TAX DIVERSIFICATION

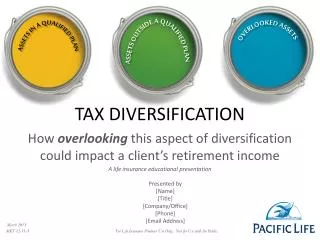

ASSETS OUTSIDE A QUALIFIED PLAN. ASSETS IN A QUALIFIED PLAN. OVERLOOKED ASSETS. TAX DIVERSIFICATION. How overlooking this aspect of diversification could impact a client’s retirement income A life insurance educational presentation. Presented by [Name] [Title] [Company/Office] [Phone]

TAX DIVERSIFICATION

E N D

Presentation Transcript

ASSETS OUTSIDE A QUALIFIED PLAN ASSETS IN A QUALIFIED PLAN OVERLOOKED ASSETS TAX DIVERSIFICATION How overlooking this aspect of diversification could impact a client’s retirement income A life insurance educational presentation Presented by [Name] [Title] [Company/Office] [Phone] [Email Address] March 2013 For Life Insurance Producer Use Only. Not for Use with the Public. MKT 12-51A

Retirement Income - Will There Be ENOUGH? 2/3 of investors between age 21 and 50 doubt they will have ENOUGH MONEY FOR RETIREMENT* 64%of Gen X and Gen Y investors expect that retirement income will come FROM NON-RETIREMENT ACCOUNTS* • 1/3of small-business owners do not have a PERSONAL OR BUSINESS-SPONSORED RETIREMENT ** *“Gen X and Y Investors Worry Retirement Savings Won’t Be Enough,” Michael S. Fischer, AdvisorOne, March 9, 2012. **”Many Small-Business owners aren’t prepared for Retirement,” Laura Petrecca, USA Today, March 1, 2012. For Life Insurance Producer Use Only. Not for Use with the Public.

What We’ll Cover • Retirement income – will it be enough? • 3 buckets of tax diversification • How tax diversification works • What is in the overlooked assets bucket? For Life Insurance Producer Use Only. Not for Use with the Public.

Tax Diversification Why failure to diversify tax liabilities at retirement could potentially hurt your client's retirement income ASSETS IN A QUALIFIED PLAN ASSETS OUTSIDE A QUALIFIED PLAN OVERLOOKED ASSETS For Life Insurance Producer Use Only. Not for Use with the Public.

Tax Diversification Why failure to diversify tax liabilities at retirement could potentially hurt your client's retirement income ASSETS IN A QUALIFIED PLAN ASSETS OUTSIDE A QUALIFIED PLAN OVERLOOKED ASSETS • 401(K) • Pension Plans • Traditional IRAs • Taxed at: Income Tax Rates For Life Insurance Producer Use Only. Not for Use with the Public.

Tax Diversification Why failure to diversify tax liabilities at retirement could potentially hurt your client's retirement income ASSETS IN A QUALIFIED PLAN ASSETS OUTSIDE A QUALIFIED PLAN OVERLOOKED ASSETS • 401(K) • Pension Plans • Traditional IRAs • Taxed at: Income Tax Rates • Real Estate • Stocks • Stock Funds • Generally taxed at: Capital Gain Tax Rates For Life Insurance Producer Use Only. Not for Use with the Public.

Tax Diversification Why failure to diversify tax liabilities at retirement could potentially hurt your client's retirement income ASSETS IN A QUALIFIED PLAN ASSETS OUTSIDE A QUALIFIED PLAN OVERLOOKED ASSETS • 401(K) • Pension Plans • Traditional IRAs • Taxed at: Income Tax Rates • Real Estate • Stocks • Stock Funds • Generally taxed at: Capital Gains Tax Rates • Municipal Bonds • Roth IRAs • Life Insurance Retirement Plan (LIRP) • Generally: Tax Free* *For life insurance, Tax-free income assumes, among other things: (1) withdrawals do not exceed tax basis (generally, premiums paid less prior withdrawals); (2) policy remains in force until death; (3) withdrawals taken during the first 15 policy years do not occur at the time of, or during the two years prior to, any reduction in benefits; and (4) the policy does not become a modified endowment contract. See IRC Sections 72, 7702(f)(7)(B), 7702A. Any policy withdrawals, loans and loan interest will reduce policy values and may reduce benefits. For Life Insurance Producer Use Only. Not for Use with the Public.

Tax Diversification Why failure to diversify tax liabilities at retirement could potentially hurt your client's retirement income ASSETS IN A QUALIFIED PLAN ASSETS OUTSIDE A QUALIFIED PLAN OVERLOOKED ASSETS • 401(K) • Pension Plans • Traditional IRAs • Taxed at: Income Tax Rates • Real Estate • Stocks • Stock Funds • Generally taxed at: Capital Gains Tax Rates • Municipal Bonds • Roth IRAs • Life Insurance Retirement Plan (LIRP) • Generally: Tax Free* $100,000 *Tax-free income assumes, among other things: (1) withdrawals do not exceed tax basis (generally, premiums paid less prior withdrawals); (2) policy remains in force until death; (3) withdrawals taken during the first 15 policy years do not occur at the time of, or during the two years prior to, any reduction in benefits; and (4) the policy does not become a modified endowment contract. See IRC Sections 72, 7702(f)(7)(B), 7702A. Any policy withdrawals, loans and loan interest will reduce policy values and may reduce benefits. For Life Insurance Producer Use Only. Not for Use with the Public.

Tax Diversification Why failure to diversify tax liabilities at retirement could potentially hurt your client's retirement income ASSETS IN A QUALIFIED PLAN ASSETS OUTSIDE A QUALIFIED PLAN OVERLOOKED ASSETS • 401(K) • Pension Plans • Traditional IRAs • Taxed at: Income Tax Rates • Real Estate • Stocks • Stock Funds • Generally taxed at: Capital Gains Tax Rates • Municipal Bonds • Roth IRAs • Life Insurance Retirement Plan (LIRP) • Generally: Tax Free* $100,000 *Tax-free income assumes, among other things: (1) withdrawals do not exceed tax basis (generally, premiums paid less prior withdrawals); (2) policy remains in force until death; (3) withdrawals taken during the first 15 policy years do not occur at the time of, or during the two years prior to, any reduction in benefits; and (4) the policy does not become a modified endowment contract. See IRC Sections 72, 7702(f)(7)(B), 7702A. Any policy withdrawals, loans and loan interest will reduce policy values and may reduce benefits. For Life Insurance Producer Use Only. Not for Use with the Public.

Tax Diversification Why failure to diversify tax liabilities at retirement could potentially hurt your client's retirement income ASSETS IN A QUALIFIED PLAN ASSETS OUTSIDE A QUALIFIED PLAN OVERLOOKED ASSETS • 401(K) • Pension Plans • Traditional IRAs • Taxed at: Income Tax Rates • Real Estate • Stocks • Stock Funds • Generally taxed at: Income Tax Rates • Municipal Bonds • Roth IRAs • Life Insurance Retirement Plan (LIRP) • Generally: Tax Free* $100,000 What happens ifIncome Tax Rates go up? *Tax-free income assumes, among other things: (1) withdrawals do not exceed tax basis (generally, premiums paid less prior withdrawals); (2) policy remains in force until death; (3) withdrawals taken during the first 15 policy years do not occur at the time of, or during the two years prior to, any reduction in benefits; and (4) the policy does not become a modified endowment contract. See IRC Sections 72, 7702(f)(7)(B), 7702A. Any policy withdrawals, loans and loan interest will reduce policy values and may reduce benefits. For Life Insurance Producer Use Only. Not for Use with the Public.

Tax Diversification Why failure to diversify tax liabilities at retirement could potentially hurt your client's retirement income ASSETS IN A QUALIFIED PLAN ASSETS OUTSIDE A QUALIFIED PLAN OVERLOOKED ASSETS • 401(K) • Pension Plans • Traditional IRAs • Taxed at: Income Tax Rates • Real Estate • Stocks • Stock Funds • Generally taxed at: Capital Gains Tax Rates • Municipal Bonds • Roth IRAs • Life Insurance Retirement Plan (LIRP) • Generally: Tax Free* $100,000 What happens ifIncome Tax Rates go up? *Tax-free income assumes, among other things: (1) withdrawals do not exceed tax basis (generally, premiums paid less prior withdrawals); (2) policy remains in force until death; (3) withdrawals taken during the first 15 policy years do not occur at the time of, or during the two years prior to, any reduction in benefits; and (4) the policy does not become a modified endowment contract. See IRC Sections 72, 7702(f)(7)(B), 7702A. Any policy withdrawals, loans and loan interest will reduce policy values and may reduce benefits. For Life Insurance Producer Use Only. Not for Use with the Public.

Tax Diversification Why failure to diversify tax liabilities at retirement could potentially hurt your client's retirement income ASSETS IN A QUALIFIED PLAN ASSETS OUTSIDE A QUALIFIED PLAN OVERLOOKED ASSETS • 401(K) • Pension Plans • Traditional IRAs • Taxed at: Income Tax Rates • Real Estate • Stocks • Stock Funds • Generally taxed at: Capital Gains Tax Rates • Municipal Bonds • Roth IRAs • Life Insurance Retirement Plan (LIRP) • Generally: Tax Free* $100,000 What happens ifIncome Tax Rates go up? $15,000 Additional Loss from Taxes: *Tax-free income assumes, among other things: (1) withdrawals do not exceed tax basis (generally, premiums paid less prior withdrawals); (2) policy remains in force until death; (3) withdrawals taken during the first 15 policy years do not occur at the time of, or during the two years prior to, any reduction in benefits; and (4) the policy does not become a modified endowment contract. See IRC Sections 72, 7702(f)(7)(B), 7702A. Any policy withdrawals, loans and loan interest will reduce policy values and may reduce benefits. For Life Insurance Producer Use Only. Not for Use with the Public.

Tax Diversification Why failure to diversify tax liabilities at retirement could potentially hurt your client's retirement income ASSETS IN A QUALIFIED PLAN ASSETS OUTSIDE A QUALIFIED PLAN OVERLOOKED ASSETS • 401(K) • Pension Plans • Traditional IRAs • Taxed at: Income Tax Rates • Real Estate • Stocks • Stock Funds • Generally taxed at: Capital Gains Tax Rates • Municipal Bonds • Roth IRAs • Life Insurance Retirement Plan (LIRP) • Generally: Tax Free* $100,000 $100,000 What happens ifIncome Tax Rates go up? $15,000 Additional Loss from Taxes: *Tax-free income assumes, among other things: (1) withdrawals do not exceed tax basis (generally, premiums paid less prior withdrawals); (2) policy remains in force until death; (3) withdrawals taken during the first 15 policy years do not occur at the time of, or during the two years prior to, any reduction in benefits; and (4) the policy does not become a modified endowment contract. See IRC Sections 72, 7702(f)(7)(B), 7702A. Any policy withdrawals, loans and loan interest will reduce policy values and may reduce benefits. For Life Insurance Producer Use Only. Not for Use with the Public.

Tax Diversification Why failure to diversify tax liabilities at retirement could potentially hurt your client's retirement income ASSETS IN A QUALIFIED PLAN ASSETS OUTSIDE A QUALIFIED PLAN OVERLOOKED ASSETS • 401(K) • Pension Plans • Traditional IRAs • Taxed at: Income Tax Rates • Real Estate • Stocks • Stock Funds • Generally taxed at: Capital Gains Tax Rates • Municipal Bonds • Roth IRAs • Life Insurance Retirement Plan (LIRP) • Generally: Tax Free* $100,000 $100,000 What happens ifIncome Tax Rates go up? $15,000 Additional Loss from Taxes: *Tax-free income assumes, among other things: (1) withdrawals do not exceed tax basis (generally, premiums paid less prior withdrawals); (2) policy remains in force until death; (3) withdrawals taken during the first 15 policy years do not occur at the time of, or during the two years prior to, any reduction in benefits; and (4) the policy does not become a modified endowment contract. See IRC Sections 72, 7702(f)(7)(B), 7702A. Any policy withdrawals, loans and loan interest will reduce policy values and may reduce benefits. For Life Insurance Producer Use Only. Not for Use with the Public.

Tax Diversification Why failure to diversify tax liabilities at retirement could potentially hurt your client's retirement income ASSETS IN A QUALIFIED PLAN ASSETS OUTSIDE A QUALIFIED PLAN OVERLOOKED ASSETS • 401(K) • Pension Plans • Traditional IRAs • Taxed at: Income Tax Rates • Real Estate • Stocks • Stock Funds • Generally taxed at: Capital Gains Tax Rates • Municipal Bonds • Roth IRAs • Life Insurance Retirement Plan (LIRP) • Generally: Tax Free* $100,000 $100,000 What happens ifIncome Tax Rates go up? What happens if Capital Gains Tax Rates go up? $15,000 Additional Loss from Taxes: *Tax-free income assumes, among other things: (1) withdrawals do not exceed tax basis (generally, premiums paid less prior withdrawals); (2) policy remains in force until death; (3) withdrawals taken during the first 15 policy years do not occur at the time of, or during the two years prior to, any reduction in benefits; and (4) the policy does not become a modified endowment contract. See IRC Sections 72, 7702(f)(7)(B), 7702A. Any policy withdrawals, loans and loan interest will reduce policy values and may reduce benefits. For Life Insurance Producer Use Only. Not for Use with the Public.

Tax Diversification Why failure to diversify tax liabilities at retirement could potentially hurt your client's retirement income ASSETS IN A QUALIFIED PLAN ASSETS OUTSIDE A QUALIFIED PLAN OVERLOOKED ASSETS • 401(K) • Pension Plans • Traditional IRAs • Taxed at: Income Tax Rates • Real Estate • Stocks • Stock Funds • Generally taxed at: Capital Gains Tax Rates • Municipal Bonds • Roth IRAs • Life Insurance Retirement Plan (LIRP) • Generally: Tax Free* $100,000 $100,000 What happens ifIncome Tax Rates go up? What happens if Capital Gains Tax Rates go up? $15,000 Additional Loss from Taxes: *Tax-free income assumes, among other things: (1) withdrawals do not exceed tax basis (generally, premiums paid less prior withdrawals); (2) policy remains in force until death; (3) withdrawals taken during the first 15 policy years do not occur at the time of, or during the two years prior to, any reduction in benefits; and (4) the policy does not become a modified endowment contract. See IRC Sections 72, 7702(f)(7)(B), 7702A. Any policy withdrawals, loans and loan interest will reduce policy values and may reduce benefits. For Life Insurance Producer Use Only. Not for Use with the Public.

Tax Diversification Why failure to diversify tax liabilities at retirement could potentially hurt your client's retirement income ASSETS IN A QUALIFIED PLAN ASSETS OUTSIDE A QUALIFIED PLAN OVERLOOKED ASSETS • 401(K) • Pension Plans • Traditional IRAs • Taxed at: Income Tax Rates • Real Estate • Stocks • Stock Funds • Generally taxed at: Capital Gains Tax Rates • Municipal Bonds • Roth IRAs • Life Insurance Retirement Plan (LIRP) • Generally: Tax Free* $100,000 $100,000 What happens ifIncome Tax Rates go up? What happens if Capital Gains Tax Rates go up? $15,000 $35,000 Additional Loss from Taxes: *Tax-free income assumes, among other things: (1) withdrawals do not exceed tax basis (generally, premiums paid less prior withdrawals); (2) policy remains in force until death; (3) withdrawals taken during the first 15 policy years do not occur at the time of, or during the two years prior to, any reduction in benefits; and (4) the policy does not become a modified endowment contract. See IRC Sections 72, 7702(f)(7)(B), 7702A. Any policy withdrawals, loans and loan interest will reduce policy values and may reduce benefits. For Life Insurance Producer Use Only. Not for Use with the Public.

Tax Diversification Why failure to diversify tax liabilities at retirement could potentially hurt your client's retirement income ASSETS IN A QUALIFIED PLAN ASSETS OUTSIDE A QUALIFIED PLAN OVERLOOKED ASSETS • 401(K) • Pension Plans • Traditional IRAs • Taxed at: Income Tax Rates • Real Estate • Stocks • Stock Funds • Generally taxed at: Capital Gains Tax Rates • Municipal Bonds • Roth IRAs • Life Insurance Retirement Plan (LIRP) • Generally: Tax Free* $100,000 $100,000 $100,000 What happens ifIncome Tax Rates go up? What happens if Capital Gains Tax Rates go up? $15,000 $35,000 Additional Loss from Taxes: *Tax-free income assumes, among other things: (1) withdrawals do not exceed tax basis (generally, premiums paid less prior withdrawals); (2) policy remains in force until death; (3) withdrawals taken during the first 15 policy years do not occur at the time of, or during the two years prior to, any reduction in benefits; and (4) the policy does not become a modified endowment contract. See IRC Sections 72, 7702(f)(7)(B), 7702A. Any policy withdrawals, loans and loan interest will reduce policy values and may reduce benefits. For Life Insurance Producer Use Only. Not for Use with the Public.

Tax Diversification Why failure to diversify tax liabilities at retirement could potentially hurt your client's retirement income ASSETS IN A QUALIFIED PLAN ASSETS OUTSIDE A QUALIFIED PLAN OVERLOOKED ASSETS • 401(K) • Pension Plans • Traditional IRAs • Taxed at: Income Tax Rates • Real Estate • Stocks • Stock Funds • Generally taxed at: Capital Gains Tax Rates • Municipal Bonds • Roth IRAs • Life Insurance Retirement Plan (LIRP) • Generally: Tax Free* $100,000 $100,000 $100,000 What happens ifIncome Tax Rates go up? What happens if Capital Gains Tax Rates go up? $15,000 $35,000 Additional Loss from Taxes: *Tax-free income assumes, among other things: (1) withdrawals do not exceed tax basis (generally, premiums paid less prior withdrawals); (2) policy remains in force until death; (3) withdrawals taken during the first 15 policy years do not occur at the time of, or during the two years prior to, any reduction in benefits; and (4) the policy does not become a modified endowment contract. See IRC Sections 72, 7702(f)(7)(B), 7702A. Any policy withdrawals, loans and loan interest will reduce policy values and may reduce benefits. For Life Insurance Producer Use Only. Not for Use with the Public.

Tax Diversification Why failure to diversify tax liabilities at retirement could potentially hurt your client's retirement income ASSETS IN A QUALIFIED PLAN ASSETS OUTSIDE A QUALIFIED PLAN OVERLOOKED ASSETS • 401(K) • Pension Plans • Traditional IRAs • Taxed at: Income Tax Rates • Real Estate • Stocks • Stock Funds • Generally taxed at: Capital Gains Tax Rates • Municipal Bonds • Roth IRAs • Life Insurance Retirement Plan (LIRP) • Generally: Tax Free* $100,000 $100,000 $100,000 What happens ifIncome Tax Rates go up? What happens if Capital Gains Tax Rates go up? $15,000 $35,000 Additional Loss from Taxes: *Tax-free income assumes, among other things: (1) withdrawals do not exceed tax basis (generally, premiums paid less prior withdrawals); (2) policy remains in force until death; (3) withdrawals taken during the first 15 policy years do not occur at the time of, or during the two years prior to, any reduction in benefits; and (4) the policy does not become a modified endowment contract. See IRC Sections 72, 7702(f)(7)(B), 7702A. Any policy withdrawals, loans and loan interest will reduce policy values and may reduce benefits. For Life Insurance Producer Use Only. Not for Use with the Public.

Tax Diversification Why failure to diversify tax liabilities at retirement could potentially hurt your client's retirement income ASSETS IN A QUALIFIED PLAN ASSETS OUTSIDE A QUALIFIED PLAN OVERLOOKED ASSETS • 401(K) • Pension Plans • Traditional IRAs • Taxed at: Income Tax Rates • Real Estate • Stocks • Stock Funds • Generally taxed at: Capital Gains Tax Rates • Municipal Bonds • Roth IRAs • Life Insurance Retirement Plan (LIRP) • Generally: Tax Free* $100,000 $100,000 $100,000 What happens ifIncome Tax Rates go up? What happens if Capital Gains Tax Rates go up? $15,000 $35,000 $0 Additional Loss from Taxes: *Tax-free income assumes, among other things: (1) withdrawals do not exceed tax basis (generally, premiums paid less prior withdrawals); (2) policy remains in force until death; (3) withdrawals taken during the first 15 policy years do not occur at the time of, or during the two years prior to, any reduction in benefits; and (4) the policy does not become a modified endowment contract. See IRC Sections 72, 7702(f)(7)(B), 7702A. Any policy withdrawals, loans and loan interest will reduce policy values and may reduce benefits. For Life Insurance Producer Use Only. Not for Use with the Public.

Tax Diversification Why failure to diversify tax liabilities at retirement could potentially hurt your client's retirement income ASSETS IN A QUALIFIED PLAN ASSETS OUTSIDE A QUALIFIED PLAN OVERLOOKED ASSETS • 401(K) • Pension Plans • Traditional IRAs • Taxed at: Income Tax Rates • Real Estate • Stocks • Stock Funds • Generally taxed at: Capital Gains Tax Rates • Municipal Bonds • Roth IRAs • Life Insurance Retirement Plan (LIRP) • Generally: Tax Free* $100,000 $100,000 $100,000 What happens ifIncome Tax Rates go up? What happens if Capital Gains Tax Rates go up? $15,000 $35,000 $0 Additional Loss from Taxes: Has your client Overlookedthis bucket? *Tax-free income assumes, among other things: (1) withdrawals do not exceed tax basis (generally, premiums paid less prior withdrawals); (2) policy remains in force until death; (3) withdrawals taken during the first 15 policy years do not occur at the time of, or during the two years prior to, any reduction in benefits; and (4) the policy does not become a modified endowment contract. See IRC Sections 72, 7702(f)(7)(B), 7702A. Any policy withdrawals, loans and loan interest will reduce policy values and may reduce benefits. For Life Insurance Producer Use Only. Not for Use with the Public.

LIFE INSURANCE RETIREMENT PLAN(LIRP) OVERLOOKED ASSETS • Municipal Bonds • Roth IRAs • Life Insurance Retirement Plan (LIRP) • Generally: Tax Free* PLUS: More PotentialRetirement Assets TaxAdvantages FinancialProtection • Premium Flexibility • Potential CreditorProtection*** • May Be Funded Through A “C” Corporation Tax-DeferredAccumulation Tax-FreeDistributions* Tax-FreeDeath Benefit** *Tax-free income assumes, among other things: (1) withdrawals do not exceed tax basis (generally, premiums paid less prior withdrawals); (2) policy remains in force until death; (3) withdrawals taken during the first 15 policy years do not occur at the time of, or during the two years prior to, any reduction in benefits; and (4) the policy does not become a modified endowment contract. See IRC Sections 72, 7702(f)(7)(B), 7702A. Any policy withdrawals, loans and loan interest will reduce policy values and may reduce benefits. **For federal income tax purposes, life insurance death benefits generally pay income tax-free to beneficiaries pursuant to IRC Section. 101(a)(1). In certain situations, however, life insurance death benefits may be partially or wholly taxable. Situations include, but are not limited to: the transfer of a life insurance policy for valuable consideration unless the transfer qualifies for an exception under IRC Section. 101(a)(2)(i.e. the transfer-for-value rule); arrangements that lack an insurable interest based on state law; and an employer-owned policy unless the policy qualifies for an exception under IRC Section. 101(j). ***State law may provide life insurance and annuities with certain asset protection benefits. As a general rule, a debtor may not transfer property with the intent to avoid debt due to his creditors. The laws governing asset protection, however, are complex and the consequences of poor planning may be both civil and criminal penalties. Anyone contemplating an asset protection plan should not undertake such without the advice of legal counsel. For Life Insurance Producer Use Only. Not for Use with the Public.

Framing the Details of LIRP Annual Premiums Life InsurancePolicy Insured Supplemental Retirement Income Death Benefit Beneficiary Tax-free Policy Loans/Withdrawals* *Tax-free income assumes, among other things: (1) withdrawals do not exceed tax basis (generally, premiums paid less prior withdrawals); (2) policy remains in force until death; (3) withdrawals taken during the first 15 policy years do not occur at the time of, or during the two years prior to, any reduction in benefits; and (4) the policy does not become a modified endowment contract. See IRC Sections 72, 7702(f)(7)(B), 7702A. Any policy withdrawals, loans and loan interest will reduce policy values and may reduce benefits. For Life Insurance Producer Use Only. Not for Use with the Public.

Benefits of LIRP OVERLOOKED ASSETS • Municipal Bonds • Roth IRAs • Life Insurance Retirement Plan (LIRP) • Generally: Tax Free* 3Tax-free income assumes, among other things: (1) withdrawals do not exceed tax basis (generally, premiums paid less prior withdrawals); (2) policy remains in force until death; (3) withdrawals taken during the first 15 policy years do not occur at the time of, or during the two years prior to, any reduction in benefits; and (4) the policy does not become a modified endowment contract. See IRC Sections 72, 7702(f)(7)(B), 7702A. Any policy withdrawals, loans and loan interest will reduce policy values and may reduce benefits. For Life Insurance Producer Use Only. Not for Use with the Public.

Tax Diversification ASSETS IN A QUALIFIED PLAN • 401(K) • Pension Plans • Traditional IRAs • Taxed at: Income Tax Rates • Overlooking tax diversification could impact a client’s retirement income • Look to the “Overlooked Assets” bucket • LIRP may help a client with “Protection Now, Income Later” ASSETS OUTSIDE A QUALIFIED PLAN • Real Estate • Stocks • Stock Funds • Generally taxed at: Capital Gains Tax Rates OVERLOOKED ASSETS • Municipal Bonds • Roth IRAs • Life Insurance Retirement Plan (LIRP) • Generally: Tax Free* For Life Insurance Producer Use Only. Not for Use with the Public.

This material is not intended to be used, nor can it be used by any taxpayer, for the purpose of avoiding U.S. federal, state or local tax penalties. This material is written to support the promotion or marketing of the transaction(s) or matter(s) addressed by this material. Pacific Life, its distributors and their respective representatives do not provide tax, accounting or legal advice. Any taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor. • Pacific Life refers to Pacific Life Insurance Company and its affiliates, including Pacific Life & Annuity Company. Insurance products are issued by Pacific Life Insurance Company in all states except New York and in New York by Pacific Life & Annuity Company. Product availability and features may vary by state. Each insurance company is solely responsible for the financial obligations accruing under the products it issues. Insurance products and their guarantees, including optional benefits and any fixed subaccount crediting rates, are backed by the financial strength and claims-paying ability of the issuing insurance company. Look to the strength of the life insurance company with regard to such guarantees as these guarantees are not backed by the broker-dealer, insurance agency or their affiliates from which products are purchased. Neither these entities nor their representatives make any representation or assurance regarding the claims-paying ability of the life insurance company. • Please Note: This material is designed to provide introductory information in regard to the subject matter covered and cannot be used in conjunction with the sale of variable universal life insurance. Investment and Insurance Products: Not a Deposit – Not FDIC Insured– Not Insured by any Federal Government Agency – No Bank Guarantee – May Lose Value Pacific Life & Annuity Company Newport Beach, CA (888) 595-6996 • www.PacificLifeandAnnuity.com Pacific Life Insurance Company Newport Beach, CA (800) 800-7681 • www.PacificLife.com For Life Insurance Producer Use Only. Not for Use with the Public. MKT 12-51A