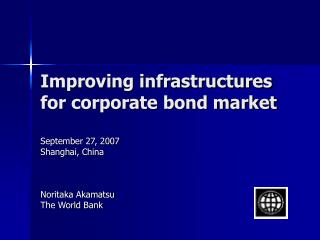

Improving infrastructures for corporate bond market. September 27, 2007 Shanghai, China Noritaka Akamatsu The World Bank. Issues. Benchmark yield curve (GS market externality) Credit rating Legal framework Trading market and transparency (GS market externality)

E N D

Improving infrastructures for corporate bond market September 27, 2007 Shanghai, China Noritaka Akamatsu The World Bank

Issues • Benchmark yield curve (GS market externality) • Credit rating • Legal framework • Trading market and transparency (GS market externality) • Clearance, custody and settlement (GS market externality)

Benchmark yield curve • The development of the government bond market has created benchmarks in many markets in the region. • In a varying degree across the countries in the region, an yield curve is being established, facilitating corporations to tap the market. E.g., • China, Thailand, Indonesia have established benchmarks and yield curves. Vietnam has issued an MOF decision to issue benchmark bonds. • In many markets, however, the reliability of the benchmarks / yield curves needs to be improved further by enhancing the transparency, liquidity and efficiency of the government bond market. E.g., • Repo market, • Primary dealers / market makers • Trading platform and market / price transparency,

Credit rating • The region’s rating agencies are only serving their home country market. Does the region really need its own credit rating agencies capable of serving across the region? • Mandating credit rating for a wide variety of issues / issuers (e.g., private placements, local government bonds, etc.) may make it a commercially viable business. However, it may also discourage the market development by imposing cost. • Credit rating agencies could be required to have certain qualifications to ensure their independence / credibility. E.g., • Certain ownership / governance structure to promote reputation and independence. • Diversified revenue base not to rely only on bond rating, particularly, revenues linked to services for investors. • Qualified financial analysts and fit-and-proper management. • Minimum capital. • Etc.

Legal framework • In a varying degree, countries in the region have established / improved a basic legal and regulatory framework for corporate bond issuance. E.g., • China: Securities law and CSRC Decree 49 on corporate bond issuance (i.e., a move toward an integration of the exchange market and the Inter-Bank Market.). • Vietnam: Securities Law, MOF Decree 52 on enterprise bonds • Yet, significant inadequacies remain regarding: • Securitization, • Special Purpose Vehicle (SBV), • Trust • Etc.

Settlement system • In a varying degree, settlement systems have also been improved. E.g., • Thailand: Bathnet II • Indonesia: BI-SSSS linked to BI-RTGS • Vietnam: SBV IBPS for RTGS money settlement. The securities custody and delivery system has yet to be integrated and strengthened. • Issues remaining are: • Consolidation of the securities custody arrangements. • Establishment of online links with the trading / market information systems for straight through processing (STP). • Does the region need its own international central securities depository (ICSD) like Euroclear in Europe?

Bond trading market • Bond market is dominated by large institutional investors and dealers, and block trades are common. The large institutional seller and the buyer need to negotiate the trade directly or indirectly through a broker. • Transaction conventions have been being standardized. • Quoting convention, yield calculation method, trading units, trade agreement format, settlement cycles, settlement instruction format, master repurchase agreement, etc. • Although advanced ICT is increasingly making it possible to better organize the government bond market, corporate bond market, which is fragmented by nature, remains difficult to organize into a common trading platform. • A vast majority of the trading has been taking place in the over-the-counter (OTC) market around the world. OTC market transactions are difficult to capture, and therefore, the market lacks transparency.

A Typical Secondary Bond Market Transaction Dealer E An investor contacts a dealer to unwind some of their large positions. Dealer C Inter-Dealer Broker Dealer B Buy-side Investor 1 Dealer D Inter-Dealer Broker Buy-side Investor 2 Dealer A Instead of risking its own capital, Dealer D contacts inter-dealer brokers to unload the investor’s sell order. An investor interested in buying bonds contacts a few dealers to get price quotes for execution. Dealer F Source: Celent Communications, World Bank

Policy objectives formarket transparency • The issuer wants good market transparency for all potential market participants because: • it makes the dealer market competitive and reduces bid-ask spread, thus attracts broadest participation of investors in the market; and • resulting demand facilitates placement in the primary market, lowers the yield and, therefore, reduces the financing cost to the issuer. • The regulator is concerned about transparency because: • Transparent market facilitates best execution of orders for investors by bond dealers and brokers (fairness of the market). • Reliable benchmark yield facilitates setting of coupons in the primary market, pricing of instruments in the secondary market and valuation of bond portfolios and collaterals and, therefore, risk management.

Trading platform and market information • Trading platform can help enhance the transparency, but fragmented / illiquid corporate bond market alone cannot support its commercial viability. • A trading platform for government bonds, if adopted, could be used to trade corporate bonds as well, but market participants may prefer to trade through a broker in the OTC market. • Market participants should be required to timely report transactions. There should be arrangements to centrally gather the reported information, consolidate it as market information and disseminate back to the market in a timely manner. This require a sound market information system.

Architectural Models Many possibilities exist (see www.bondmarkets.com). • Single dealer systems • Inter-dealer systems • eSpeed (Canter Fitzgerald), ETC (Garban Intercapital), MTS (which acquired BrokerTec and Coredeal), etc. • Multi-dealer systems • Market Access, TradeWebb, Bloomberg BondTrader, etc. • Cross matching systems • Automated Bond System (NYSE, i.e., order-matching system) • Auction systems • BondVision (for MTS to create a multi-dealer system)

A typical market structure Individual Cooperative Mutual Fund Individual Mutual Fund SC Bank Bank Dealer SC Provident Fund Dealer Dealer Inter-dealer Market Insurance Company Bank Dealer Foundation Dealer SC Dealer Bank Pension Fund Pension Fund SC Individual Mutual Fund Insurance Company

Competitive Inter-Dealer Market Cooperative Mutual Fund Individual Mutual Fund Dealer Dealer Dealer IDB Pension Fund IDB Insurance company SRO & Information Platform Dealer Dealer Foundation IDB IDB Pension Fund Dealer Dealer Dealer Provident Fund Individual Mutual fund Insurance company

Straight through processing from reporting to settlement • Settlement system-based information does not include price information. Even if the system is designed to capture it, it would involve time delay or noise unless the settlement cycle is standardized and made short. However, short, standardized settlement cycle would create a liquidity pressure on market participants and may be resisted by them. • Instead, the reporting could be made a separate but linked requirement for all transactions to be settled. • To facilitate the compliance, the reporting should be supported by a common information network linked online to the settlement system, achieving STP (although the settlement system should offer an option for market participants to access directly in case of system failure of the reporting system.)

However, bear in mind that … • Transparency is not free. • Gathering, processing and disseminating useful information involves implicit as well as explicit costs while bond trading is very sensitive to the transaction cost. • User fee may be charged to cover the cost while the use is made mandatory (Is this fair?). The authority and the market participants should explore ways to reduce the cost (e.g., internet-based system) and enhance the convenience of reporting (e.g., STP) as much as possible. • The more transparent, not always the better. • Demanding high transparency of certain market information can discourage market activities, particularly market making. • Examine and identify what kind of transparency is desirable and what not.

Transparency andmarket architecture • Transparency is not one thing: Certain information is a public good while some other is a private good owned by those who pay for or invest in it, implicitly or explicitly. • Pre-trade price and volume information is a partly private good while post-trade price and volume information should be a mostly public good. • Anonymity: identity of market participants, pre- and post-trade is a private good. • Balancing the public and the private goods is a key to designing the secondary market structure. • Public goods: the more, the better, • Private goods: need to reconcile conflicting business interests of different groups of market participants.

Optimal market architecture • Reconciling different business interests of different groups of market participants. • Market makers / primary dealers • Non-market maker intermediaries • Institutional investors • Retail investors • Primary market structure influences the optimal secondary market structure. • Primary dealer (PD) system with an “exclusive” privilege to participate in the primary auctions.

Legal & regulatory issues • Should an ID platform be authorized as an exchange? • Can it be allowed to offer voice broking without a brokerage license? • Should it be supervised as an exchange as well as an SRO by the securities regulator? • How should IDB be authorized and regulated? • Is there Regulation ATS to authorize and regulate electronic trading platforms and ECNs? • Whether and how should Bloomberg, Reuters, Telerate be regulated if they offer trading services? • How can possible public sector ownership be treated under the existing regulatory framework?