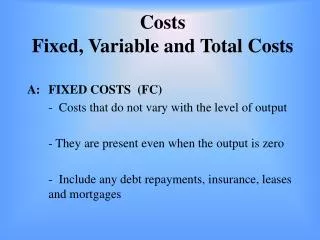

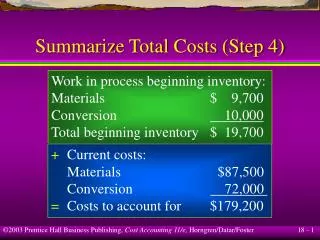

Summarize Total Costs (Step 4)

Summarize Total Costs (Step 4). Work in process beginning inventory: Materials $ 9,700 Conversion 10,000 Total beginning inventory $ 19,700. Current costs: Materials $87,500 Conversion 72,000

Summarize Total Costs (Step 4)

E N D

Presentation Transcript

Summarize Total Costs (Step 4) Work in process beginning inventory: Materials $ 9,700 Conversion 10,000 Total beginning inventory $ 19,700 • Current costs: • Materials $87,500 • Conversion 72,000 • Costs to account for $179,200

Assign Total Costs (Step 5) Good units completed and transferred out (31,000 units): Costs before adding normal spoilage: 31,000 × ($2.70 + $2.50) $161,200 Normal spoilage: 620 × ($2.70 + $2.50) 3,224 Total $164,424

Assign Total Costs (Step 5) Abnormal spoilage: 380 × ($2.70 + $2.50) $ 1,976 Work in process, ending (4,000 units): Direct materials (4,000 × $2.70) $10,800 Conversion (800 × $2.50) 2,000 Total $12,800

Assign Total Costs (Step 5) Costs of units completed and transferred out (including normal spoilage) $164,424 Cost of abnormal spoilage 1,976 Costs in ending inventory 12,800 Total costs accounted for $179,200 The $1,976 cost of abnormal spoilage is assigned to the Loss from Abnormal Spoilage account.

Learning Objective 4 Account for spoilage in process costing using the first-in, first-out (FIFO) method.

Physical Units (Step 1) Work in process, beginning (November 1): 100% material, 60% conversion costs 1,000 Started during November 35,000 36,000 Good units completed and transferred out: From beginning inventory 1,000 Started and completed 30,000 31,000

Physical Units (Step 1) Work in process, ending inventory: 100% material, 20% conversion costs 4,000 Normal spoilage 620 Abnormal spoilage 380

Compute EquivalentUnits (Step 2) MaterialsConversion Good units completed and transferred out: From beginning inventory 0 400 Started and completed 30,000 30,000 Normal spoilage 620 620 Abnormal spoilage 380 380 Ending inventory 4,000 800 Equivalent units 35,000 32,200

Compute EquivalentUnit Costs (Step 3) MaterialsConversion Current costs $87,500 $72,000 Divided by equivalent units 35,000 32,200 Cost per unit $2.50 $2.236* *$2.236 (rounded)

Summarize Total Costs (Step 4) Work in process beginning inventory: Materials $ 9,700 Conversion 10,000 Total beginning inventory $ 19,700 • Current costs: • Materials $ 87,500 • Conversion 72,000 • Costs to account for: $179,200

Assign Total Costs (Step 5) Good units completed and transferred out: From beginning inventory: Work in process $ 19,700.00 Conversion costs added in current period (400 × $2.236) 894.40 Total $ 20,594.40 Started and completed: 30,000 × ($2.50 + $2.236) $142,080.00

Assign Total Costs (Step 5) Costs before adding normal spoilage: ($20,594.40 + $142,080.00) $162,674.40 Normal spoilage: 620 × ($2.50 + $2.236) 2,936.32 Total $165,610.72

Assign Total Costs (Step 5) Abnormal spoilage: 380 × ($2.50 + $2.236) $1,799.68 Work in process, ending (4,000 units): Direct materials (4,000 × $2.50) $10,000 Conversion (800 × $2.236) 1,789 Total $11,789

Assign Total Costs (Step 5) Costs of units completed and transferred out (including normal spoilage) $165,610.72 Cost of abnormal spoilage 1,799.68 Costs in ending inventory 11,789.00 Total costs accounted for $179,200.00 The $1,799.68 costs of abnormal spoilage are assigned to the Loss from Abnormal Spoilage account.

Learning Objective 5 Account for spoilage in process costing using the standard-costing method.

Standard-Costing: Spoilage The standard-costing method makes calculating equivalent unit costs unnecessary and so simplifies process costing.

Journal Entries Assume that the completed units are transferred to Finished Goods. What are the journal entries? Finished Goods XXX Work in Process XXX To transfer good units completed in November

Journal Entries Loss from Abnormal Spoilage XXX Work in Process XXX To recognize abnormal spoilage detected in November