Designing Effective Deposit Protection for Financial Stability and Systemic Resilience

60 likes | 179 Vues

This document outlines essential principles for financial regulation to enhance stability by addressing moral hazard while allowing institutions to fail. It emphasizes the importance of creating well-designed deposit protection schemes that mitigate bank runs, prevent political pressure to save insolvent banks, and facilitate the swift transfer of critical deposit-taking functions. It also addresses the cross-border implications of deposit protection, stressing the need for international cooperation and comparable coverage across countries to ensure systemic relevance and stability of domestic financial systems.

Designing Effective Deposit Protection for Financial Stability and Systemic Resilience

E N D

Presentation Transcript

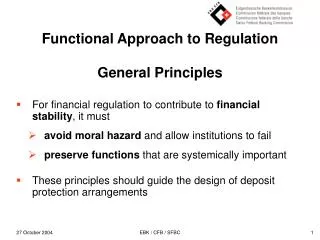

Functional Approach to Regulation General Principles • For financial regulation to contribute to financial stability, it must • avoid moral hazard and allow institutions to fail • preserve functions that are systemically important • These principles should guide the design of deposit protection arrangements EBK / CFB / SFBC

Objectives • Properly designed deposit protection arrangements will • Reduce the risk of bank runs • Reduce the risk of political pressure to save an insolvent bank • Promote the rapid transfer of systemically important deposit taking through replacement or detachment • Reduce the systemic effects of insolvency through exante or ex post measures (e.g., set-off, market structure measures, safety-net) • Acknowledge differences in regulatory design across countries EBK / CFB / SFBC

Cross-border Implications • In order to achieve the objectives is it necessary to protect • Deposits in local and foreign currencies? • Deposits held by residents and non-residents? • Deposit at domestic banks and domestic branches of foreign banks? • Deposits at foreign branches of domestic banks? EBK / CFB / SFBC

The Challenge – Foreign Branch Deposits • Administration of system (assessment of premia, etc.) • Differential treatment of home/host depositors • Coverage by home country • Systemic relevance of foreign branch deposit taking function? • Capacity of home country deposit insurer? • Coverage by host country • Reliance on home country supervision? • High recovery costs EBK / CFB / SFBC

Cross-border Cooperation • Acknowledge home/host country interests • Primary concern for stability of the domestic financial system • Resulting information needs • Acknowledge limitations of domestic deposit insurance schemes • Achieve level playing field by agreeing on comparable coverage limits, insurance premium, topping-up arrangements, etc. EBK / CFB / SFBC

Conclusion • Design a deposit protection regulation to permit failure of the bank and to preserve systemically important functions • Whether deposit-taking is systemically significant depends on the structure of the financial industry • Acknowledge national incentives – primary concern for stability of the domestic financial system • Forge agreement on division of tasks between home/ host deposit insurer that is incentive compatible EBK / CFB / SFBC