Download

1 / 31

310 likes | 349 Vues

VA Loans for Vets NMLS#184169<br>5050 North 40th Street, Ste 260<br>Phoenix, AZ 85018<br>602-908-5849<br><br>Jimmy Vercellino is one of the nationu2019s top VA Home Loan mortgage originators. A Marine veteran, he and his team work hard to help veterans take advantage of their VA loan benefit and become homeowners. From start to finish, they guide their clients through the process and make it as smooth and stress-free as possible. Visit the site at https://www.valoansforvets.com

E N D

Whether you’re applying for your first mortgage or your fifth, you must know your debt-to-income ratio.

It is one of the most important factors used to determine not only whether you can afford a new mortgage, but how much you can afford and at what interest rate.

Lenders are loaning you their money to buy or refinance a home. Your financial situation, income and debts you owe, are important to them.

They must determine if you already have too much debt to repay. It’s one of many ways they assess your ability to repay the loan you are asking for from them.

They want to know they’re making a wise financial investment.

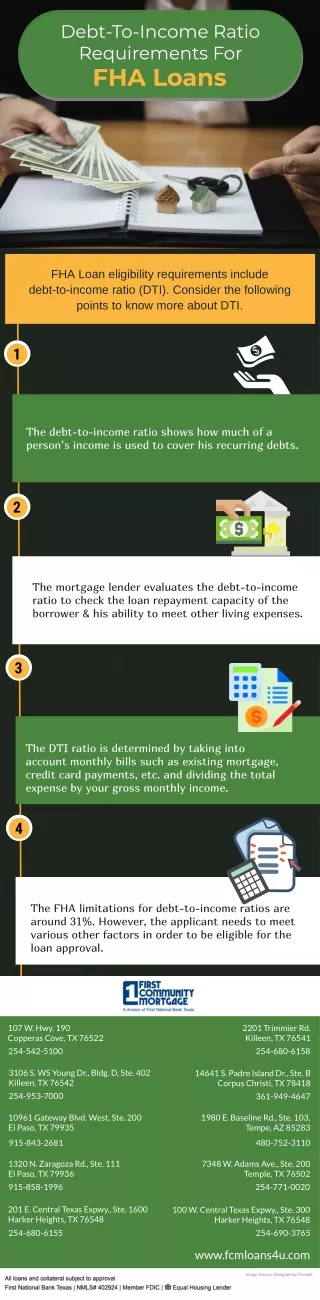

WHAT IS CONSIDERED DEBT?

There are many questions associated with calculating debt-to-income ratio. Not all your monthly expenses are considered debt.

But for this calculation, it’s important to know which ones are considered: ➢Mortgage payment ➢ Escrowed real estate and homeowners insurance

➢ Car notes ➢ Student loans ➢ Personal loans ➢ Credit card payments

➢ Time shares ➢ Alimony ➢ Child support ➢ Loans you co-signed

Things such as your car insurance, health insurance, utilities, and other bills of that nature are not included in the debt portion of your debt-to- income ratio.

HOW TO CALCULATE DEBT-TO-INCOME

The ideal ratio is at or below 36%. But it’s always best to keep your debts as low as possible.

The way to calculate this percentage is to add up all debts included in the list above. Then add up all sources of gross income.

Gross income is the amount of money you earn each month prior to the subtraction of taxes and other deductions from your paycheck.

This is important to note. If you use your net income for this calculation, you will get an incorrect analysis of your debt-to-income ratio.

Once you correctly determine these numbers, take your debt and divide it by your income. This is the percentage of your debt-to-income ratio.

For example, if you have $2,000 in monthly debt expenses and $10,000 in monthly gross income, your debt-to-income ratio is 20%. This is low, and it looks good to lenders.

When your debt-to-income ratio exceeds 36%, it’s not a good sign. Many lenders will refuse to work with you. Or they will require you to spend some time and money paying down your debts.

Paying off your mortgage or car loan might not be possible. But paying off any other loans in your name or credit card balances will work in your favor.

Your lender will advise you as to what you need to pay off.

It’s also important to remember your current mortgage is not going to be calculated in this ratio if you are applying for a new one.

The potential new mortgage you’re applying for is the one that’s calculated when you go through this process.

Speak to your lender about any questions you might have regarding your debt-to-income ratio.

Mortgage Originator Jimmy Vercellino, specializing in VA loans, helps veterans use their VA loan benefit to their greatest advantage.

First Choice Loan Services Inc., DBA FCLS in CA 959 South Coast Drive, #490Costa Mesa, CA 92626 Phone: 619-350-1951