Budgeting: Linking Business Objectives & Financial Plans

E N D

Presentation Transcript

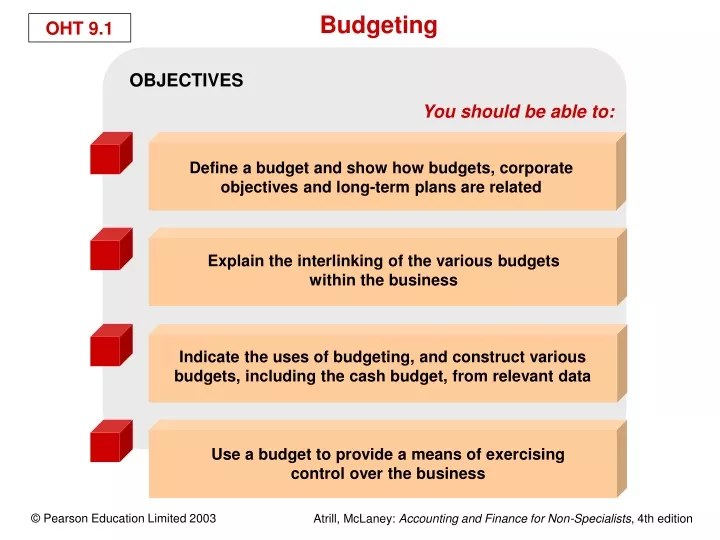

OBJECTIVES You should be able to: Define a budget and show how budgets, corporate objectives and long-term plans are related Explain the interlinking of the various budgets within the business Indicate the uses of budgeting, and construct various budgets, including the cash budget, from relevant data Use a budget to provide a means of exercising control over the business Budgeting

Identify business objectives Consider options Evaluate options and make a selection Prepare short-term plans (budgets) The planning process

Trade creditors budget Tradedebtors budget Cash budget Raw materials purchases budget Direct labour budget Capital expenditure budget Overheads budget Sales budget Finished stock budget Raw materials stock budget Productionbudget The interrelationship of various budgets

Promote forward- thinking and identification of short-term problems Help co-ordinate the various sections of the business Budgets Able to motivate managers to better performance Provide a basis for a system of control Provide a system of authorisation Budgets are seen as having five main benefits to the business

Sales budget 78 76 Budgeted profit and loss 73 Overheads budget Cash budget 63 46 Budgeted balance sheet Purchases budget 35 Production budget 21 40 60 0 20 80 100 Frequency of preparation (%) Preparation of budgets in SMEs Source:Reproduced from Figure 16 on p. 22 from Financial Management and Working Capital Practices in UK SMEs, Business Development Centre,Manchester Business School (Chittenden, F., Poutziouris, P. and Michaelas, N.,1998), reprinted by kind permission of the authors

Jan Feb Mar Apr May June £000£000£000£000£000£000 Receipts Debtors 60 52 55 55 60 55 Payments Creditors 30 30 31 26 35 31 Salaries and wages 10 10 10 10 10 10 Electricity 14 9 Other overheads 2 2 2 2 2 2 Van purchase 11 Total payments 42 42 68 38 47 52 Cash surplus 18 10(13) 17 13 3 Cash balance 30 40 27 44 57 60 An example of a budget – the cash budget

Identify business objectives Consider options Evaluate options and make a selection Prepare budgets Perform and collect information on actual performance Respond to variances and exercise control Revise plans (and budgets) if necessary The planning and control process

The difference between the profit as shown in the original budget and the profit as shown in the fixed budget for the period Sales volume variance The difference between the actual sales figure for the period and the sales figure as shown in the flexed budget Sales price variance Sales variances

The difference between the actual direct material cost and the direct material cost according to the flexed budget (standard usage for the actual output) Total direct material variance The difference between the actual quantity of direct materials used and the quantity of direct material according to the flexed budget (standard usage for actual output). This quantity is multiplied by the standard direct material cost per unit Direct material usage variance The difference between the actual cost of the direct material used and the direct material cost allowed (actual quantity of material used at the standard direct material cost) Direct material price variance Materials variances

Total direct materials variance Direct materials usage variance Direct materials price variance Relationship between the total, usage and price variances of direct materials

The difference between the actual direct labour cost and the direct labour cost according to the flexed budget (standard direct labour hours for the actual output) Total direct labour variance Direct labour efficiency variance The difference between the actual direct labour hours worked and the number of direct labour hours according to the flexed budget (standard direct labour hours for the actual output). This figure is multiplied by the standard direct labour rate per hour The difference between the actual cost of the direct labour hours worked and the direct labour cost allowed (actual direct labour hours worked at the standard labour rate) Direct labour rate variance Labour variances

Fixed overheads spendingvariance The difference between the actual fixed overhead cost and the fixed overhead cost according to the flexed (and the original) budget Fixed overhead variance

Budgeted profit All favourable variances plus All adverse variances minus equals Actual profit Relationship between the budgeted and actual profit

A serious attitude taken to the system by all levels of management Clear demarcation between areas of managerial responsibility Budget targets being reasonable Established data collection, analysis and dissemination routines Reports aimed at individual managers Fairly short reporting periods Variance reports being produced shortly after the end of the reporting period Action being taken to get operations back under control Making budgetary control effective

The existence of budgets generally tends to improve performance Demanding, yet achievable, budget targets tend to motivate better than less demanding targets Unrealistically demanding targets tend to have the adverse effect on managers’ performance The participation of managers in setting their targets tends to improve motivation and performance Behavioural aspects of budgetary control