Download

1 / 35

440 likes | 884 Vues

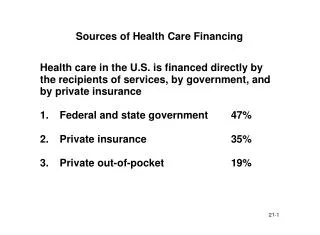

Health Care Financing. SANJAY OAK VICE CHANCELLOR PDDYPV. HEALTH CARE FINANCING. Definition of health care financing. Health care financing includes:- mobilization of funds for health care allocation of funds to the regions and population groups and for specific types of health care

E N D

Health Care Financing SANJAY OAK VICE CHANCELLOR PDDYPV HEALTH CARE FINANCING

Definition of health care financing Health care financing includes:- • mobilization of funds for health care • allocation of funds to the regions and population groups and for specific types of health care • mechanisms for paying health care

Overview • Importance and rationale for the focus on health financing • Definitions for health care financing • Different mechanisms of financing • Community based financing • Health financing in India

Points To Ponder • Changing Demographics • Rising Affordability & Expectations • Increasing Lifestyle Related Diseases • Health Insurance • Medical Tourism • Chanigng Trends in Research & Pharma • Regulatory Authorities.

Opportunities & Growth Strategies • The Unmet Need • Opportunities • Growth Strategies • Building Functional Efficiencies • Revenue Drivers • Risk Factors & Mitigation.

Indian health care industry is valued at USD 40 Billion in 2011 and is expected to grow at 24.11% p.a. till 2020. • Private equity and Chain group of Hospitals on the rise. • India spends 4.2% of GDP on health, global average 8.3%. • Private equity is expected to rise to 80>3% by 2025.

RISING AFFORDIBILITY GDP PER CAPITA $729…..2005 $1389….2010 $2226….2015 INCREASING WEALTH INCREASING AWARENESS INCREASING EXPECTATIONS.

PRIVATE SECTOR Concentration in Tier I Tertiary Care Facilities Primay Care Dis interest Inequitable distribution

POPULATION DEMOGRAPHICS Population above the age Of 60 is likely to double From 96.4 million in 2010 To 192.7 million in 2030.

LIFESTYLE DISEASES • Additional Demand For • Specialized treatment and hospitals. • Geriatric • Diabetic • Day Care CT units • Short Stay Hospitals • Hotel WITHIN Hospital.

CARDIAC CARE • Paediatric Cardiac • Preventive • Rehabilitation • Ayurveda

REGULATORY FACTORS Benefit of Section 10 ( 23G) of IT Act. PPP models Benefit of 80-IB for rural areas investment Life saving equipment custom duty 25%- 5% Import dutyon med. Equipment 7.5% Incentives for medical tourismDrugs & Cosmetics act. BMW Disposal rules 1998 Clinical Establsihment Bill 2010 NABH DGCI FDI in hhospitals upto 100%.

Gross Health Insu. Premiums have increased from 733.9 million $ to 2095 $ in 2011.

MEDICAL TOURISM Quality At Affordable Cost. $350 million in 2010 to $ 2.2 Billion in 2015.

MARKET TRENDS Higher profitability in Tier II & III cities Operating costs are 30% lower Operating profitability in 1sr or 2nd year. Disease profiles changing from infectious to lifestyle related. Operation & management contracts Telemedicine applications Expat doctors settling Holistic appraoch.

Telemedicine • Specialty clinics • Tier II & III cities.

Mechanisms of Health Financing • general revenue or earmarked taxes • social insurance contributions • private insurance premiums • community financing • direct out of pocket payments

Direct out of pocket • made by patients to private providers at the time a service is rendered • user fees refer to fees the patients have to pay to public hospitals, clinics, and health posts not to private sector providers. • proponents of user fees believe that the fee can increase revenue to improve the quality of public health services and expand coverage • major objection raised against user fees had been on equity grounds

Changing government role in health care • Health is considered a public good • Government needs to actively participate to avoid market failures

Donations Fines Contributory Mutual Funds Sponsorships University Chairs.

Pharma Sector Regulations Research Review University-Industry Projects Relook at Legislations

IT APPLICATIONS SOFTWARE DEVELOPMENT PACS & PAPERLESS RAF HEALTH CARD.

Rashtryia Bima Yojana Geriatric Mental Women & Child

Special Economic Zones For Health Care Tax Concession schemes for health iinvesting firms Health coverage For Middle Class Families Tax Payers For City HEALTH CARE FINANCING

Health service financing source • External sources refer to the external aid which comes through bilateral aid program or international non governmental organizations

Private insurance • consumers voluntarily choose to purchase an insurance package that best matches their preference. • offered on individual and group basis. Under individual insurance the premium is based on that individuals risk characteristics. • Under group insurance, the premium is calculated on a group basis. risk is pooled across age, gender and health status.

Community based financing Refers to schemes are based on three principles: community cooperation, local self reliance and pre payment Factors for success of community financing • Technical strength and institutional capacity of the local group • Financial control as part of the broader strategy in local management and control of health care services • Support received from outside organizations and individuals • Links with other local organizations • Diversity of funding • Responding to other (non health) development needs of the community • Ability to adapt to a changing environment

Employer based schemes • Offered both by public and private sector companies through their own employer managed facilities • Mode lump sum payments, reimbursements of employee’s health expenditure or covering them under the group health insurance policy with one of the subsidiaries of GIC. • Workers buy health insurance through their employers taking insurance in lieu of wages

Voluntary health insurance schemes • Are for individuals and corporations • Available mainly through the General Insurance Corporation (GIC) of India and its four subsidiaries- a government owned monopoly. • financed from household and corporate funds • GIC offers MEDICLAIM policy for groups and individuals and the JAN Arogya Bima scheme to individuals and families, mainly to cover poor people. • With Insurance Regulatory and Development Act 1999 and the liberalization of insurance more private voluntary health schemes are expected to be introduced soon.

Challenges with insurance • India linking health insurance with employment is difficult because most people are self employed, have agricultural work, or do not have a formal employer or steady employment. • Many of the poor are excluded from access to high quality health care and health insurance because of inability to pay, lack of knowledge, or other factors, related to geography or discrimination • Too much of cream skimming too in India i.e.selection of less risky groups by insurance companies

Conclusion • Role of health economists be recognized • Health financing cannot be dealt separately as it has got to do with good governance, economic growth, education • Social inclusion and financial protection seems to be provided through community based financing