Download

1 / 9

90 likes | 229 Vues

Yield Curve and Term Structure of Interest Rate. Base rate of interest US Treasuries are “safer” than any other (US) debt security free of credit risk free of liquidity risk On-the-Run Treasuries (most recently auctioned) more so than Off-the-Run Treasuries free of call risk

E N D

Base rate of interest • US Treasuries are “safer” than any other (US) debt security • free of credit risk • free of liquidity risk • On-the-Run Treasuries (most recently auctioned) more so than Off-the-Run Treasuries • free of call risk • but NOT free of interest rate risk • So, their yield is the minimum rate that a (US) investor would accept • This rate is called the base or benchmark rate Other rates trade at a spread (or risk premium) to the benchmark

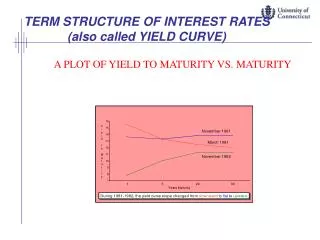

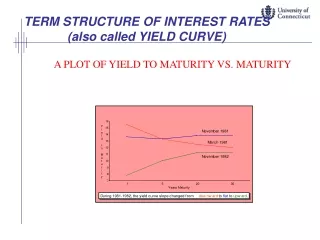

Yield curve • “Plot of yield vs maturity” • Note: Bonds of same maturity with different coupon trade at different yields • Yield curve typically is a par yield curve (same as coupon yield curve). • For Treasuries, use mainly on-the-run issues (whose coupon issues typically trade close to par) • Different shapes of Treasury yield curve • yield increasing with maturity: “upward sloping” or “normal” • Yield decreasing with maturity: “downward sloping” or “inverted” • Hump / U-shaped structure: max/min yield at intermediate maturities

Treasury yield curve useful in setting benchmark for other bonds, but… • Yield curve is not very precise in pricing a premium or discount bond • Yield assumes a single discount rate for all cash flows • If coupons differ, cash flow patterns differ • not appropriate to use same yield to discount different cash flows even with the same maturity

The building blocks of treasury security is zero coupon bonds, or zeros • Also called pure discount bonds • The yield implied by a zero is called spot rate of interest • The price (PV) per dollar of par value for a zero coupon bond is called the discount factor • Other coupon bond, or any risk-free cash flows can be thought as a portfolio of zero coupon bonds • No-arbitrage condition says the price of the portfolio has to be the same as the sum of its component assets

An Example Bond A is a one period zero traded at 3% yield Bond B is a two-period zero traded at 4% yield Bond C is a two-period coupon bond that pays 10% coupon. Bond D is a two-period coupon bond that pays 20% coupon. Q: What is the price of bond C and D? Q: What is the ytm of bond C and D? Q: What coupon rate needed to be offered for a par bond? Q: What should be the ranking of all bonds in terms of yield to maturity?

In practice, intermediate to long term treasury securities are typically issued with coupons. • Strictly speaking, term structure of interest rate and yield curve should be the yields for zeros to avoid ambiguity • We can reverse engineer the zero coupon bond yield with coupon bonds • The process is called bond bootstrapping • Sequential substitution • Q: How do we find one and two year spot rates if we only know the price of bond A and bond C?

Q: How do we find one and two year spot rates if we only know the price of bond A and bond C?

Forward Rates • Embedded in spot rate curve is fact that future spot rates can be “locked in” today. • This does not mean that future spot rates will actually be this “lockable” rate • But this does represent investor expectations • Risk premium • And I can arrange to borrow/lend tomorrow at this rate (which is known today) • This known future spot rate is called the forward rate, fn(t) • E.g., f5(5)= interest rate you can lock in applicable at year 5 for a deposit for 5 periods (matures at period 10) • Q: How is forward rate related to spot rates?