Download

1 / 24

240 likes | 255 Vues

Explore how historic tax credits can turn into capital through syndication at the National Historic Tax Credit Conference in Chicago. Gain insights on rehabilitation projects, review bodies, certification processes, pitfalls, and developer considerations. Learn from experts like John M. Tess from Heritage Consulting Group.

E N D

National Historic Tax Credit ConferenceChicago September 24-26, 2008 “How Credits Become Capital: When and How to Syndicate” John M. Tess Heritage Consulting Group Portland, OR Philadelphia, PA 19118 503-228-0272 jmtess@heritage-consulting.com www.heritage-consulting.com

General Observations Rehabilitation projects: Are generally more complex than non-historic deals Time consuming Receive much more scrutiny than non-historic deals from a design standpoint Without early coordination of team players can lead to additional costs and frustrations

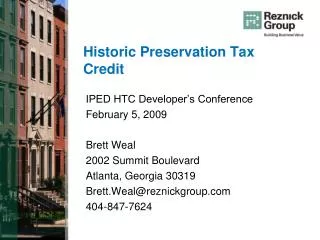

General Post Office or Tariff Building Washington, DC National Historic Landmark GSA property Long Term lease to the Kimpton Hotel Group 180 Room hotel Rehab costs approximately $28 Million

Tariff Building Washington, DC

Tariff Building Washington, DC

Tariff Building Washington, DC

Review Bodies 2 local agencies in the District of Columbia Neighborhood Groups, Goodwill and support SHPO, Tax Act NPS, Tax Act GSA, Owners Advisory Council, Section 106

Who are some of the development team players Developer Contractor Attorney(s) Accountants Architects and engineers Other Consultants Preservation Consultant

Other possible team players • Local review bodies • Neighborhood • SHPO • NPS

Understanding how the Standards are interpreted The interpretation of the Standards is a subjective process. Local, State and Federal authorities may differ on the interpretation. Interpretation is generally done on a case by case basis depending on many factors. Interpretation can vary from one reviewer to the next.

Tax Act Certification Process 3 Step process Part One - Determines whether your building is historic or might be considered historic. Part Two Application - Sets forth your proposed rehab project for purposes of review by state and federal agencies to determine if your project meets the Secretary of the Interior’s Standards. (Part Three) Certification of Completed work.

National Register Process and when to Nominate • Want to determine if the building is eligible • Want to determine if you want to leave the 10% option open

Part OnePitfalls Timing of filing – Prior to being placed in service and prior to review of Part Two. Listing in the National Register Assuming that the Building will become historic.

Part Two Pitfalls Proper documentation Timing of submittal Being clear on the scope of Tax Act review Assumption that local or state approval in turn means National Park Service approval Early review by National Park Service Failing to submit additional information following preliminary approval

Certification of Completed Work Pitfalls • Forgetting to file • Filing too soon – May limit you ability to use the credit • Problems with complexes – future work on other phases may affect the credits already claimed

Helping to put the team together • Saving time and money in the design process • Providing letters to lenders and equity investors

The following are questions every developer should answer prior to beginning the Tax Certification process? • Does the Building Qualify? • Should I use the 10% or 20 % Credit? • Can I even use the credit? • What constitutes a Qualified Rehabilitation Expenditure? • When do the credits become available? • Who can use the credit? • To sell or not to sell the credits? • What other incentives might be available?

John M. Tess Heritage Consulting Group 1120 NW Northrup St. Portland, OR 97209 15 Highland Avenue Philadelphia, PA 19118 jmtess@heritage-consulting.com www.heritage-consulting.com