Download

1 / 8

90 likes | 218 Vues

The Western Canada beef industry faces unique challenges and opportunities within its value chain. Key players include ranchers, feedlots, and processors such as Cargill and IBP, with investments ranging from $200 to $3,000 per head. The current system processes more than 2.7 million animals annually, addressing a surplus of production capacity. Innovations focus on rancher ownership, quality control, and niche marketing, reducing risks associated with live animal markets. A shift towards transparent, market-based pricing is also essential for enhancing profitability and sustainability in the sector. ###

E N D

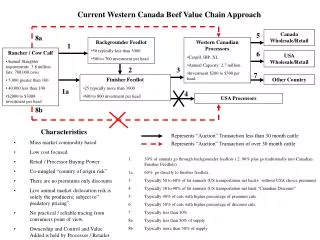

Current Western Canada Beef Value Chain Approach 5 Canada Wholesale/Retail 8a • Backgrounder Feedlot • 50 typically less than 3000 • 500 to 700 investment per head • Western Canadian Processors • Cargill, IBP, XL • Annual Capacity: 2.7 million • Investment $200 to $300 per head 1 • Rancher / Cow Calf • Annual Slaughter requirements 3.8 million fats; 700,000 cows • 5,000 greater than 100 • 40,000 less than 100 • $2000 to $3000 investment per head 6 USA Wholesale/Retail 2 3 7 • Finisher Feedlot • 25 typically more than 3000 • 600 to 800 investment per head Other Country 1a 4 USA Processors 8b • Characteristics • Mass market commodity based • Low cost focused. • Retail / Processor Buying Power • Co-mingled “country of origin risk” • There are no premiums only discounts • Live animal market dislocation risk is solely the producers; subject to” predatory pricing”. • No practical / reliable tracing from consumers point of view. • Ownership and Control and Value Added is held by Processor / Retailer Represents “Auction” Transaction less than 30 month cattle Represents “Auction” Transaction of over 30 month cattle • 30% of animals go through backgrounder feedlots ( 2. 90% plus go traditionally into Canadian Finisher Feedlots) • 1a. 60% go directly to finisher feedlots. • Typically 50 to 60% of fat animals (US transportation net back+ without USA choice premium) • Typically 30 to 40% of fat animals (US transportation net back “Canadian Discount” • Typically 40% of cuts with higher percentage of premium cuts. • Typically 50% of cuts with higher percentage of discount cuts. • Typically less than 10% • 8a Typically less than 50% of supply • 8b Typically more than 50% of supply

Next Generation Western Canada Beef Value Chain Approach • Rancher’s Owners • Now more than 30 • Ultimately the number that elect to own • Over time, will reflect the number that combine to cover the vast majority of the capacity of the plant. 1 • Rancher’s Feedlot • More than 1/2 of the plant capacity owned • Rest of Feedlot capacity organized by contract • Rancher’s Processing • 250,000 capacity (easily doubled and can grow further with market) • Flexible (cow / bull & fats) • Investment 200 to 300 per head Rancher’s Brand 4 White Label 3 2 • Characteristics • Rancher’s supply and processing separate from co-mingled mass market • Differenced / Niche market based • Value add based. • Fully tracked “vertical” quality control • Minimizes buyer discounts • Creates opportunity to obtain premiums. • Producers have opportunity to eliminate live animal market dislocation risk; accept the wholesale meat market risk. • Producers no longer subject to” predatory pricing by processors”. • Ownership and Control and Value Added is held by Rancher’s / Retailer Represents “Market Value Net-back Pricing” • Rancher’s Brands; BSE free by full testing; Hormone free.. others; Marketed to Canada; USA; Europe; Asia • Rancher’s will custom develop and process for any other compatible brand. • Owners can elect a “quality adjusted market based price” or can elect to pay custom processing fee and arrange market for the meat. • Owners can elect to retain ownership of animals through feedlot and elect options under 3 or can sell to Rancher’s for “quality adjusted market based price” • Owners are hedged from discount live animal markets either through profits of Rancher’s or Wholesale meat market less custom processing and custom feedlot cost approach. • All interested parties (including governments) get market transparency. • Rancher’s ownership units will be listed and trade. Creates Private Sector Capital markets as source for growth capital; Creates competitive tension with Legacy Processors.

Current Situation • Western Canadian Beef Industry produces 30 % more live animals than can be processed in Canada. • Investment in production of livestock is 20 to 30 times as much capital as is required in the processing industry. • International borders are closed to live animal movement; cattle and sheep. • Over 80% of the processing capacity in Canada is in two American processing Plants in Southern Alberta. • The international borders are open to meat with particular specifications. • No other country in the world has a animal production industry that depends on this amount of international trade in live animals. • Regulators, Trade agencies, Health Agencies are becoming more active as science moves forward and new tests are developed. It is not just BSE.

Depending on International Trade of Live Animals Makes No Sense • Health issues with live animals are infinitely more complex than with meat. • Live animals have limited shelf life and have every day carrying cost. • Live animals are a potential health risk to other live animals. • The cost of processing is minor relative to the cost of producing the animal. • The cost of transport of meat is much less than the cost of transport of live animals. • Why export the employment opportunities associated with processing?

Why Did the Industry Evolve This Way? • Western Canada is amongst the best locations to raise and fatten cattle. • Environment is good, superior genetics, land that is less useful for other purposes, abundant cereal grains for feed. (The meat is superior meat). • Processing was driven by economies of scale; low cost - not value add. • Main economy of scale was derived from the value of the non-meat part of the carcass. • Small processors could not make up on the revenue side for the loss on the non-meat side. • Now the main processors have buying muscle as well. • Even though producers have much more invested than processors, they are many individuals. • The producing industry had enough efficiency advantages to thrive even though it had access to a much inferior processing marketplace from a competition point of view. • The discipline was their ability to export live animals to USA based plants.

Characteristics of a Lasting Solution • Increase Processing Capacity so Domestic Processing is Able to Handle Domestic Production. • Create the “Next Generation” Value Add Value Chain. • Create Canada Based competition in processing to create a viable marketplace. • Create value added specialty brands directly targeting specific markets whether in USA, Asia or Europe. • Get away from the lose-all risk of the “Canadian Brand”. • Create an environment that gives producers the option of investing in value added and marketing as opposed to being forced to accept the outcome of a non-competitive cost based marketplace. • If producers had the option to create viable alternatives to the status quo then a number would evolve and the Government would no longer be exposed to risk that the trade in live animals is disrupted by other governments. A portion of any government funding for BSE related hardship should be targeted at initiatives that Canadians control and solve the market problem.

Rancher’s Beef Ltd • Who is involved? • Sunterra Farms is the founder. Successful family-owned farming enterprise that has value added processing and specialty marketing in pork, veal and lamb. (Markets to Canada, Japan, USA, Mexico). • More than 50 other producers have committed to purchase ownership. (Alberta, BC, Saskatchewan). • Over $25 million of assets and over $15 million of cash committed. • Ownership is open to anyone that wants to invest. (Subscribers continue to grow). • What is Rancher’s Business Objective? • State of the art processing, combined with feedlot operations with ownership linkage to cow / calf and backgrounder. • Will develop and market specialty branded beef products by organizing the supply chain to deliver a differentiated superior value to its customers. • Business is organized so that producers are in control and own the profit that is generated by the value chain to the branded meat market. • Customer driven; profit based. • It is the first real example of the “Next Generation Value Chain” organized for the future as opposed to the past.

What Does Government Need to Do? • To date, the Government supported initiatives have been supporting the status quo. • Unless the domestic supply / processing imbalance and the lack of competition and diversity in the processing sector is addressed, the benefactor of government support programs will be large existing processors. (As has happened to date). • Governments need to financially support the transition to a new domestic market-place which gives producers the option of investing in value added and creates the appropriate domestic competitive tension with the large commodity based processors. • Rancher’s is an example: • Federal government should agree to match provincial government funding for such initiatives. • In Rancher’s case, we are proposing that if the Private Sector raises $25 million of equity, that the Province of Alberta and the Government provide funding of $10 million. • Governments can support a number of these type of initiatives. (Three Rancher’s sized initiatives would bring domestic processing in line with domestic production).