Bertrand and Hotelling

Bertrand and Hotelling. Oligopoly. Assume: Many Buyers Few Sellers Each firm faces downward-sloping demand because each is a large producer compared to the total market size There is no one dominant model of oligopoly… we will review several.

Bertrand and Hotelling

E N D

Presentation Transcript

Oligopoly • Assume: Many Buyers • Few Sellers • Each firm faces downward-sloping demand because each is a large producer compared to the total market size • There is no one dominant model of oligopoly… we will review several.

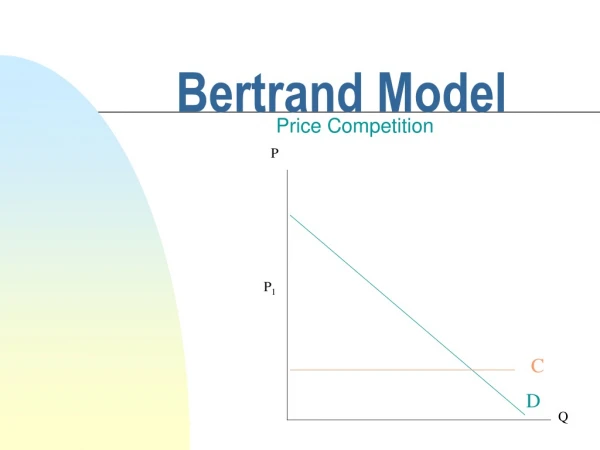

1.Bertrand Oligopoly (Homogeneous) • Assume: Firms set price* • Homogeneous product • Simultaneous • Noncooperative • *Definition: In a Bertrand oligopoly, each firm sets its price, taking as given the price(s) set by other firm(s), so as to maximize profits.

Definition: Firms act simultaneously if each firm makes its strategic decision at the same time, without prior observation of the other firm's decision. Definition: Firms act noncooperatively if they set strategy independently, without colluding with the other firm in any way

How will each firm set price? • Homogeneity implies that consumers will buy from the low-price seller. • Further, each firm realizes that the demand that it faces depends both on its own price and on the price set by other firms • Specifically, any firm charging a higher price than its rivals will sell no output. • Any firm charging a lower price than its rivals will obtain the entire market demand.

Definition: The relationship between the price charged by firm i and the demand firm i faces is firm i's residual demand • In other words, the residual demand of firm i is the market demand minus the amount of demand fulfilled by other firms in the market: Q1 = Q - Q2

Price Example: Residual Demand Curve, Price Setting Market Demand Residual Demand Curve (thickened line segments) • Quantity 0

Assume firm always meets its residual demand (no capacity constraints) • Assume that marginal cost is constant at c per unit. • Hence, any price at least equal to c ensures non-negative profits.

Example: Reaction Functions, Price Setting and Homogeneous Products 45° line Price charged by firm 2 Reaction function of firm 1 Reaction function of firm 2 • p2* Price charged by firm 1 p1* 0

Thus, each firm's profit maximizing response to the other firm's price is to undercut (as long as P > MC) • Definition: The firm's profit maximizing action as a function of the action by the rival firm is the firm's best response (or reaction) function • Example: • 2 firms • Bertrand competitors • Firm 1's best response function is P1=P2- e • Firm 2's best response function is P2=P1- e

So… • 1. Firms price at marginal cost • 2. Firms make zero profits • 3. The number of firms is irrelevant to the price level as long as more than one firm is present: two firms is enough to replicate the perfectly competitive outcome!

Equilibrium: • If we assume no capacity constraints and that all firms have the same constant average and marginal cost of c then… • For each firm's response to be a best response to the other's each firm must undercut the other as long as P> MC • Where does this stop? P = MC (!)

Bertrand Competition • Homogenous good market / perfect substitutes • Demand q=15-p • Constant marginal cost MC=c=3 • It always pays to undercut • Only equilibrium where price equals marginal costs • Equilibrium good for consumers • Collusion must be ruled out

Sample result: Bertrand Two Firms Fixed Partners Five Firms Random Partners Two Firms Random Partners “I learnt that collusion can take place in a competitive market even without any actual meeting taking place between the two parties.” “Some people are undercutting bastards!!! Seriously though, it was interesting to see how the theory is shown in practise.”

Hotelling’s (1929) linear city • Why do all vendors locate in the same spot? • For instance, on High Street many shoe shops right next to each other. Why do political parties (at least in the US) seem to have the same agenda? • This can be explained by firms trying to get the most customers.

Hotelling (voting version) Voters vote for the closest party. R L Party A Party B If Party A shifts to the right then it gains voters. R L Party A Party B Each has incentive to locate in the middle.

Hotelling Model R L Party A Party B Average distance for voter is ¼ total. This isn’t “efficient”! R L Party A Party B Most “efficient” has average distance of 1/8 total.

Further considerations: Hotelling • Firms choose location and then prices. • Consumers care about both distance and price. • If firms choose close together, they will eliminate profits as in Bertrand competition. • If firms choose further apart, they will be able to make some profit. • Thus, they choose further apart.

Price competition with differentiated goods • Prices pA and pB • Zero marginal costs • Transport cost t • V value to consumer • Consumers on interval [0,1] • Firms A and B at positions 0 and 1 • Consumer indifferent if V-tx- pA= V-t(1-x)- pB • Residual demand qA=(pB- pA+t)/2t for firm A • Residual demand qB=(pA- pB+t)/2t for firm B

Price competition with differentiated goods • Residual demand qA=(pB- pA+t)/2t for firm A • Residual demand qB=(pA- pB+t)/2t for firm B • Residual inverse demands pA=-2t qA +pB+t, pB=-2t qB +pA+t • Marginal revenues must equal MC=0 MRA=-4t qA +pB+t=0, MRB=-4t qB +pA+t=0 MRA=-2(pB- pA+t)+pB+t=0, MRB=-2(pA- pB+t)+pA+t=0 MRA=2pA-pB-t=0, MRB=2pB-pA-t=0 pA=2pB-t; 4pB-2t-pB-t=0; pB=pA=t • Profits t/2

Bertrand Competition (Differentiated) • Assume: Firms set price* • Differentiated product • Simultaneous • Noncooperative • As before, differentiation means that lowering price below your rivals' will not result in capturing the entire market, nor will raising price mean losing the entire market so that residual demand decreases smoothly

Example: • Q1 = 100 - 2P1 + P2"Coke's demand" • Q2 = 100 - 2P2 + P1"Pepsi's demand" • MC1 = MC2 = 5 • What is firm 1's residual demand when • Firm 2's price is $10? $0? • Q110 = 100 - 2P1 + 10 = 110 - 2P1 • Q10 = 100 - 2P1 + 0 = 100 - 2P1

Example: Residual Demand, Price Setting, Differentiated Products • Each firm maximizes profits based on its residual demand by setting MR (based on residual demand) = MC Coke’s price Pepsi’s price = $0 for D0 and $10 for D10 100 MR0 0 Coke’s quantity

Example: Residual Demand, Price Setting, Differentiated Products • Each firm maximizes profits based on its residual demand by setting MR (based on residual demand) = MC Coke’s price 110 Pepsi’s price = $0 for D0 and $10 for D10 100 D10 D0 0 Coke’s quantity

Example: Residual Demand, Price Setting, Differentiated Products • Each firm maximizes profits based on its residual demand by setting MR (based on residual demand) = MC Pepsi’s price = $0 for D0 and $10 for D10 Coke’s price 110 100 D10 D0 MR10 MR0 0 Coke’s quantity

Example: Residual Demand, Price Setting, Differentiated Products • Each firm maximizes profits based on its residual demand by setting MR (based on residual demand) = MC Pepsi’s price = $0 for D0 and $10 for D10 Coke’s price 110 100 D10 D0 MR10 5 MR0 0 Coke’s quantity

Example: Residual Demand, Price Setting, Differentiated Products • Each firm maximizes profits based on its residual demand by setting MR (based on residual demand) = MC Pepsi’s price = $0 for D0 and $10 for D10 Coke’s price 110 100 30 27.5 D10 D0 MR10 5 MR0 0 Coke’s quantity 45 50

Example: • MR110 = 55 - Q110 = 5 • Q110 = 50 • P110 = 30 • Therefore, firm 1's best response to a • price of $10 by firm 2 is a price of $30

Example: Solving for firm 1's reaction function for any arbitrary price by firm 2 • P1 = 50 - Q1/2 + P2/2 • MR = 50 - Q1 + P2/2 • MR = MC => Q1 = 45 + P2/2

And, using the demand curve, we have: • P1 = 50 + P2/2 - 45/2 - P2/4 …or… • P1 = 27.5 + P2/4…reaction function

Pepsi’s price (P2) P2 = 27.5 + P1/4 (Pepsi’s R.F.) • Example: Equilibrium and Reaction Functions, Price Setting and Differentiated Products 27.5 Coke’s price (P1)

P1 = 27.5 + P2/4 (Coke’s R.F.) Pepsi’s price (P2) P2 = 27.5 + P1/4 (Pepsi’s R.F.) • • Example: Equilibrium and Reaction Functions, Price Setting and Differentiated Products 27.5 Coke’s price (P1) 27.5 P1 = 110/3

P1 = 27.5 + P2/4 (Coke’s R.F.) Pepsi’s price (P2) P2 = 27.5 + P1/4 (Pepsi’s R.F.) Bertrand Equilibrium P2 = 110/3 • • Example: Equilibrium and Reaction Functions, Price Setting and Differentiated Products 27.5 Coke’s price (P1) 27.5 P1 = 110/3

Equilibrium: • Equilibrium occurs when all firms simultaneously choose their best response to each others' actions. • Graphically, this amounts to the point where the best response functions cross...

Example: Firm 1 and firm 2, continued • P1 = 27.5 + P2/4 • P2 = 27.5 + P1/4 • Solving these two equations in two unknowns… • P1* = P2* = 110/3 • Plugging these prices into demand, we have: • Q1* = Q2* = 190/3 • 1* = 2* = 2005.55 • = 4011.10

Notice that • 1. profits are positive in equilibrium since both prices are above marginal cost! • Even if we have no capacity constraints, and constant marginal cost, a firm cannot capture all demand by cutting price… • This blunts price-cutting incentives and means that the firms' own behavior does not mimic free entry

Only if I were to let the number of firms approach infinity would price approach marginal cost. • 2. Prices need not be equal in equilibrium if firms not identical (e.g. Marginal costs differ implies that prices differ) • 3. The reaction functions slope upward: "aggression => aggression"

Back to Cournot • Inverse demand P=260-Q1-Q2 • Marginal costs MC=20 • 3 possible predictions • Price=MC, Symmetry Q1=Q2 260-2Q1=20, Q1=120, P=20 • Cournot duopoly: MR1=260-2Q1-Q2=20, Symmetry Q1=Q2 260-3Q1=20, Q1=80, P=100 • Shared monopoly profits: Q=Q1+Q2 MR=260-2Q=20, Q=120, Q1=Q2=60, P=140

Bertrand with Compliments (?!*-) • Q=15-P1-P2, MC1=1.5, MC2=1.5, MC=3 • Monopoly: P=15-Q, MR=15-2Q=3, Q=6, P=P1+P2=9, Profit (9-3)*6=36 • Bertrand: P1=15-Q-P2, MR1=15-2Q-P2=1.5 15-2(15-P1-P2)-P2=-15+2P1+P2=1.5 Symmetry P1=P2; 3P1=16.5, P1=5.5, Q=4<9 P1+P2=11>9, both make profit (11-3)*4=32<36 Competition makes both firms and consumers worse off!

The Capacity Game GM DNE Expand 18 DNE 20 18 15 Ford 16 * 15 Expand 20 16 What is the equilibrium here? Where would the companies like to be?

War Mars Not Shoot Shoot -5 Not Shoot -1 -5 -15 Venus -10 * -15 Shoot -1 -10