Download

1 / 19

190 likes | 291 Vues

Dive into the creation and evolution of the Federal Reserve, exploring its role in maintaining economic stability through monetary policy. Understand how the Fed's actions impact inflation, employment, and overall economic prosperity.

E N D

Creation of the Fed In 1913 Congress authorized the Federal Reserve as the U.S. central bank (the third time it had created one—the charters of the previous central banks were allowed to expire, largely because Americans expressed suspicion about the East Coast financial establishment controlling credit and currency). Prior to 1913 the country suffered several recessions (panics) in the 19th century and a severe one in 1907; one that was worsened by the inability of private banks to produce the currency demanded by depositors. The 1907 Panic prodded Congress to create our present central bank.

Creation of the Fed • Populist aversion to the concept remained, however—thus, Congress established 12 central banks, supervised by a relatively weak Federal Reserve Board in Washington. • Within this Federal Reserve System existed 12 independent Regional banks and 25 branch offices. • The private banks that the Fed was to serve provided the Fed’s seed money, but they have virtually no control over central bank.

Evolution of the Fed • As the importance of a national monetary policy increased, power to conduct it was eventually concentrated in Washington. Because monetary actions can be unpopular, Congress has insulated the Fed from day-to-day political pressures by staggering the 14 year terms of the seven governors who serve on the Board of Governors. In addition, the Fed does not need appropriations from Congress to operate.

Evolution of the Fed • The 12 regional banks still exist, but they largely coordinate their actions through the board of governors.

Job of the Fed (the end) • The Fed’s job involves being alert for signs of recession or accelerating inflation and conducting monetary policy aimed at preventing either. • The twin goals of the Fed: price stability (i.e. curbing inflation) and full employment (i.e. promoting economic growth. • These twin goals, if/when met result in continued and sustainable economic prosperity. • Achieving these goals requires quite a balancing act.(next slide) • The Fed tries to make sure that dollars are plentiful enough so consumers and businesses can buy all the goods and services produced by the economy, even while investing in new facilities and technology to supply a growing population and provide a higher standard of living.

The Fed’s Balancing Act • There are times when money is difficult to obtain, loans become expensive and individuals and businesses don’t spend. • People lose jobs because such items as cars and airline tickets are not purchased or new buildings are not built. • If not enough money is available and loans are expensive and hard to obtain, people spend less. • Businesses then produce fewer goods and services than they are capable of producing. • They lay off workers and slow investments. • If production declines for many months, in what is called a recession, people can lose jobs. • At other times, lots of people have jobs, money seems easy to obtain and people and businesses spend freely. • Sometimes the good times get out of hand. • Too many dollars chase too few goods, and prices rise. • Loans can be obtained so easily that free spending becomes frivolous spending as investors pay too much for assets such as real estate and stocks. • If too much money is available, the major consequence is inflation—a general increase in prices. • If businesses are near the limit of their production capacity, any increase in the money supply means that consumers and businesses will spend more dollars on the same amount of goods and services, driving up their average cost. • Inflation strikes especially hard at those on fixed incomes or whose incomes do not rise as fast as inflation, as well as those who save and lend because their dollars may be worth less in the future.

Job of the Fed (the means) • The ultimate aim of Fed policy is to increase/decrease demand (the quantity of goods and services that consumers and businesses are willing and able to purchase). • The Fed can affect the environment in which economic decisions are made by manipulating the cash and credit conditions. • The Fed does not work directly on consumers or businesses, rather, it accomplishes its policy through banks by changing monetary policies.(next slide)

Monetary Policy • Monetary policy involves the manipulation of the amount of funds that banks have available to lend. • As the central decision-making body in charge of monetary policy, the Fed can take actions almost daily to help determine how much money is available, how easily it may be borrowed, and how costly it will be. • This in turn affects how many people will have a job, whether prices will be stable, and how many goods and services will be produced and sold. • With an eye on today and tomorrow, the Fed regulates the supply of credit and money. • In short, the Fed has the authority to change the level of bank reserves in a way it thinks will provide the amount of money and credit that will lead to full employment, stable prices, and economic growth.

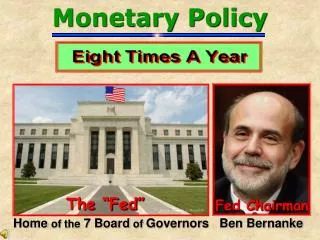

FOMC: The vehicle of the Fed’s monetary policies • The Federal Open Market Committee (FOMC) • A twelve member group consisting of the 7 governors who serve on the board and the President of the Federal Reserve bank of New York (all permanent members) as well as the Presidents of 3 other Federal Reserve banks who serve staggered terms that meets 8 times annually to review the economy and devise monetary policy. • This monetary policy is carried out by the Federal Reserve Bank of New York. • 1978: the FOMC was ordered by Congress to conduct policy to achieve twin goals: price stability and full employment.

The three tools of monetary policy • The discount rate(See subsequent slide) • Reserve Requirements (See subsequent slide) • Open Market Operations (See subsequent slide)

Discount Rate • The interest rate that the Fed charges to banks that need to borrow from the Fed to meet their reserve requirements. • Banks borrow from the Fed at the so-called “discount window”. • Decades ago, this was a key tool of monetary policy. • By changing the rate it charges at its “discount window,” for these loans, the Fed can encourage or discourage lending. • The discount rate is a passive tool. • For it to work, banks must come to the Fed to borrow. • For about 25 years, healthy banks have virtually ceased borrowing at the discount window, so the Fed cannot affect lending much by raising or lowering the discount rate.

Reserve Requirment • A percentage of checking deposits commercial banks and other deposit-taking institutions (e.g. savings and loan associations) are required by the Fed to keep on “reserve” (out of circulation) as cash in their vaults or as deposits in special “reserve balance” Fed accounts that resemble standard checking accounts. • These “reserves” must be non-interest bearing accounts—otherwise, banks might be encouraged to enlarge deposits since the money would be accruing interest. • The amount of money the banking system can create from a deposit ultimately is limited by the reserve requirement. • A bank cannot lend these required reserves. • The Fed can induce banks to lend more or less by changing the reserve requirements. • At most large banks today, the reserve requirement is ten percent. • Because banks earn no interest on reserve deposits, they prefer to keep them close to the required minimum. • Those holding more than is required lend the excess (usually overnight) to banks that are short of reserves and otherwise would pay a sizable penalty to the Fed. • The interest rate paid by a bank to borrow excess reserves from another bank is called the federal funds rate. • The federal funds rate is determined by supply and demand. • The Fed seldom changes reserve requirements to affect monetary policy because frequent changes in reserve requirements would be disruptive to banks and would be likely to change reserves in far bigger increments than the Fed usually seeks.

Open Market Operations • Currently, the monetary policy tool carried out almost exclusively by the Fed; it involves buying and selling government securities from private sources. • The New York Federal Reserve Bank is the main actor. • Securities that the New York Federal Reserve Bank buys and sells are basically IOU’s issued by the federal government for various periods of time as Treasury bills, notes, and bonds. • These transactions occur in so-called government securities markets. • The New York Fed open market desk does business with securities firms, called dealers, which are in business to trade Treasury securities for customers and themselves. • About 30 of these “dealers” are designated by the Fed as “primary” dealers and those are the firms with which the Fed buys and sells securities.

“Tightening” monetary policy • If/when FOMC members determine that demand for goods and services is increasing faster than businesses can supply them, they tighten monetary policyto fight inflation (next slide).

Tightening monetary policy • FOMC reduces the funds available to banks for loans and raises interest rates in hopes of discouraging the willingness of businesses and consumers from borrowing and buying. • The Discount Rate: • If, for example, the economy heats up, The Fed can decide to cool off the national economy by raising the discount rate. The “discount window” at which banks borrow from the Fed, is narrowed, banks generate less loans at higher rates because it is more costly for them to borrow from the Fed, and less available money lowers business investment, employment, consumer spending, and borrowing. • The Reserve Requirement: • If, for example, the economy heats up, the Fed can decide to cool off the national economy by increasing the reserve requirement ratio. This action would mean less money is available for banks to lend and more money would be kept out of circulation in “reserves”. The demand for a smaller amount of available money raises interest rates for consumers and businesses and would result in a decline in employment, salaries, prices, and business spending. • Example: If the Fed raises the requirement from ten percent to eleven percent, banks would have one percent less of their checking deposits available to lend. The higher the requirement, the less money can be created by a bank because it requires the bank to set aside a larger part of accepted deposits leaving less available for relending.

“Easing” Monetary Policy • If/when businesses aren’t selling as many goods and services as they can produce and fewer people have jobs than want them, or if the Fed thinks that the economy is headed in that direction, it eases monetary policy. (next slide)

The FOMC lowers interest rates by increasing the funds that banks can lend, hoping to encourage businesses and consumers to buy more. • Discount Rate: • If, for example, the economy is sluggish, The Fed can decide to stimulate the national economy by lowering the discount rate. The “discount window” at which banks borrow from the Fed, is widened, banks generate more loans at lower rates because it is less costly for them to borrow from the Fed, and more available money raises business investment, employment, consumer spending, and borrowing. • Reserve Requirement: • If, for example, the economy is sluggish, the Fed can decide to stimulate the national economy by decreasing the reserve requirement ratio. This action would mean more money is available for banks to lend and less money would be kept out of circulation in “reserves”. The demand for a larger amount of available money lowers interest rates for consumers and businesses and would result in an increase in employment, salaries, prices, and business spending. • Example: If the Fed lowers the requirement, banks would have a higher percent of their checking deposits available to lend. The lower the requirement, the more money can be created by a bank because it requires the bank to set aside a smaller part of accepted deposits leaving more available for relending. In short, if the requirement is lowered, funds would be freed.

Limits of the Fed • Whereas the Fed has more control over the interest rates of short-term loans, it has much less control over the interest rates of long-term loans such as home mortgages. • The Fed cannot make people spend or borrow more than they want to, and it cannot force banks and other lenders to provide loans. Moreover, the Fed cannot control what particular goods and services consumers want to buy and what investments businesses are willing to make. • Although the Fed can affect the environment in which economic decisions are made, it cannot force anyone to respond. It can increase the money supply, but people do not have to spend more. It can make credit more expensive (i.e. raise interest rates), but people still might spend money faster and pay the higher interest rates.

Limits of the FED • Monetary policy does not address important issues such as growing income inequality. • The Fed does not print money