Download

1 / 1

20 likes | 172 Vues

Franchisor Accounting: A Focus on Consolidation and Revenue Recognition Standards Julie Wynstra Marietta College. INTRODUCTION. ANALYSIS AND SUMMARY. CONSOLIDATION STANDARDS .

E N D

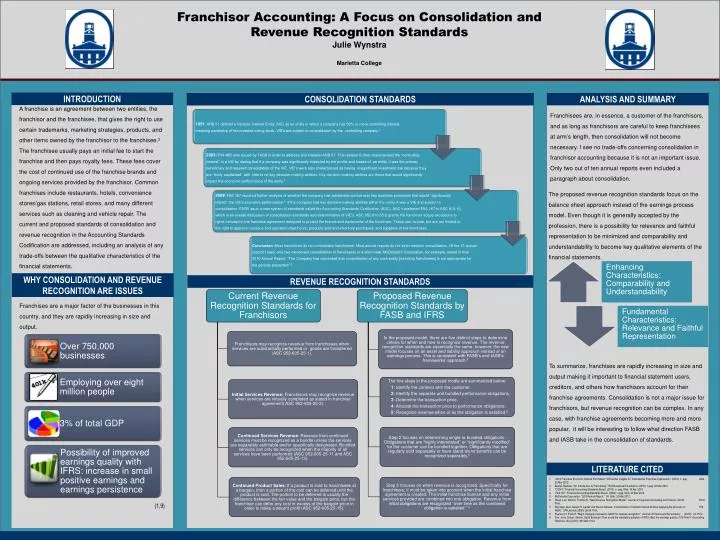

Franchisor Accounting: A Focus on Consolidation and Revenue Recognition StandardsJulie Wynstra Marietta College INTRODUCTION ANALYSIS AND SUMMARY CONSOLIDATION STANDARDS A franchise is an agreement between two entities, the franchisor and the franchisee, that gives the right to use certain trademarks, marketing strategies, products, and other items owned by the franchisor to the franchisee.2 The franchisee usually pays an initial fee to start the franchise and then pays royalty fees. These fees cover the cost of continued use of the franchise brands and ongoing services provided by the franchisor. Common franchises include restaurants, hotels, convenience stores/gas stations, retail stores, and many different services such as cleaning and vehicle repair. The current and proposed standards of consolidation and revenue recognition in the Accounting Standards Codification are addressed, including an analysis of any trade-offs between the qualitative characteristics of the financial statements. Franchisees are, in essence, a customer of the franchisors, and as long as franchisors are careful to keep franchisees at arm’s length, then consolidation will not become necessary. I see no trade-offs concerning consolidation in franchisor accounting because it is not an important issue. Only two out of ten annual reports even included a paragraph about consolidation. The proposed revenue recognition standards focus on the balance sheet approach instead of the earnings process model. Even though it is generally accepted by the profession, there is a possibility for relevance and faithful representation to be minimized and comparability and understandability to become key qualitative elements of the financial statements. WHY CONSOLIDATION AND REVENUE RECOGNITION ARE ISSUES REVENUE RECOGNITION STANDARDS Franchises are a major factor of the businesses in this country, and they are rapidly increasing in size and output. To summarize, franchises are rapidly increasing in size and output making it important to financial statement users, creditors, and others how franchisors account for their franchise agreements. Consolidation is not a major issue for franchisors, but revenue recognition can be complex. In any case, with franchise agreements becoming more and more popular, it will be interesting to follow what direction FASB and IASB take in the consolidation of standards. LITERATURE CITED “2012 Franchise Economic Outlook Fact Sheet.” IHS Global Insights for: International Franchise Organization. (2012): n. pag. Web. 20 Mar 2012. Beshel, Barbara. “An Introduction to Franchising.” IFA Educational Foundation. (2010): n.pag. 20 Mar 2012. “CON 8.” Financial Accounting Standards Board. (2010): n. pag. Web. 10 Apr. 2012. “FAS 167.” Financial Accounting Standards Board. (2009): n.pag. Web. 22 Mar 2012. McDonalds Corporation. “2010 Annual Report.” 30. Web. 20 Mar 2012. Olsen, Lori, Weirich, Thomas R. “New Revenue Recognition Model.” Journal of Corporate Accounting and Finance. (2010): 55-61. Print. Reinstein, Alan, Gerald H. Lander and Steven Danese. “Consolidation of Variable Interest Entities: Applying the provision of FIN 46(R).” CPA Journal (2006): 28-34. Print. Ryerson III, Frank E. “Major changes proposed to GAAP for revenue recognition.” Journal of Finance and Accountancy. (2010): 1-9. Print. Sun, Jerry, Cahan, Steven, David Emanuel. “How would the mandatory adoption of IFRS affect the earnings quality of US firms?” Accounting Horizions. 25.4 (2011): 837-860. Print. (1,9)