Ch14

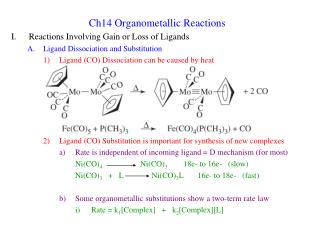

Ch14. 14.1 The nature of autocorrelation ( 自我相關 ) One of ASS of OLS: and are independent => No autocorrelation => correlation doesn’t exist in disturbances If not, => we have autocorrelation (p.429) (a)~(d) 都有線性相關, (e) 則無線性相關, no autocorrelation

Ch14

E N D

Presentation Transcript

Ch14 • 14.1 The nature of autocorrelation (自我相關) One of ASS of OLS: and are independent => • No autocorrelation => correlation doesn’t exist in disturbances If not, => we have autocorrelation (p.429) (a)~(d) 都有線性相關,(e)則無線性相關, no autocorrelation => don’t just rely on your eyeballs !

Ch14 MC 不該用線性估計 *why does autocorrelation occur ? • Inertia: lag, time memory (sluggishness) ex: GDP、生產…=>呈循環(有time memory) 2. 模型設定錯誤(Model Specification Errors)

Ch14 3. The cobweb Phenomenon (蛛網理論) => 農民都去種白菜=> 白菜excess supply => 農民都不種白菜=> 白菜excess demand 4. 資料處理的錯誤(Data Manipulation) • 14.2 Consequences of autocorrelation(p.431) • 與Heteroscedasticity 一樣: still unbiased => , but min Var( ) no longer hold => is not BLUE anymore => F, t, R², R², C.I are not reliable => test hypothesis conclusion invalid

Ch14 Inconclu-sion Inconclu- sion No autocorrelation + auto. - auto. 0 dL du 2 4-du 4-dL 4 • 14.3 detecting autocorrelation (p.434) Graphical Method ☆ The Durbin-Watson statistic => E-view will compute Note: 1. 0<d<4 2. 愈接近2, 愈無自我相關 3. dL, du 可查表得知 (p.528)

Ch14 Ex:14.1 d=0.2136 (E-view) => 落入”+” autocorrelation => check with p.528, n=45, k為number of independent variable =1 得 dL=1.475, du=1.566, 代入上數線判斷區間: there is positive autocorrelation. • Limitations of D-W statistic (p.346) • 需在有截距項時才可使用 • ,只能檢定一階自我相關 • Lagged dependent variable appear among X1…X4

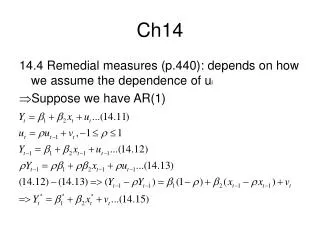

Ch14 14.4 Remedial measures (p.440): depends on how we assume the dependence of ui • Suppose we have AR(1)

Ch14 OLS on (14.15)=> no autocorrelation • will be BLUE • called generalized Least Squares (GLS), 使用一般化最小平方法,求出 值 14.5 How to estimate (1) : the first difference Method (一階差分法) (if D-W statistic <R² ) Assume 代入(14.14)