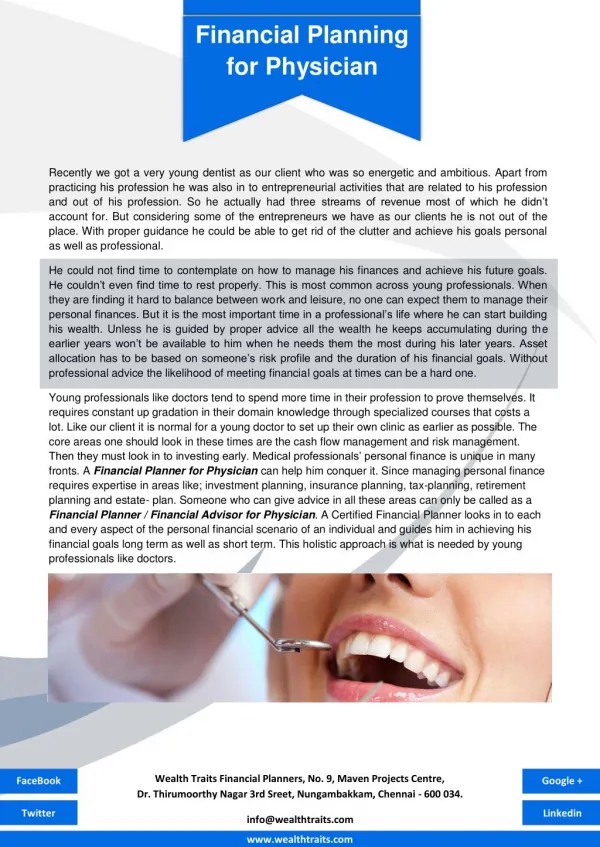

Financial Planning For Residents

550 likes | 787 Vues

Financial Planning For Residents. GOALS. GOALS. GOALS. GOALS. GOALS?. Stuck in ED at age 80. GOALS?. GOALS?. Financial Planning. Insure Against “What If” • Insurance Protection • Emergency Cash Fund • Debt Management • Retirement Planning • Estate Planning. Absolutely

Financial Planning For Residents

E N D

Presentation Transcript

GOALS? • Stuck in ED at age 80

Insure Against “What If” • Insurance Protection • Emergency Cash Fund • Debt Management • Retirement Planning • Estate Planning Absolutely Necessary (Survival) Life Plan Absolutely Necessary

Debt Management Get in the Habit of PAYING YOURSELF FIRST!!!

Budgeting “Income minus Expenses”

Budgeting Goals • Must Define and Articulate *Student loan repayment *Retirement planning *Education funding for kids *Cash savings *Buying home *Eliminating BAD debt *Buying into group *Fancy Car and Toys

Assign Value/Priorities • Importance to you/family • Timeline • Intelligent repayment of debt • Fear of debt • Need for toys *Beware of Golden Handcuffs • Financial Independence • Avoiding Frustration

Debt Management • Which should you pay off first? *$100,000 Student loan at 3% *$5,000 Credit Card at 18% *$250,000 Mortgage at 6% fixed

Fear of Debt • Not all debt is bad • Realize that on average the stock market makes 8-12% a year historically • Realize that as a resident you don’t make much *Compare you student loan debt in relation to 10 of working as a physician *Defer you student loans *Stretch out you repayment periods *Pay yourself first!!

Emergency Cash Fund • Experts say 3-6 months of expenses • This depends on your comfort zone/situation • Do you have short term disability? • Long term disability doesn’t kick in for 3-9 months • Cash keeps you in control

Emergency Cash Fund • Make use of a money market account *Higher yield and easily liquid *Some are tax free • Should develop systematic and disciplined method to build cash reserves *Monthly budgeted draft • Goal is to try and avoid bad debt (credit cards)

Credit Cards • Try to get rid of this debt first *Worst kind of debt *Transfer money lowest credit cards *Goal is to ALWAYS pay off at end of month *Only use cards that give you something back with no yearly fees • Free Cash back cards are out there • Fund Retirement First?!?!?!

Retirement Can EM Residents Save For Retirement? Yes!

Age When Investments Begin 25 $158 35 $442 45 $1,316 55 $4,882 Monthly Investments Required to Reach Goal Why Invest Now? Here are the monthly investments required at different ages to accumulate $1,000,000 by age 65, assuming a 10%* compounded rate of return.

$500,000 $400,000 $299,599 $300,000 $200,000 $174,494 $100,627 $100,000 $57,435 $0 6% 8% 10% 12% Why Invest Now? Illustration of the growth of an assumed $10,000 investment compounded annually over a 30-year period at differing rates of return.*

Save, Save, Save • Can you put aside $333+ a month? *Moonlighting? *Not paying school loans *Not overpaying credit cards? *Not drinking Starbucks daily *Limiting expenses

Roth IRA (10% each Year) Yr 1 $4000 $400 $4400 Yr 2 $4000 $840 $9240 Yr 3 $4000 $1324 $14564 Yr 4 $4000 $1856 $20420 Graduate No more contributions Break even in ~62 months Keeps growing tax free Credit Card (20% each Yr) Yr 1 $-4000 $-800 $-4800 Yr 2 $-4000 $-1760 $-10560 Yr 3 $-4000 $-2912 $-17472 Yr 4 $-4000 $-4294 $-25766 Graduate Payoff $1000 a month Done 33 month ~$33262 total payment Credit Cards

Where to Invest? • ROTH IRA *Up to $4000/year -- After Taxes • 401k/403b *Up to $15,000/year --Before Taxes • SEP IRA *20% of moonlighting income up to $44,000 *Tax deductible

DEPOSIT ACCUMULATION DISTRIBUTION 1 401(k)s & 403(b)s TRADITIONAL IRAs Tax Deductible (Before Tax $’s) Tax Deferred (Funds not Available) Taxable (Income & Estate) SEP & SIMPLE IRAs KEOGH, PSP & MPP ESOPs IRS penalties for retirement withdrawals prior to age 59 ½ ! 2 LIFE INSURANCE Tax Deferred (Funds Available with Municipal Bonds) Can be Tax Free or Taxable… You Choose ANNUITIES Not Deductible (After Tax $’s) MUNICIPAL BONDS ROTH IRAs 529/COVERDALE IRAs Possible IRS penalties for withdrawals prior to age 59 ½! Partially Tax Deferred and Partially Tax Free 3 CDs, SAVINGS, Partially Taxable And Partially Tax Free Not Deductible (After Tax $’s) MUTUAL FUNDS STOCKS, BONDS PARTNERSHIPS Three Phases of Investment

700,000 Assumptions: Growth if tax-deferred $100,000 investment $672,750 600,000 10% net annual compounded rate of return* 39.6% tax bracket Tax- deferred 500,000 after taxes $445,941 400,000 300,000 $323,143 Growth if taxable $303,467 200,000 100,000 5 yrs 10 yrs 15 yrs 20 yrs Years The Value of Tax Deferred *Hypothetical rate of return for illustrative purposes only. Return is net of expense.

Goal is to Understand and Minimize Income Taxes 7% 8% 9% Tax Deferred EQUALS 11.66% 13.33% 15% Taxable

ROTH IRA • Should be your first place to put money!! *Money is tax deferred and Tax Free in Distribution *Can only put money into Roth as a resident • Cannot fund if make more that $110,000 single or $160,000 jointly *Can pull out for down payments on first home, higher education, some rare other reasons (don’t recommend). *Pull out at age 59 ½

Louisiana Deferred Compensation Plan (457b) • You should all be in this NOW!!! • You can take the 7.5% you pay to Social Security and put this into your own portfolio • All Pre-Tax Money • Max of $15,000 a year • Can offset contribution with moonlighting pay or recent raise • Can take it with you to other job or financial institution • No Matching

401k/403b/457 • For Future Job *Pretax money placed into investment *All growth Tax Deferred *Some Jobs Match (always at least put match percentage or you are giving away free money) *Hope that your tax bracket will be lower when you are older *Distribution at age 59 ½ *Can take it with you to other job or financial institution

Why 401k/403b/457? • No Investment *Salary $3000/month *25% tax bracket is $750/month *Take home pay $2250/month • Investing $500/month *Salary $3000/month - $500/month contribution *New Salary $2500/month *25% tax bracket is $625/month *Take Home pay $1875/month *$375 less take home but $500 into retirement ($125 less taxes paid)

SEP IRA • In most cases, third option for resident • Can only invest if Moonlighting (Independent Contractor—Form 1099) • Most of times, fund if Roth IRA and matched 401k/403b fully funded • Then 401k/403b/SEP IRA act the same just depends on what kind of job you have

Insurance • Medical • Disability • Life • Other *Auto *Home/Rental *Umbrella

Medical Insurance • COBRA *Do not let your insurance lapse (especially if you or your family have pre-existing conditions) *GME must provide *Usually have 30-60 days to pay premiums *Important to know when exactly your contract begins

Disability Insurance Most Important Thing to do BEFORE Residency Ends!!!

Disability Insurance Everything you own, plan to own, or plan to pay off, depends on your ability to earn an income.

Disability Insurance • GME provides *Usually either 50-60-66 2/3-80% of your current paycheck *$3000/month pretax—your benefit would be $1800 *This money is taxable *Payable to age 65 • WARNING: Not all plans are created equally!!

Disability Insurance • There are special Disability Insurance plans that are only available for residents!!! • Benefits *Usually starts at $4000/month benefit (more than you make now) *Can get a rider that allows you to increase to $10,000/month benefit *Can take it with you after you graduate *Can stack on top of your job’s current disability plan

Disability Insurance • Must have these Characteristic *Cannot be dropped or amended by the insurer *The premiums cannot be increased *Protects your right to work in your own medical specialty *Ability to control benefits through Guaranteed Purchase options (Rider to increase amount) *Cost of living adjustments features *Consider catastrophic or long term care provisions • $181-418 a month depending on coverage

Disability Insurance • Carriers *Guardian *MetLife *Standard *Union Central *Principal Financial

Life Insurance • Why do you need it now? *The younger you are, the cheaper it is *The healthier you are, the cheaper it is *Lock it in now at the youngest and healthiest you will ever be *Prepares you for future need at today’s prices • Married or kids later in life

Life Insurance • 2 Types of Life Insurance *Term Life Insurance • Limited Term (10, 20, 30 years) • Cheap (32 year old--~$450/yr for $1,000,000 coverage) • Good to cover for early unexpected death *Permanent Life Insurance • Lasts for life • More expensive • Many types: Whole Life, Universal Life, Variable Life • Good as a method of saving more money

Life Insurance • Variable Life Insurance *You can add to the cash value *Grows Tax Deferred in an account inside your life insurance *You can pull cash out (that you put in) at any time and use it but your relatives won’t get that *You die—Family gets your death benefit and whatever you put in—Jackpot *You don’t die—You can pull it out as you need it like a loan (emergency cash fund?)

Other Insurance • Auto Insurance *Don’t forget to cover appropriately as net worth goes up, (can come after salary if not covered) • Homeowner Insurance *Don’t forget to cover for appropriate cost of rebuilding home • Umbrella Insurance *Extra insurance that protect for catastrophe attached around car and home

Estate Planning Decisions are easier to make while you are ALIVE!

Estate Planning • Basics *Will *Living Will *Durable Power of Attorney *Healthcare Power of Attorney • Advanced *Trusts *Inheritance planning *Gifts

Financial Planner/Team Do you really know what you are doing?

Financial Planner/Team • If yes, Proceed • If no, Consider hiring someone you TRUST! *Remember that poor investments or poor allocation could cost you $1000s-$10,000s. Especially as you get older *Do you have the time to manage this? *Do you know all the legal loopholes *Is it worth your time? *Can you work one shift a year for the comfort of mind