Lecico Egypt: Investment Recommendation for Growth and Recovery Potential

Lecico Egypt is an established international producer of sanitary ware and tiles, with a competitive edge through significantly lower production costs compared to European rivals. The company is set to expand its ceramic and brassware production, backed by a robust 70% capacity increase in tile production. Analysts forecast a 27% CAGR in net income over the next five years. While challenges exist in the regional political climate and EU demand, strategic initiatives and cost efficiency position Lecico for promising growth. Target price: EGP 21.4, with an upside based on manufacturing recovery and improved capacity.

Lecico Egypt: Investment Recommendation for Growth and Recovery Potential

E N D

Presentation Transcript

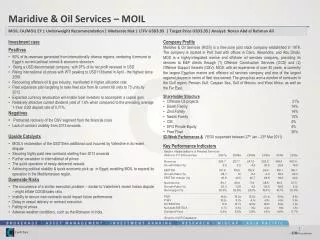

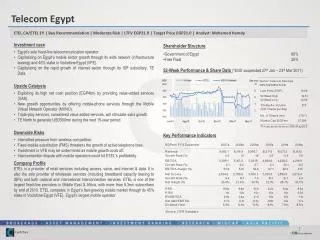

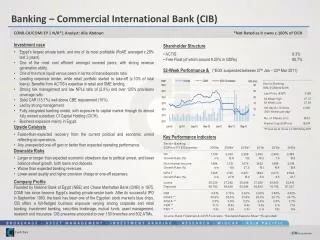

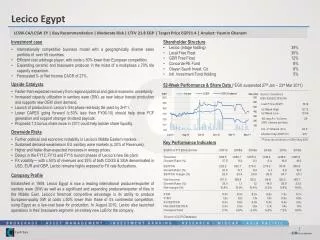

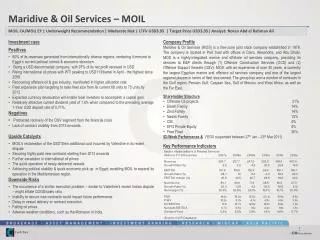

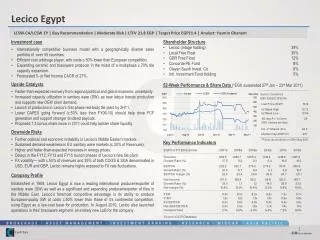

Lecico Egypt LCSW.CA/LCSW EY | Buy Recommendation | Moderate Risk | LTFV 21.8 EGP | Target Price EGP21.4 | Analyst: Yasmin Ghanem Investment case • Internationally competitive business model with a geographically diverse sales portfolio of over 55 countries. • Efficient cost arbitrage player, with costs c.50% lower than European competition. • Expanding ceramic and brassware producer in the midst of a multiphase c.70% tile capacity expansion. • Forecasted 5- yr Net Income CAGR of 27%. Upside Catalysts • Faster-than-expected recovery from regional political and global economic uncertainty. • Increased capacity utilization in sanitary ware (SW), as new labour boosts production and supports new OEM client demand. • Launch of production in Lecico’s first-phase red-body tile plant by 2H11. • Lower CAPEX going forward (c.50% less than FY06-10) should help drive FCF generation and support stronger dividend payouts. • Proposed 1:3 bonus share issue in 2011 could help bolster share liquidity. Downside Risks • Further political and economic instability in Lecico’s Middle Eastern markets. • Sustained demand-weakness in EU sanitary ware markets (c.30% of Revenues). • Higher and faster-than-expected increases in energy prices. • Delays in the FY12, FY13 and FY15 launch phases of Lecico’s new tile plant • FX volatility— with c.50% of revenues and 35% of both COGS & SGA denominated in USD, EUR and GBP, Lecico remains highly exposed to FX rate fluctuations. • Shareholder Structure • Lecico (Intage holding) 39% • Local Free Float 30% • GDR Free Float 12% • Concorde PE Fund 8% • Olayan Saudi Invest. Co. 6% • Intl. Investment Fund Holding 5% • 52-Week Performance & Share Data (*EGX suspended 27th Jan – 23rd Mar 2011) Key Performance Indicators Company Profile Established in 1959, Lecico Egypt is now a leading international producer/exporter of sanitary ware (SW) as well as a significant and expanding producer/exporter of tiles in the Middle East. Lecico’s foremost competitive advantage is its ability to produce European-quality SW at costs c.50% lower than those of it’s continental competition, using Egypt as a low-cost base for production. In August 2010, Lecico also launched operations in their brassware segment- an entirely new LoB for the company.