Download

1 / 10

140 likes | 625 Vues

CAPITAL ASSET PRICING MODEL(CAPM). CAPITAL ASSET PRICING MODEL(CAPM). It is developed by Professors Sharpe & Markowitz in 1960. Prof Sharp won Nobel Prize in 1990. Types of investors. Risk taker: The investor who take risk.

E N D

CAPITAL ASSET PRICING MODEL(CAPM) It is developed by Professors Sharpe & Markowitz in 1960. Prof Sharp won Nobel Prize in 1990

Types of investors • Risk taker: The investor who take risk. • Risk Aversor: The investor who avoided risk and if he take risk he ask for more reward and in this case it is risk premium.

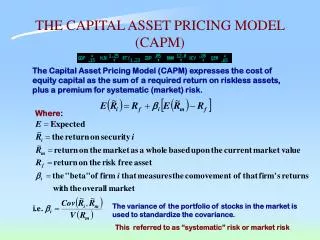

CAPM Defined • It is a model which describes the relationship between risk and expected (required) return. • In this model a security expected (Required) return is equal to risk free rate and risk premium based on the systematic risk of the security.

Mathematically CAPM is written as Rj= Rf + Bj (Rm – Rf) Where: Rj = Required (expected) rate of return of security j Rf = Risk free rate of short term govt bond Bj = It is the systematic risk of security “j” which can not be diversified. Rm = Required rate of return of market (KSE 100 index) (Rm – Rf) = Risk premium because of bearing risk “B” (beta)

Assumption of CAMP • The capital market is efficient, in that investor are well informed. • No transaction cost. • Negligible restriction on investment. • No investment is large enough to effect the market price of a stock. • There is no taxes. • The quantities of all assets are given fixed. • All assets are perfectly divisible and perfectly liquid.

Investment Opportunities • Investment in risk free securities whose return are fixed. Short term rate is used is CAPM. • Market portfolio of common stock.

Beta • It is a tendency of a Stock to move with the Market (or Portfolio of all Stocks in the Stock Market). it is the building block of CAPM. Total Risk = Diversifiable Risk + Market Risk Total Stock Return = Dividend Yield + Capital Gain Yield

Stock Risk Vs Stock Beta: Stock Risk: • It is a statistical spread of possible returns (or Volatility) for that Stock Stock Beta: • It is a statistical spread of possible returns (or Volatility) for that Stock relative to the market spread i.e. spread (or Volatility) of the fully diversified market portfolio or index. • Beta Coefficients of Individual Stocks are published in “Beta Books” by Stock Brokerages & Rating

Meaning of Beta for Share ABC in Karachi Stock Exchange (KSE): • If Share A’s Beta = +2.0 then that Share is Twice as risky (or volatile) as the KSE Market i.e. If the KSE 100 Index moved up 10% in 1 year, then based on historical data, the Price of Share B would move up 20% in 1 year. • If Share B’s Beta = +1.0 then that Share is Exactly as risky (or volatile) as the KSE Market • If Share C’s Beta = +0.5 then that Share is only Half as risky (or volatile) as the KSE Market • If you could find a Share D with Beta = -1.0 then that share would be exactly as volatile as the KSE Market BUT in the opposite way i.e. If the KSE 100 Index moved UP 10% then the price of the Share D would move DOWN by 10%! • The Beta of most Stocks ranges between + 0.5 and + 1.5 • The Average Beta for All Stocks = Beta of Market = + 1.0 Always.