Download

1 / 15

150 likes | 320 Vues

November 2009. Asset Building in Washington State. Why promote asset building?. Asset Building means improving savings and financial skills, behaviors and outcomes for working families

E N D

November 2009 Asset Building in Washington State

Why promote asset building? • Asset Building means improving savings and financial skills, behaviors and outcomes for working families • At least 30% of WA state residents are asset poor – without liquid savings to maintain their household for more than three months. • At least 25% low and moderate income folks do not have and/or use a bank or credit union account

Why promote asset building? • Average American credit card debt is $8,500 – 15% higher than 2000 • 43% households spend more than they earn annually • 44% workers say they live “pay-check to paycheck” in 2007, up from the prior year • BUT, research shows that savings and ownership of assets is possible for low income families • The TIME IS NOW to focus on savings and asset building – economic crisis has sobered up our national spending spree… • Across WA, communities are taking action and beginning to show results

Asset Building Update • State funds have helped start and sustain 15 local asset building coalitions since 2007 • WABC is promoting policies to support savings, financial education and consumer protection • Over 85 WABC organizational members; WABC e-newsletter sent to over 1000 recipients

WABC members • Community action, housing & social service agencies • United Ways • Federal, state & local government agencies • Banks, credit unions and regulatory groups • Advocacy and organizing groups • Native and tribal entities • Micro-enterprise providers

WABC Policy Principles • Expand Financial Skills For Success • Increase financial fitness in schools and for adults; integrate into public services • Help People Save And Invest • Support small biz development, IDAs, home ownership, savings and EITC • Remove Barriers To Gaining And Keeping Assets • Expand lower cost lending alternatives, regulate predatory lending, eliminate asset limits

WABC Board and Teams Local Coalitions & Statewide Institutions

WABC Vision The homeownership rate is over 70%. People have housing choices and homeownership is feasible all across the state. Mainstream banking is the norm for low income people. Payday loans are gone or significantly reduced, and strong alternatives are offered. AB and financial health is a top priority for governor and legislature. Major policy changes have been made Local AB coalitions flourish and produce outcomes. Low income people are involved at state and local level. Asset Building Vision People are planning for the future, and have opportunities to achieve financial health and security Tribes are providing AB leadership in and outside native communities. People have hope, freedom to choose their future High Level of Involvement of employers on behalf of employees: Incentives, matching, benefits, etc. Tax credits are claimed by those who have earned them. A state EITC-like product is also offered. AB resources come from many sources. Meaningful public, private, nonprofit partnership. AB is talked about, embraced and funded. Saving is Cool! Social marketing changes behaviors, rewards for saving are offered by FI’s, employers, government, nonprofits, etc. Financial educ. is taught in all schools Financial Health is valued in the same way as physical health, with prevention a public policy issue as well as a family issue

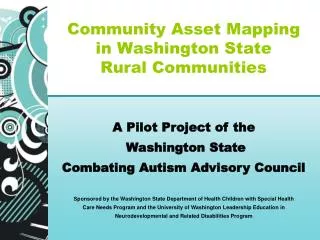

Local Asset Building Projects • In 2005, only one community had organized around asset building – now, 15 coalitions are planning and taking action • Actions include: promoting savings and banking, providing financial literacy and help with credit repair, marketing EITC, and promoting home ownership and business start-up • State funds have leveraged significant private and other funds since 2007 to expand start-up and existing activities

Whatcom San Juan Pend Oreille Okanogan Ferry Skagit Stevens Island Kitsap Clallam Snohomish Chelan Jefferson Spokane Douglas Lincoln King Mason Grays Harbor Grant Kittitas Adams Whitman Pierce Thurston Pacific Lewis Franklin Yakima Garfield Columbia WallaWalla Cowlitz Asotin Skamania Benton Wahkiakum Klickitat Funded in 07-08 and 08-09 Clark New counties funded 08-10 Asset Building Coalitions in WA 10 10

2008-09 Highlights • WABC’s June 2008 Building Assets-Strengthening Communities conference in Yakima inspired and educated 280 leaders and practitioners from across the state • Plan on attending our Nov. 5-6 Conference in Tacoma • Over one million mailing inserts, handbills and posters marketed EITC tax benefits and resulted in an increase of 18% at free tax prep centers • Two local “Bank on” initiatives were launched and a statewide WA Saves campaign promoted savings and financial education

2010-12 Legislative Policy Agenda Building Assets to Access the American Dream • Bank-On Washington Initiative: A statewide bank-on initiative is essential to promote a culture of savings in the state and link tens of thousands of “unbanked” people to mainstream institutions. • Position: Resources to help local coalitions establish and run Bank-On projects • Individual Development Accounts: In order to become self-sufficient, people with low incomes must have the opportunity to save money and build wealth. Washington State’s Individual Development Accounts (IDAs) are matched savings accounts for people with lower incomes that help them save for homes, small businesses and other assets. Participants receive financial training to help them plan a family budget and save. • Position: Dedicated Funding Source for Individual Development Accounts • Elimination/Modification Asset Limits: In addition to using a family's income to determine eligibility for public benefit programs, Washington State also limits eligibility to those with few or no assets (savings, car, etc). If a family has assets over the state’s very low limits, it must deplete longer-term savings in order to receive what is often short-term public assistance. • Position: Eliminate/Modify Asset Limits in public benefits programs

2010-12 Legislative Policy Agenda Building Assets to Access the American Dream • Increase and Strengthen Financial & Consumer Education: There are a lack of resources for Washington state consumers for financial and consumer education. Resources are difficult to find, marketing is not wide spread or coordinated, and there is a lack of knowledge about the best curriculum offered. Washington state needs a fully developed, robust network of financial education and coaching resources across the state. • Position: Pilots and Resource Bank for Financial and Consumer Education • College Savings Incentive/Children Savings Accounts: Post-secondary education is one of the best investments an individual can make in his or her economic future. Unfortunately, escalating costs discourage many from pursuing post-secondary education. For low-income families, the net out-of-pocket cost of a four-year public university education is estimated to be as high as 39 percent of total income. • Position: Create Incentives for College Savings/Open Children Savings Accounts

WABC Needs You! • Horizon communities can become involved with local coalitions • This is not a “program” of a local agency, but a “movement” requiring involvement from all sectors – Horizon members and areas • Now is the time to act to increase financial fitness, savings and asset building policies and protect people • Lots of ways to get involved -- Please join us!

Contact us For more information contact: Paul Knox, WABC Executive Director Phone: 360.977.0476 Email: pknox@washingtonabc.org www.washingtonabc.org