Download

1 / 10

100 likes | 121 Vues

This article discusses the challenges and opportunities in improving the provision of debt advice, focusing on the work of Citizens Advice and the key elements of their Money Advice Strategy. It highlights the increasing demand for debt advice, funding challenges, and the need for consistent and high-quality services. The article also emphasizes the importance of empowering citizens, integrating preventative and responsive services, and utilizing volunteers to enhance the capacity of debt advice provision.

E N D

Improving Debt Advice provision. Lisa Colclough National Money Advice Policy and Development Officer Citizens Advice

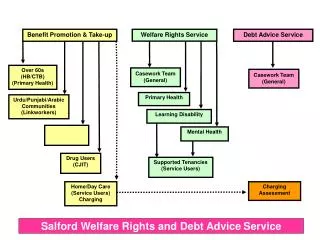

The CAB Service • Citizens Advice Bureaux - independent charities • 390 member bureaux • 16000 volunteers • 95% public awareness • 52% public usage/contact • 7 million new problems last year – 18% increase due to recession • Advice face-to-face, on the phone, in community venues, by email and www.adviceguide.org.uk - 9 million users • Advice available from nearly 3,400 locations – one-third of these in health settings

All topics handled • 100% of bureaux give advice on debt – level of service to deliver casework varies with funding • 66% of bureaux deliver financial education • 14 Financial Capability forums • Money Advice (Money Guidance) delivered in Wales and Scotland

2.3m debt issues/problems (1/3 of all problems) • 580,000 people advised on debt problems • 250,000 receive financial education • 70% are tenants not homeowners • Half the average income • Owe £17k on average – unsecured • No savings – even for a rainy day • High levels fuel poverty

Lots of innovative and exiting projects but • Demand increasing • Funding challenges • F2F (FIF) funding extended until April 2012 • Local Authority funding cuts • LSC funding for debt advice likely to end • We welcome MAS involvement and co-ordinated approach to delivery and funding • Our Money Advice Strategy is developing to meet challenges and opportunities

Key elements Empowering citizens • Helping people to help themselves • Self-help is part of every service • Creating a ‘contract’ with the client • Joining up preventative and responsive services • Modelling how these mesh together • Integrating into the ‘money advice’ model • Following up clients to avoid the revolving door

Consistency and Quality Creating greater quality and consistency • Establishing a single recommended process model • Across and between all channels • Working with partners to deliver • Integrating existing tools such as CASHflow and the Money Advice Service Health Check • Further development of ICT tools that both advisor and client can use • Delivered to a recognised standard

In the community Making greater use of volunteers • At different stages of the money advice process • Enhancing the capacity of specialist money volunteers • Consistent support frameworks for volunteers

Benefits for the consumer • Clear – knowing where to go • Tailored – Advice that mixes web, phone and / or face-to-face in a way that is right for the user • Empowering – throughout the process, building skills and confidence to avoid crisis happening again and financial ‘health’ • Local, caring and independent – being served by people in their communities • Effective – solving problems and changing behaviour

Contact • Lisa.colclough@citizensadvice.org.uk 07967 014690