Download

1 / 23

230 likes | 385 Vues

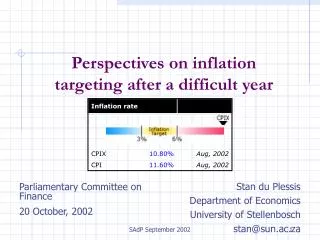

Inflation rate. CPIX. 10.80%. Aug, 2002. CPI. 11.60%. Aug, 2002. Perspectives on inflation targeting after a difficult year. Stan du Plessis Department of Economics University of Stellenbosch stan@sun.ac.za . Parliamentary Committee on Finance 20 October, 2002. Issues covered.

E N D

Inflation rate CPIX 10.80% Aug, 2002 CPI 11.60% Aug, 2002 Perspectives on inflation targeting after a difficult year Stan du Plessis Department of Economics University of Stellenbosch stan@sun.ac.za Parliamentary Committee on Finance 20 October, 2002 SAdP September 2002

Issues covered • Recent concerns about domestic inflation • The present debate on inflation targeting • Reasons for inflation targeting • Evaluating inflation targeting • Some suggestions for domestic policy SAdP September 2002

Present problems: I • Moderate (but rising) domestic inflation • undermines the credibility of the framework for monetary policy • SARB’s track record and hence credibility harmed • Government (having set the target) also suffers credibility loss SAdP September 2002

Recent international inflation experience Green indicates an inflation targeting country SAdP September 2002

Present problems: II • Inflation forecasts not credibly within the target range in years to come • undermines the credibility of policy making at the SARB • …however, there are no expectations of runaway inflation SAdP September 2002

Result: credibility deficit for monetary policy BER survey of CPIX inflation expectations (in 3rd quarter of 2002) SAdP September 2002

Issues covered • Recent concerns about domestic inflation • The present debate on inflation targeting • Reasons for inflation targeting • Evaluating inflation targeting • Some suggestions for domestic policy SAdP September 2002

Present debate on inflation targeting • Three broad camps • Group A • Against inflation targets • …arguing that government’s priorities are wrong • Group B • Targets are good, but the present targets are not • … [some] arguing that the target should be higher in a developing country • Hence the SARB is (forced into) setting policy incorrectly • Group C • The present targeting regime is good • Hence the SARB’s decisions are sensible • (Except that it may be time for the escape clause) SAdP September 2002

Background to the debate on inflation targeting • 3 observations about modern Central Banking • Increasing adoption of explicit targets for monetary policy • Also in developing countries • Central Banks are gaining independence • Associated with lower inflation • At no cost to growth • Helping the poor (who cannot hedge against inflation) • Credibility increasingly recognised as crucial to the success of monetary policy • Inflation targeting incorporates all of the above in a disciplined framework for monetary policy SAdP September 2002

Reasons for adopting inflation targeting as a framework • “Negative” reasons • Lack knowledge for ‘fine tuning’ monetary policy • Ensures consistent monetary policy over time • Experience: • Capital flows cause problems for alternative anchors (for example, exchange rate targets) • “Positive” reasons • Solves the “democratic deficit” • The problem of a (very) powerful, unelected, policymaking institution in a democratic country • Helps to build credibility • Good track record internationally SAdP September 2002

Inflation targeting is an increasingly popular tool for building credibility SAdP September 2002 Source: Mishkin and Schmidt-Hebbel, 2001

Evaluating inflation targeting • Distinguish a number of different aspects of inflation targeting • A. Ultimate objectives • B. Transparency • C. Final responsibility (the institutional design, accountability and independence of the MPC does not concern this meeting directly) (Government decisions have been underlined on the following slides) SAdP September 2002

A. Ultimate objectives • 3-step procedure: • Government defines clear goals for Central Bank • “goal dependence” • e.g. an inflation target • Empower the SARB to pursue those goals • “Instrument independence” • Hold the SARB accountable for the achieving the goals • Reasonableness of the target affects the government’s credibility • Present situation • SARB has instrument independence • Treasury sets the inflation target SAdP September 2002

B. Transparency • Public must be able to monitor the goals • Major problem - control lag in monetary policy implies separate evaluation of: • The policy framework • evaluated with the track record (mainly on inflation) • Policy stance, given the framework • forward looking evaluation using the inflation forecast • SARB’s credibility affected by both the framework and the stance of policy SAdP September 2002

B. Transparency at SARB • Fair degree of “formal” transparency • But some shortcomings: • lack of openness • No published model, no information of conditioning variables • Policy signal of the fan chart cannot be monitored • Hence, public cannot evaluate the stance of policy • The choice of a band as opposed to a point target • …and narrowing of the range in 2004 by 33% • “Hardening” of the range’s upper edge • does not reflect uncertainty of transmission mechanism • undermines the evaluation of the policy framework and the credibility of the SARB SAdP September 2002

International experience with the design of inflation targets SAdP September 2002

Further shortcomings • MPC implements a forecast target… • specified as an average over a calendar year • this does not give a clear policy signal • and makes timing difficult as monetary policy is set continuously and not for periods matching the calendar year • Further, the average inflation rate over a calendar year is a ‘derived’ concept, and hard for the public to understand SAdP September 2002

MPC’s target is tied to the calendar year • would be preferable to have a rolling horizon (say 2 years) for the forecast target • This would reflect the duration of the transmission mechanism more precisely than calendar year averages • Allows for adjusting the target when opportune • as opposed to tying these adjustments to calendar years SAdP September 2002

Issues covered • Recent concerns about domestic inflation • The present debate on inflation targeting • Reasons for inflation targeting • Evaluating inflation targeting • Some suggestions for domestic policy SAdP September 2002

Recommendations: • Clarify the target as point-target with tolerance range • new target could be 6% at a rolling 2 year horizon • … with 2% tolerance range on either side • (Presently, the SARB is aiming at the upper end of the 3-6% range) SAdP September 2002

Benefits of this clarification: : • Provides a clear policy signal to the MPC for setting the stance of monetary policy • in contrast with the target as “calendar annual averages” • SARB target remains 6% • But takes account of uncertainty in the realisation of inflation on both sides of the target • allowing credibility to be built for monetary policy • allowing scope for lowering the target at an opportune time • Removes the need for an escape clause • Avoiding the associated credibility problem SAdP September 2002

Credibility costs of these adjustments • Government: • Effectively the forecast target remains unchanged at 6% • Government not seen to reverse policy in ‘hard times’ • Avoid impression that goal posts have been shifted • SARB • Cost in re-educating public about adjusted framework for monetary policy • Have to emphasise the forward and backward looking aspects and 2 yearrolling policy horizon • But long term gain in credibility of improved target design SAdP September 2002

The end SAdP September 2002