Download

1 / 13

130 likes | 331 Vues

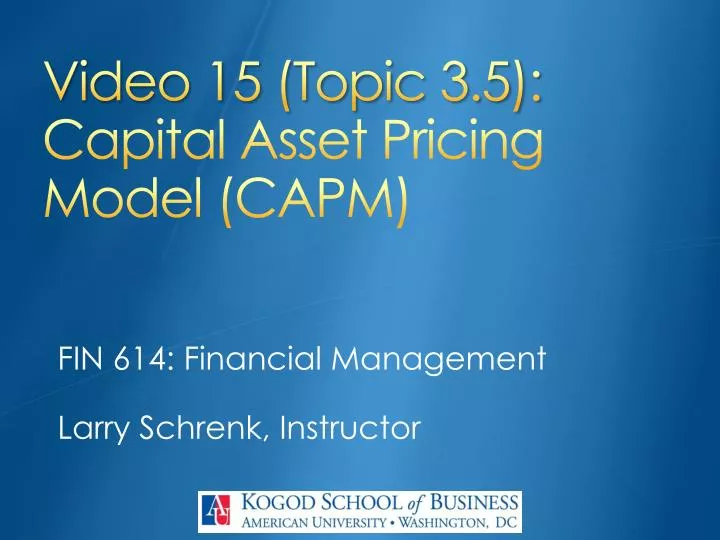

Video 15 (Topic 3.5): Capital Asset Pricing Model (CAPM). FIN 614: Financial Management Larry Schrenk, Instructor. Topics. Capital Market Line (CML) Security Market Line (SML) Capital Asset Pricing Model (CAPM ). Capital Market Line (CML). Market Portfolio. Efficient Frontier. Return.

E N D

Video 15 (Topic 3.5):Capital Asset Pricing Model (CAPM) FIN 614: Financial Management Larry Schrenk, Instructor

Topics • Capital Market Line (CML) • Security Market Line (SML) • Capital Asset Pricing Model (CAPM)

Capital Market Line (CML) Market Portfolio Efficient Frontier Return CML MVP rf sp

Security Market Line • Security Market Line (SML) • Graphing the relationship between beta and return • Begin with the two points we know:

Building the SML▪ We know two points. Where would we find portfolios that contain combinations of the risk free asset and the market? Return Return rM Market rf Risk Free Asset 0 1 Beta

Using the SML▪ SML What would happen if there were a stock above the line? Return Return Market equilibrium forces all stocks to be on the line, which is called the Security Market Line (SML). rM What would happen if there were a stock below the line? rf 0 1 Beta

The CAPM Equation • CAPM Equation • Formula for the SML • Firm Data • Beta • Market Data • The Risk Free Rate • The Return on the Market

Capital Asset Pricing Model (CAPM) • It is the equilibrium model that underlies all modern financial theory. • Derived using principles of diversification with simplified assumptions. • Markowitz, Sharpe, Lintner and Mossin are researchers credited with its development.

Assumptions • Single-period investment horizon. • Investors forecasts agree with respect to expectations, standard deviations, and correlations of the returns of risky securities • Therefore all investors hold risky assets in the same relative proportions • Investors behave optimally • In equilibrium, prices adjust so that aggregate demand for each security is equal to its supply

CAPM Data • Beta • Linear Regression • Firm Stock Return on Market Return (S&P 500) • Risk Free Rate • Treasury Security • Maturity = CAPM Time Horizon • Return on the Market • Average Return on a Market Portfolio (S&P 500)

The CAPM Equation: Examples • Use the following, to find the expected return: • rf = 4.5% • rM = 12.3% • Find the expected return on the following three stocks: •bA= 1.02 •bB= 0.89 •bC= 1.34

Video 15 (Topic 3.5):Capital Asset Pricing Model (CAPM) FIN 614: Financial Management Larry Schrenk, Instructor

![[2018] CAPM Dumps PDF - 100% Pass Guarantee](https://cdn4.slideserve.com/7976872/slide1-dt.jpg)