Download

1 / 10

120 likes | 298 Vues

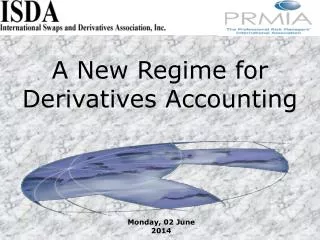

A New Regime for Derivatives Accounting. The IASB Structure. Board of Trustees Appoints IASB, IFRIC, SAC Oversees effectiveness and funding. Standards Advisory Council. International Accounting Standards Board (IASB) Develops IFRSs. International Financial Reporting

E N D

The IASB Structure Board of Trustees Appoints IASB, IFRIC, SAC Oversees effectiveness and funding StandardsAdvisory Council International Accounting Standards Board (IASB) Develops IFRSs International Financial Reporting InterpretationsCommittee (IFRIC) Develops Authoritative Interpretations of IFRS

EFRAG SupervisoryBoard EFRAG Technical Expert Group Insurancesub-committee The EU Endorsement Mechanism Political level Technical level AccountingRegulatory Committee (ARC) European Commission Advises Brings Recommendations to

Accounting in 2005 • Existing standards on Financial Instruments - IAS 32 and IAS 39 • June 2002 - Proposed Amendments • November 2002 – over 160 comment letters received • March 2003 – “public roundtables” held • August 2003 - Proposed Amendments: Fair Value Hedge Accounting for a Portfolio Hedge of Interest Rate Risk

The impact on the Reporting Environment • Over 7,000 European firms affected from 2005. • Each country can expand scope of EU regulation. • Companies not under the EU Regulation will continue to be subject to Accounting Directives and local accounting standards • Even where convergence is an objective, there are still likely to be differences for a while • These differences, together with the related impacts on tax and regulatory reporting, could have a significant influence on those many companies that have a choice to make

Fair Value Measurement • any financial instrument can be measured at fair value • ‘what is fair value?’ • The Exposure Draft presented a number of potential issues • From our work with the IASB, we are hopeful that many of these issues have been resolved • Final wording?

Hedge Accounting • All derivatives on balance sheet at fair value. • Doing nothing will create significant earnings volatility. • Achieving hedge accounting is a challenge: • Strict requirements for hedge designation. • Process issues are significant. • Resource requirements are large. • Ability to achieve portfolio hedge accounting is limited, and still moving. • Expect some earnings volatility even so. • Economic hedges and hedge accounting are likely to differ.

Issuer Classification Liability, Equity, or Both? • Split accounting for compound instruments • Liability component is initially measured at fair value with any residual amount assigned to equity • A derivative based on an entity’s own equity instruments, depending on its terms for settlement, may be accounted for as: • a derivative asset/liability (net amount) • a liability for the gross redemption amount • equity

Derecognition • The model is new and still moving. • Still not sure what it means other than change. • It will impact all securitisation transactions executed from 1 January 2004 • …but we won’t see the final model until the year end.

Questions and Answers?