Subchapter S Corporation

Subchapter S Corporation. Ryan Stachler , Grant Hollingsworth, Jack Armstrong . Definition. An S corporation is a corporation that has elected S corporation tax status Elect to pass corporate income, losses, deductions, and credits through to their shareholders for tax purposes

Subchapter S Corporation

E N D

Presentation Transcript

Subchapter S Corporation Ryan Stachler, Grant Hollingsworth, Jack Armstrong

Definition • An S corporation is a corporation that has elected S corporation tax status • Elect to pass corporate income, losses, deductions, and credits through to their shareholders for tax purposes • Forming an S corporation allows companies to have the limited liability of a shareholder

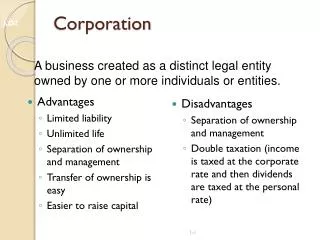

Advantages • Avoid double taxation- only shareholders pay taxes on gains • Shareholder limited liability- shareholders are not responsible for accumulation of debts, assets, or lawsuits

Advantages Cont. • Easy to raise money- they can issue stock to finance expansions, pay debt or finance other activities • Existence- they exist for an unlimited amount of time. The owner can die and it still goes on • Once a year tax filing requirement- c corporation must do it four times a year

Disadvantages • Extra accounting- The tax return is much more complicated compared to a sole proprietorship because of the numerous shareholders • Not eligible for dividend deductions • Additional banking procedures/legal costs

Disadvantages Cont. • Shareholder ownership restrictions- can only have 100 shareholders and they must be a US citizen • Closer IRS scrutiny- Because amounts given to shareholders can be dividends or salary, the IRS makes sure they are being paid for what they do

How to set up • Review the requirements and organize your business according to those requirements • Must meet the following requirements: be a domestic corporation, have only individual shareholders or certain trusts, no more than 100 shareholders, only one type of stock

How to Set Up Cont. • Form a corporation under your states business laws. This includes filing the articles of organization 4. File IRS Form 2553 which allows your business to be taxed under the subchapter S tax code.

How it is taxed • The way they are taxed looks like that of a sole proprietorship or partnership • They are not subject to corporate taxes • They don’t have to pay federal income tax; instead, shareholders pay taxes on certain capital gains

Examples • As of today there are around 4.5 million S corporations • Many of the small businesses in America • Gingrich Productions • MAKO surgical corp. • EMTEQ Electrical & Mechanical Technologies

Citations • http://www.irs.gov/Businesses/Small-Businesses-%26-Self-Employed/S-Corporations • http://www.sba.gov/content/s-corporation • https://www.ftb.ca.gov/businesses/bus_structures/sCorp.shtml • https://www.incorporate.com/s_corporation.html • http://www.entrepreneur.com/encyclopedia/subchapter-s-corporation