Download

1 / 21

210 likes | 328 Vues

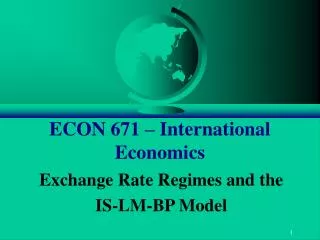

ECON 671 – International Economics. Exchange Rate Regimes and the IS-LM-BP Model. IS-LM-BP under a Fixed Exchange Rate Regime. Open Economy SR Equilibrium: IS-LM-BP Model. IS-LM-BP Model described by 3 equations (IS) Y = C (Y-T, W) + I(i) + G + NX(e, Y, Y ROW , W)

E N D

ECON 671 – International Economics Exchange Rate Regimes and the IS-LM-BP Model

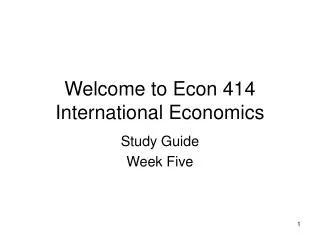

Open Economy SR Equilibrium:IS-LM-BP Model • IS-LM-BP Model described by 3 equations (IS)Y = C (Y-T, W) + I(i) + G + NX(e, Y, YROW, W) (LM)Ms/P= a(DR + IR)/P= f(Y, i, W, E(p)) (BP)BOP0 = NX(e, Y, YROW, W) + j(i, i*+ xa) • IS-LM-BP with Fixed Exchange Rate Regime: • Endogenous Variables: Y, i, M(BOP=DIR) • Exogenous Variables: G, T, DR, W, P, e • In a Fixed Exchange Rate Regime, adjustment to FX market equilibrium occurs through changes in Int’l Reserves, IR. • Changes in IR will shift LM Curve Only • No Changes in IS or BP Curves to changes in IR.

Reach equilibrium by changes in all 3 endog. variables: i, Y, e or M LM Curve - shifts with DM or DP BP Curve LM([DR+IR]/P) - shifts with De or DROW variables BP(e0, i*, Y*) i1 IS Curve - shifts with De, DG or DT IS(e0, G0, T0) Y1 IS-LM-BP Model Interest Rate Income, Output

Types of Fixed EXR Regimes • Traditional Fixed Exchange Rate Regime: • Gov’t sets a fixed level for the exchange rate. • Central bank intervenes in FX market to maintain EXR fix. • Requires Central bank to hold credible levl of Int’l Reserves. • Exchange Rate Bands: • Gov’t sets a “band” around a fixed level for exchange rate. • Central bank intervenes if EXR moves outside bands. • Requires Central bank to hold credible level of Int’l Reserves. • Currency Board: • Gov’t sets a fixed level for exchange rate. • Currency Board issues domestic currency only to extent it can be backed 100% by Int’l Reserves. • Currency Board conducts no independent monetary policy.

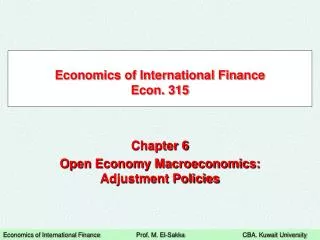

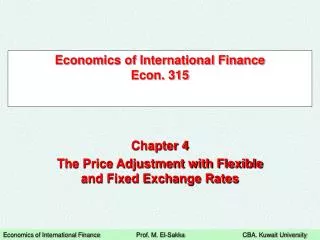

Fiscal Policy with Fixed EXR • Look at effects of increase in gov’t spending, G. • Direct Effect • Increase in G will shift IS Curve outwards. • No Direct effect on either BP or LM Curves. • New internal equilibrium where LM and new IS intersect. • Both Y and i increase at new intersection. This is not overall equilib.!! • What is status of BoP at this point? • Depends on capital mobility. • Indirect Effects (Automatic Adjustment to New Equilibrium) • If capital is relatively immobile • BOP < 0, Int’l Reserves fall as Central Bank tries to keep EXR fixed • This shifts the LM Curve backwards until IS-BP-LM all intersect. • If capital is relatively mobile • BOP > 0, Int’l Reserves rise as Central Bank tries to keep EXR fixed • This shifts the LM Curve outwards until IS-BP-LM all intersect.

1. Rise in Gov’t spending shifts IS Curve out 2. BOP surplus at B leads to increase in IR at fixed e. 3. Rise in IR, raises Ms, which shifts LM out to pt. C. 1. LM1 DG > 0 2. B i1 C IS(e0, G1, T0) Y1 Fiscal Policy under Fixed EXR Interest Rate LM0 BP(e0, i*, Y*) i0 A IS(e0, G0, T0) Y0 Income, Output

LM1 IS1 IS1 LM1 i1 Y1 Fiscal Policy & Capital Mobility Capital Completely Immobile Capital Perfectly Mobile i i BP0 IS0 LM0 LM0 IS0 BP0 i0 i* Y0 Y Y Y0

IS1 LM1 IS1 LM1 i1 i1 Y1 Y1 Fiscal Policy & Capital Mobility Capital Relatively Immobile Capital Relatively Mobile i i BP0 IS0 IS0 LM0 LM0 BP0 i0 i0 Y0 Y0 Y Y

Monetary Policy with Fixed EXR • Look at effects of decrease in money supply through lower DR. • Direct Effect • Decrease in Ms shift LM Curve inwards. • No Direct effect on either BP or IS Curves. • New internal equilibrium where new LM and IS Curves intersect. • Both Y and i increase at new intersection. This is not overall equilib.!! • BoP at this point is always in surplus regardless of capital mobility. • Indirect Effects (Automatic Adjustment to New Equilibrium) • BoP surplus means that IR will increase, results in increase in Ms. • This shifts the LM Curve outwards until get back to original equilibrium. • Monetary policy is ineffective under Fixed Exchange rate Regime • Independent monetary policy is not possible as Central Bank must intervene to keep EXR at set level.

LM1 LM1 DDR<0 DDR<0 DIR>0 DIR>0 Monetary Policy & Capital Mobility Capital Completely Immobile Capital Perfectly Mobile i i BP0 LM0 LM0 BP0 i1 = i0 i* IS0 IS0 Y0 Y0 = Y1 Y Y

LM1 LM1 DDR<0 DDR<0 DIR>0 DIR>0 i1 = i1 = = Y1 = Y1 Monetary Policy & Capital Mobility Capital Relatively Immobile Capital Relatively Mobile BP0 i i LM0 LM0 BP0 i0 i0 IS0 IS0 Y0 Y0 Y Y

EXR Policy with Fixed EXR • Look at effects of devaluation in domestic currency, (rise in e). • Direct Effects • Depreciation raises NX which shifts IS and BP Curves outwards. • No Direct effect on LM Curve. • New internal equilibrium where LM and new IS Curves intersect. • Both Y and i increase at new intersection. This is not overall equilib.!! • BoP at this point is always in surplus regardless of capital mobility. • Indirect Effects (Automatic Adjustment to New Equilibrium) • BoP surplus means that IR will increase, results in increase in Ms. • This shifts the LM Curve outwards until get to IS-BP-LM equilibrium. • Exchange Rate policy is effective. • A Devaluation of the Exchange Rate is expected to increase the level of GDP in the country, i.e. its an expansionary policy.

1. Depreciation in EXR shifts IS Curve out. 2. Depreciation in EXR shifts BP Curve out. 3. BOP surplus at B leads to increase in IR at fixed e. 4. Rise in IR, raises Ms, which shifts LM out to pt. C. LM1 1. De > 0 3. B De > 0 2. BP(e1, i*, Y*) i1 C IS(e0, G1, T0) Y1 EXR Policy under Fixed EXR Interest Rate LM0 BP(e0, i*, Y*) i0 A IS(e0, G0, T0) Y0 Income, Output

BP1 IS1 De>0 LM1 LM1 De>0 i1 De>0 IS1 Y1 Y1 EXR Policy & Capital Mobility Capital Completely Immobile Capital Perfectly Mobile i i BP0 LM0 LM0 BP0 i0 i* =BP1 IS0 IS0 Y0 Y0 Y Y

BP1 IS1 IS1 De>0 De>0 LM1 LM1 i1 i1 BP1 De>0 Y1 Y1 EXR Policy & Capital Mobility Capital Relatively Immobile Capital Relatively Mobile i i BP0 IS0 LM0 IS0 LM0 De>0 i0 i0 BP0 Y0 Y0 Y Y

Summary of Policy Effects under a Fixed Exchange Rate Regime

Policy Effects with Fixed EXR • Fiscal Policy • Directly affects only the IS Curve. • Adjustments to equilibrium depend on degree of capital mobility. • Higher the degree of capital mobility, the more effective is fiscal policy. • When capital immobile, IR adjustment shifts LM in & increases i, Y fixed. • When capital mobile, IR adjustment shifts LM out & increases Y, i fixed. • Monetary Policy • Directly affects only the LM Curve. • Adjustment to equilibrium does not depend on degree of capital mobility. • Monetary policy is not effective in changing Y. • Change in Domestic Reserves brings changes in i & Y affecting FX market. • FX market disequilibrium, requires Central Bank to change Int’l Reserves by amount exactly offsetting original change in Domestic Reserves. • Exchange Rate Policy • Devaluation affects both IS & BP curves, increasing Y. • Central Bank intervention to achieve new fixed EXR brings about change.