Triple Bottom Line Accounting

110 likes | 347 Vues

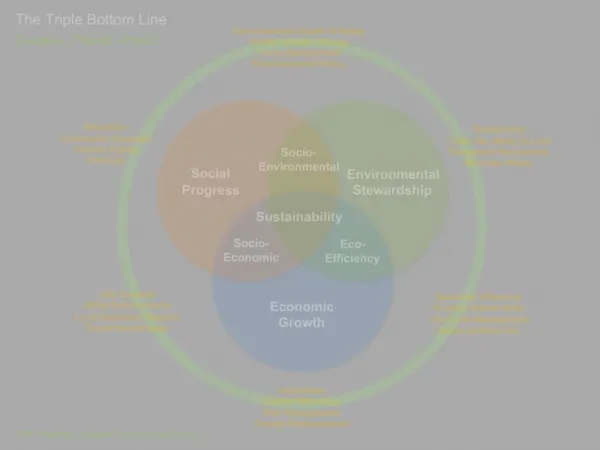

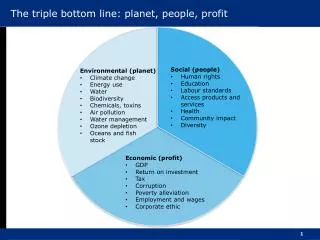

Triple Bottom Line Accounting. The 3-Legged Stool A tool used to measure an organization’s activities Measurements include more than simple economic indicators 1 – Social Accounting 2 – Ecological Accounting 3 – Economic Accounting. Social Accounting.

Triple Bottom Line Accounting

E N D

Presentation Transcript

Triple Bottom Line Accounting • The 3-Legged Stool • A tool used to measure an organization’s activities • Measurements include more than simple economic indicators • 1 – Social Accounting • 2 – Ecological Accounting • 3 – Economic Accounting

Social Accounting • The well-being of all stakeholders are taken into account. • Seeks to benefit as many social constituencies as possible • Does not exploit or endanger any group

Social Accounting • TBL business would: 1 – Not knowingly use child labor 2 – Pay fair salaries to all of it’s workers 3 – Maintain safe work environment 4 – Not seek to exploit community

Ecological Accounting • Refers to sustainable environmental practices • Seeks to benefit the natural order as much as possible, or at at minimum, not to harm the environment. • Seeks to curtail environmental impact, and attempts to reduce their ecological footprint.

Ecological Accounting • Environmental sustainability may actually be more profitable for a firm in the long run • Ecological accounting indicators are more easily quantified and standardized than indicators for social accounting • Measuring environmental impact is quantitative and easy to display • Measuring social impact is qualitative and therefore more easily subjected to debate

Economic Accounting • Not the same as traditional bottom line of everyday commerce • Within the framework of sustainability, ‘profit’ is the economic benefit enjoyed by the host society • Therefore, TBL approach shouldn’t be interpreted as traditional corporate bottom line plus social and environmental impact accounting

Relevance? • TBL is directly related to environmental management in that it gives ecological sustainability equal weight to economics and social factors • Economy may grow, but environmental and social conditions often offset that growth

Why Triple Bottom Line Earth’s carrying capacity cannot support our current levels of exploitation and consumption The collective ecological footprint of the planet’s population is unsustainable, and the current trends of growth and environmental degradation suggest we are going to encounter major problems in the near future

Conclusion • Triple Bottom Line Accounting is an innovative approach to measuring growth • Economic measurements alone are not sufficient indicators of progress • There is a need to go beyond parochial analyses that disregard very important aspects of our environment and society

Sources • Adam, C. (2003). Profit and principles: Finding a balance with the triple bottom line. [Electronic version]. Water Science and Technology: Water Supply, 3(1), 405-410. • Elkington, John. (1999). Cannibals with Forks: The Triple Bottom Line of 21st Century Business. New York: New Society Publishers. • Foran, B., Lenzen, M., Dey, C., & Bilek, M. (2005). Integrating sustainable chain management with triple bottom line accounting. [Electronic version]. Ecological Economics, 52(2), 143- 157. • Heller, T. (2002). Profitable environmentalism. [Electronic version]. Foreign Policy, (128), 13. • Henriques, Adrian; Richardson, Julie. (2004). The Triple Bottom Line: Does it all add up? Assessing the sustainability of business and CSR. Sterling VA: Earthscan Publications Ltd. • Langholz, J. A. (2002). External partnering for the triple bottom line: People, profits and the protection of biodiverity. [Electronic version]. Corporate Environmental Strategy, 9(2), 145-154. • Norman, Wayne; Macdonald, Chris. (2003). Getting to the Bottom of the Triple Bottom Line. Retrieved October 12, 2007, from <http://www.businessethics.ca/3bl/triple-bottom- line.pdf> • Maroochy Shire Council. (2007). Triple Bottom Line Reporting. Retrieved October 12, 2007, from <http://www.maroochy.qld.gov.au/sitePage.cfm?code=tbl_reporting>