Download

1 / 42

430 likes | 582 Vues

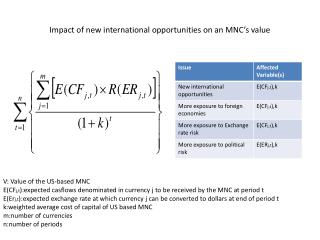

Impact of new international opportunities on an MNC’s value. V: Value of the US-based MNC E(CF j,t ):expected casflows denominated in currency j to be received by the MNC at period t E(Er j,t ):expected exchange rate at which currency j can be converted to dollars at end of period t

E N D

Impact of new international opportunities on an MNC’s value V: Value of the US-based MNC E(CFj,t):expected casflows denominated in currency j to be received by the MNC at period t E(Erj,t):expected exchange rate at which currency j can be converted to dollars at end of period t k:weighted average cost of capital of US based MNC m:number of currencies n:number of periods

General:international opportunities • New international opportunities can enhance MNC’s value.However, that advantage should be weighted by more exposure to foreign economies, exchangge rate risk, political risk that reduce it • Importers’ main source of pesimism lies in exchange rate risk • Financial managers have limited control over international trends but they have controllable exposure to them

Impact of international trade on an MNC’s value V: Value of the US-based MNC E(CFj,t):expected casflows denominated in currency j to be received by the MNC at period t E(Erj,t):expected exchange rate at which currency j can be converted to dollars at end of period t k:weighted average cost of capital of US based MNC m:number of currencies n:number of periods

Macro1:international trade • Cash flow may be affected positively by inflation rate and higher national income in each foreign country it operates • Also cash flows maybe affected by more open trade(reduced tariffs & tolls and other trade barriers • A weaker dollar brings about more exports but there is a lagging effect and less imports and intracompany trade (50% of trade)remains unaffected while other economies’ currencies many times move in tandem neutralizing the effect

Impact of Global financial Markets on an MNC’s value V: Value of the US-based MNC E(CFj,t):expected casflows denominated in currency j to be received by the MNC at period t E(Erj,t):expected exchange rate at which currency j can be converted to dollars at end of period t k:weighted average cost of capital of US based MNC m:number of currencies n:number of periods

Macro2:financial markets • Issuing stock in foreign markets brings about name recognition & credibility in that market • Financial markets reduce the cost of borrowing(ie borrow in foreign, Eurocurrency, EuroBond,Eurocredit markets) & coversely WACC • Lower interest rates in foreign countries stimulate spending and borrowing which results to more demand in the end

Impact of factors that influence exchange rates on an MNC’s value V: Value of the US-based MNC E(CFj,t):expected casflows denominated in currency j to be received by the MNC at period t E(Erj,t):expected exchange rate at which currency j can be converted to dollars at end of period t k:weighted average cost of capital of US based MNC m:number of currencies n:number of periods

Macro3:Factors related to exchange rate • Higher foreign inflation rates cause downward pressure to the foreign currency causing reduced home currency cashflows • Higher foreign interest rates cause upward pressure to the foreign currency and have favorable effect on home currency cashflows • These effects are balanced due to reduced cashflows corollary is accompanied with an inverse longer effect on foreign country growth which is to cause more demand

Impact of currency derivatives on an MNC’s value V: Value of the US-based MNC E(CFj,t):expected casflows denominated in currency j to be received by the MNC at period t E(Erj,t):expected exchange rate at which currency j can be converted to dollars at end of period t k:weighted average cost of capital of US based MNC m:number of currencies n:number of periods

Macro4:Currency derivatives • Using currency derivatives(forwards, futures, options) is double-edged :when foreign currency appreciates you lose an opportunity, having used derivatives yet protected from depreciation • Standard deviation=risk is reduced though and thus you are more trusted and have credibility when trying to raise funds due to risk aversion

Impact of Central bank intervention on an MNC’s value V: Value of the US-based MNC E(CFj,t):expected casflows denominated in currency j to be received by the MNC at period t E(Erj,t):expected exchange rate at which currency j can be converted to dollars at end of period t k:weighted average cost of capital of US based MNC m:number of currencies n:number of periods

Macro5:Government influence on exchange rates • Direct Intervention(open market operations:engaging in reserves & forex trade) can affect the values of foreign currencies which determine the expected home currency cash flows remitted from subsidiaries.Additionally also demand is affected • Indirect intervention (rates,money supply)has the same effects:ie a government of a country with substantial net-outflows(which results in severe downward pressure on its currency) will lower interest rates to prevent excesive outflows

Impact of arbitrage on an MNC’s value V: Value of the US-based MNC E(CFj,t):expected casflows denominated in currency j to be received by the MNC at period t E(Erj,t):expected exchange rate at which currency j can be converted to dollars at end of period t k:weighted average cost of capital of US based MNC m:number of currencies n:number of periods

Macro6:Effect of arbitrage • Arbitrage ensures that spot and forward rates of foreign currency in the ForEx market are aligned. • Cash flows are secured in that manner and additionally there is no cost needed to monitor exchange rates

Impact of Foreign Inflation on an MNC’s value V: Value of the US-based MNC E(CFj,t):expected casflows denominated in currency j to be received by the MNC at period t E(Erj,t):expected exchange rate at which currency j can be converted to dollars at end of period t k:weighted average cost of capital of US based MNC m:number of currencies n:number of periods

Macro7:Foreign Inflation • Higher interest rates will reflect expectation of higher inflation(IFE) which is meant to excert downward pressure on local currency against MNC’s home currency • High inflation in foreign country will multiply profit margin.(higher costs and earnings alike) • However high inflation will bring about weaker currency(PPP) that balances that effect • So what matters for MNC’s cashflows is the net effect and timing with which the two forces(parities) will manifest

Impact of Forecasted Exhange rates on an MNC’s value V: Value of the US-based MNC E(CFj,t):expected casflows denominated in currency j to be received by the MNC at period t E(Erj,t):expected exchange rate at which currency j can be converted to dollars at end of period t k:weighted average cost of capital of US based MNC m:number of currencies n:number of periods

Micro1:Forecasting exchange rates • Having the forecast, the company will choose to hedge or remain exposed. • That decission is all about setting the exchange rate at which the expected casflows will be remmited to the home country. Hedge it(fix it) or let it flow(and absorb the net effect)

Impact of Exposure on an MNC’s value V: Value of the US-based MNC E(CFj,t):expected casflows denominated in currency j to be received by the MNC at period t E(Erj,t):expected exchange rate at which currency j can be converted to dollars at end of period t k:weighted average cost of capital of US based MNC m:number of currencies n:number of periods

Micro2:Impact of Exposure • Transaction exposure is itself the cash-flow effect of absorbing the transactions of HQ/subsidiaries as they are having transactions across countries. • The MNC may take the effect even before transactions take place. If the company is competing with other firms in each geographical region, the effect of exchange rates will be felt in demand for its products (and therefore expected casflows) will be dependent on the currency in which competitors are denominating their cash flows • Also the effect on WACC will be felt(sometimes in a meaningful magnitude) as exposure increases

Impact of hedging transaction exposure on an MNC’s value V: Value of the US-based MNC E(CFj,t):expected casflows denominated in currency j to be received by the MNC at period t E(Erj,t):expected exchange rate at which currency j can be converted to dollars at end of period t k:weighted average cost of capital of US based MNC m:number of currencies n:number of periods

Micro3:Transaction exposure • The decission to hedge is itself the arrangement of rate at which the transaction will take place. • Also affected are the casflows by the decission to remain unhedged and take the risk that the foreign currency will depreciate or hedge and fix the magnitude of inflows

Impact of hedging economic exposure on an MNC’s value V: Value of the US-based MNC E(CFj,t):expected casflows denominated in currency j to be received by the MNC at period t E(Erj,t):expected exchange rate at which currency j can be converted to dollars at end of period t k:weighted average cost of capital of US based MNC m:number of currencies n:number of periods

Mucro4:Economic exposure • For a start transaction exposure is a subset of economic exposure so what was described is accounted • Subsidiaries may decide to restructure (change their debt/equity ratio or fixed/variable costs and earnings) in order to be more predictable(less exposed) • ..or even sell most of their products locally(remember that this also means restrained capacity and thus less economies of scale and therefore lost business and cash-flows)

Impact of DFI decissions on an MNC’s value V: Value of the US-based MNC E(CFj,t):expected casflows denominated in currency j to be received by the MNC at period t E(Erj,t):expected exchange rate at which currency j can be converted to dollars at end of period t k:weighted average cost of capital of US based MNC m:number of currencies n:number of periods

Micro 5: Foreign Direct Investment decissions • The revenue generated as well as the expenses rise as you move from exporting to Foreign Direct Investment. Therefore the cash flows are determined by this kind of resstructuring • But also the cost of capital may increase due to the rise of risk unless there is the opportunity to borrow locally cheaper

Impact of Multinational capital budgeting on an MNC’s value V: Value of the US-based MNC E(CFj,t):expected casflows denominated in currency j to be received by the MNC at period t E(Erj,t):expected exchange rate at which currency j can be converted to dollars at end of period t k:weighted average cost of capital of US based MNC m:number of currencies n:number of periods

Micro6:Multinational capital budgeting • Previous slide was about entering a foreign market with operations. Well, this one is about expanding within that market and it implies similar impact • When parent company supports financially the ‘new’ operations it affects the level of risk which is reflected in required rate of return and cost of capital

Impact of Multinational Restructuring Decisions on an MNC’s value V: Value of the US-based MNC E(CFj,t):expected casflows denominated in currency j to be received by the MNC at period t E(Erj,t):expected exchange rate at which currency j can be converted to dollars at end of period t k:weighted average cost of capital of US based MNC m:number of currencies n:number of periods

Micro7:Effect of multinational restructuring • A strategy of foreign expansion creates additional expected cashflows after an initial outlay • By foreign expansion we usually speak of acquiring firms, (partial or full or acquisitions of privatized firms) but also of international alliances(including licensing or franchising) or even divestures where salvage value comes into play

Impact of Country Risk on an MNC’s value V: Value of the US-based MNC E(CFj,t):expected casflows denominated in currency j to be received by the MNC at period t E(Erj,t):expected exchange rate at which currency j can be converted to dollars at end of period t k:weighted average cost of capital of US based MNC m:number of currencies n:number of periods

Micro8:Impact of Country risk analysis • A country Risk analysis can affect the value of a MNC. If a firm is expectes to acquire an Austrian firm or build a foreign subsidiary in Austria and it expect that Austrian Government is to apply a law about environmental protection then it must comply to the added complexity as far as their altered obligations are concerned • Other examples are tax & fiscal policy expectations, trade barriers even to intracompany trade, through competition in cases of subsidies local firms may enjoy and other political and financial concerns

Impact of Multinational Capital Structure Decisions on an MNC’s value V: Value of the US-based MNC E(CFj,t):expected casflows denominated in currency j to be received by the MNC at period t E(Erj,t):expected exchange rate at which currency j can be converted to dollars at end of period t k:weighted average cost of capital of US based MNC m:number of currencies n:number of periods

Micro9:Impact of a multinational’s parent’s capital structure • CC may be lower for MNCs because of larger size, access to capital, diversification • Parent must choose to support the foreign operation financially, use local debt or local equity. • Foreign Debt will cause less inflows but also less exchange rate risk since lower amounts have to be converted. • Foreign Equity may dillute ownership while it also is accompanied by less cash inflows

Impact of Long-Term Financing Decisions on an MNC’s value V: Value of the US-based MNC E(CFj,t):expected casflows denominated in currency j to be received by the MNC at period t E(Erj,t):expected exchange rate at which currency j can be converted to dollars at end of period t k:weighted average cost of capital of US based MNC m:number of currencies n:number of periods

Micro10:Impact of long term Financing • This decission dictates maturity and other provisions on long-term debt securities issued.It also pinpoints to the currency used to denominate debt if not local sources are to be used • Disparity among interest rates may cause such a decission • Cost of debt describes cost of capital and thus required rates of return

Impact of Trade Financing Decisions on an MNC’s value V: Value of the US-based MNC E(CFj,t):expected casflows denominated in currency j to be received by the MNC at period t E(Erj,t):expected exchange rate at which currency j can be converted to dollars at end of period t k:weighted average cost of capital of US based MNC m:number of currencies n:number of periods

Macro11:International trade financing • International trade financing may enable the MNC to trade with foreign customers and have more inflows • Also it may purchase supplies at lower cost through importing and use of international trade financing

Impact of Short term Financing Decisions on an MNC’s value V: Value of the US-based MNC E(CFj,t):expected casflows denominated in currency j to be received by the MNC at period t E(Erj,t):expected exchange rate at which currency j can be converted to dollars at end of period t k:weighted average cost of capital of US based MNC m:number of currencies n:number of periods

Micro12:Short-term financing decission • To the extent that MNC’s parent van achive short-term financing in currencies that will reduce short-term financing expenses, it can maintain less cash to cover them • Consequently, it frees up additional cash flow to be used where it will generate more profit …or enable the subsidiary to time cash-outflows for a more lucrative conversion

Impact of International cash management on an MNC’s value V: Value of the US-based MNC E(CFj,t):expected casflows denominated in currency j to be received by the MNC at period t E(Erj,t):expected exchange rate at which currency j can be converted to dollars at end of period t k:weighted average cost of capital of US based MNC m:number of currencies n:number of periods

Micro13:international cash management • If subsidiaries excess cash reserves are used to purchase currencies in international opportunistic cash equivalents market (usually by the application and extent netting enables them) it may succeed to improve cash-inflows to home country