Monieness and Options

460 likes | 667 Vues

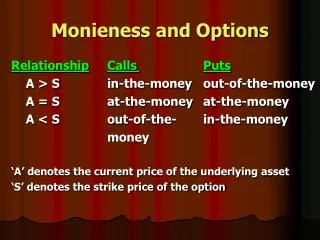

Monieness and Options. Relationship Calls Puts A > S in-the-money out-of-the-money A = S at-the-money at-the-money A < S out-of-the- in-the-money money ‘A’ denotes the current price of the underlying asset ‘S’ denotes the strike price of the option. Value of an Option.

Monieness and Options

E N D

Presentation Transcript

Monieness and Options RelationshipCalls Puts A > S in-the-money out-of-the-money A = S at-the-money at-the-money A < S out-of-the- in-the-money money ‘A’ denotes the current price of the underlying asset ‘S’ denotes the strike price of the option

Value of an Option The two components are, • Intrinsic Value: of call = Max [A-S, 0] of put = Max [S-A, 0] • Time value: It is the value in excess of the intrinsic value and indicates option’s potential to become more valuable before it expires. It decays with passage of time.

How is Value of Options Affected*? *American Options

Call Option Pay-off Diagram: Net payoff on call Strike Price Price of underlying asset

Put Option Pay-off Diagram: Net payoff on put Strike Price Price of underlying asset

Options other than Calls and Puts • Convertible in bonds: purchaser buys a straight bond and a call option • Callable bonds: purchaser buys a straight bond and sells a call option to issuer • An equity share can be viewed as a call option on the assets of a company.

Buying and Selling Stock:Long Position Profit E 0 MP (T) 400 (-) 400 Loss

Buying and Selling Stock:Short Position Profit 240 240 0 MP (T) E Loss

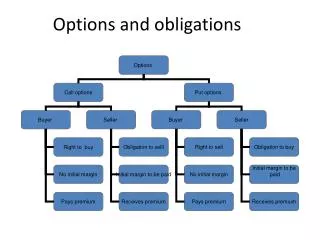

Elementary Investment Strategies • Long Call • Short Call • Long Put • Short Put

Long Call This refers to the purchase of a call Profit 400 E 0 MP (T) 440 (-) 40 Loss These are cash flows when a bullish Investor buys a 3-month call on the Stock with an exercise price of Rs.400 Per share by paying a premium of Rs.40

Short Call This involves writing a call without owning the underlying asset Profit (+) 40 440 0 MP (T) E 400 Loss These cash flows relate to writing a 3-month call on a stock at an exercise price of Rs.400 per share by receiving a premium of Rs.40.

Long Put This involves buying a put – the right to sell the Underlying asset at a specified price Profit (+) 216 E 240 0 MP (T) 216 (-) 24 Loss These cash flows relate to a bearish investor Buying 3-month put with a exercise price of Rs.240 per share by paying a premium of Rs.24

Short Put This involves writing a put Profit E 0 MP (T) 240 216 (-) 216 Loss These cash flows relate to a bullish investor Writing a put at an exercise price of Rs.240 Per share receiving a premium of Rs.24.

Complex Investment Strategies • Covered Call Writing • Protective Put • Straddles • Strangles • Spreads

Covered Call Writing It involves buying the stock and writing call on that. Profit (+)48 E MP (T) 302 350 These are cash flows when we buy 100 shares @310 and write a May 350 call for Rs.8 so that initial Investment is Rs.302 (-)302

Covered Call Writing: CF0 = (Rs.302) MP (T) At Time T NCF Sell Stock Buy Call CF(T) 270 270 0 270 -32 290 290 0 290 -12 310 310 0 310 8 330 330 0 330 28 350 350 0 350 48 370 370 -20 350 48

Covered Call:Why better than stock or only short calls? • Reduces the risk of uncovered call writing. • Downside risk is reduced by the premium amount. • Loss of upward gains can be minimized by rolling up the exercise price. • When call ends up out-of-the-money, profits increase by every dollar by which the stock price exceeds the original price. • Has a lower B.E.P. compared to only stock. • Writing a covered call at lower exercise price is conservative, it reduces the loss but also the upward gains. • Writing at higher exercise price is risky. Downside loss is higher (less protective) and also gains are higher. • A short holding period reduces the stock movement possibility and is the best.

Protective Put It involves buying the stock and buying put on that. Profit E MP (T) 270 312 (-)42 These are cash flows when buy 100 shares @ Rs.310 and buy a Jun 270 put for Rs.2 so that initial Investment is Rs.312 Loss

Protective Put • Guards against fall and also participate in gains. Put ensures min. selling price for stock. • Gain on upside movement is restricted by the premium. • Smaller downside risk and smaller upward gains and higher BEP. • Higher strike price costs maximum but also provides maximum protection. Reduces the profits maximum. • Lower strike price costs less, less protective and reduces profits less. • Long holding period has chances of recovery of time value due to more chances of price movements.

Synthetic Put and Call • A synthetic put involves long calls and short sale of an equal number of shares of stock. • Synthetic call involves buying stock and an equal number of puts and is nothing but protective put.

Long Straddle Involves buying a put and a call, each with same exercise price and same time to expiration. Profit 247 E1 E2 MP (T) 247 373 (-)63 310 Buying a Jun 310 call for Rs.21 And Jun 310 put for Rs.42 per Share. Initial investment Rs63. Loss

Short Straddle Involves selling a put and a call, each with same exercise price and same time to expiration. Profit (63) E2 E1 MP (T) 247 310 373 Loss (-)247

Straddle Variants Straps: A bullish variation of straddle, involves two calls and one put. Investors are more bullish than bearish and therefore increase calls. Strips: It is a slightly bearish variation of straddle, has long position in two puts and one call and involves one’s bet that the market will go down.

Long Strangle Involves buying a call and a put on the same underlying asset for same expiration period at different exercise prices Profit 247 270 310 E1 E2 MP (T) 333 247 -23 Buy Jun 310 call for Rs.21 and Jun 270 Put for Rs. 2. Initial investment Rs.23. Usually one in-the-money and another Out-of-the-money. Initial investment Can be less than straddle Loss

Spreads • Involve buying of one option and selling of another. • Offer potential for small profit and limit the risk. • Vertical Spreads also called Strike or Money spreads. Could be written as say, July 120/125 Spread. • Horizontal Spreads also called as Time or Calendar Spreads. Could be written as June/July 120 Spread.

Spreads For Vertical Spreads: • A July 120/125 call spread is a net long position and is called Buying the Spread, sometimes referred to as Debit Spread. • A July 120/125 put spread is a net short position and is called Selling the Spread, sometimes referred to as Credit Spread.

Spreads For Horizontal Spreads: • A June/July 120 call spread is a net short position and is called Selling the Spread, sometimes referred to as Credit Spread. • A July/June 120 call spread is a net long position and is called Buying the Spread, sometimes referred to as Debit Spread.

Vertical Spread (Across Strike Prices) Involves buying an option and selling another option of the same type and time to expiration but with different exercise price Profit + 30 E MP (T) 270 320 350 - 50 Bullish vertical spread using calls wherein we Buy Mar 270 calls for Rs.58 and sell Mar 350 Calls for Rs.8 i.e. buy lower strike price and Sell higher strike price calls. Loss

Vertical Spread Involves buying an option and selling another option of the same type and time to expiration but with different exercise price Profit + 68 E MP (T) 270 282 350 - 12 Bullish vertical spread using puts wherein We buy Mar270 put for Rs.2 and sell Mar 350 put for Rs.70. Loss

Vertical Spread . Profit +59 E MP (T) 270 329 350 -21 Bearish vertical spread wherein Sell Jun 270 call for Rs.71 and buy Jun 350 call for Rs.12. Loss

Vertical Spread . Bearish vertical spread using Puts wherein Buy Mar 350 put for Rs.70 and sell Mar 270 put for Rs.2 Profit +12 E MP (T) 270 282 350 -68 Loss

Horizontal Spreads(Across Expiration Months) • Involve buying an option and selling another of same type with same exercise price but with different expiration time. • In a horizontal bull spread, we buy back month and sell the front month. In a horizontal bear spread, we buy front month and sell back month. • Horizontal bull spread has similar pay-off as that of a short straddle and horizontal bear spread has similar payoff as that of a long straddle.

Diagonal Spreads They are vertical and horizontal at the same time i.e. the are across both strike price and expiration month.

Butterfly Spread • Involves four options, all calls or all puts. • All have same expiration month and same underlying asset. • One option has high strike price, one has low strike price and two have same strike price which is between those of high strike and low strike. • Two middle strike price are sold and the two end options are purchased.

Reverse Butterfly or Sandwich Spreads • This is strategy reverse of the butterfly spread. • The two middle strike price options are purchase and the two end strike price options are sold.

Evaluation of the Strategies • Transaction costs have not been considered and should be kept in mind. • Bid-ask spreads may affect payoffs. • They are not dividend protected. • Margin requirements are applicable to option writing. • Possibility of early exercise may pose new risks. • Timing of cash flows can make a difference.

Futures vs. Options: Performance • Option purchasers do not post margins since they have no obligations • An option clearing house serves the similar functions as those of clearing associations in futures trading • Option writers have to post margins to clearing houses • Options are also OTC and dealers may require margins or guarantees.

Illustration 1 Consider the price of the stock at $165.125. Buy 100 shares of stock and write one August 170 call contract at a premium of $3.25. Hold the position until expiration. Determine the profits and graph the results. Identify the breakeven stock price at expiration, the maximum profits, and the maximum loss.

Illustration 2 Consider the price of the stock at the same level as in the previous illustration i.e. $165.125. Now assume that you buy 100 shares of stock and buy one August 165 put contract at a premium of $4.75. Hold the position till expiration. Determine the profits and graph the results. Identify the breakeven stock price at expiration, the maximum profits, and the maximum loss.

Illustration 3 A call option with a strike price of $50 costs $2. A put option with a strike price of $45 costs $3. Explain how a strangle can be created from these two options. What is the pattern of profits from the strangle?

Illustration 4 A call with a strike price of $50 costs $6. A put with the same strike price and expiration date costs $4. Construct a table that shows the profits from a straddle. For what range of stock prices would the straddle lead to a loss?

Illustration 5 • Discuss the main objectives of covered call and protective put vis-à-vis simple call and put strategies. • What is synthetic puts and synthetic calls?

A Transaction on an Option Exchange . 1a 1b 2a Options Exchange 3 2b Buyer 6a Buyer’s Broker Buyer’s Broker’s Floor Broker Seller’s Broker’s Floor Broker Seller’s Broker 6b Seller 5a 5b 7a 7b 4 8a 8b Options Clearing House 9a 9b Buyer’s Broker’s Clearing Firm Buyer’s Broker’s Clearing Firm • 1a 1b Buyer and seller instruct their respective brokers to conduct an option transaction. • 2a 2b Buyer’s and seller’s brokers request their firm’s floor brokers execute the transaction. • Both floor brokers meet in the pit on the floor of the options exchange and agree on a price. • Information on the trade is reported to the clearinghouse. • 5a 5b Both floor brokers report the price obtained to the buyer’s and seller’s brokers. • 6a 6b Buyer’s and seller’s brokers report the price obtained to the buyer and seller. • 7a 7b Buyer deposits premium with buyer’s broker. Seller deposits margin with seller’s broker. • 8a 8b Buyer’s and seller’s brokers deposit premium and margin with their clearing firms. • 9a 9b Buyer’s and seller’s brokers’ clearing firms deposit premium and margin with clearinghouse. Note: Either buyer or seller (or both) could be a floor trader, eliminating the broker and floor broker.