Download

1 / 19

190 likes | 309 Vues

This document outlines the operational budgeting, costing methodologies, and invoicing models utilized in PCB manufacturing within the fiscal year 2010. It presents a comprehensive view of the investment strategies, outsourcing management, and budgetary allocations for various processes including design, assembly, and maintenance of workshop equipment. Detailed insights into expenses, invoicing methods, and the development of new processes highlight effective management practices aligned with fiscal responsibilities and operational efficiency.

E N D

TE-MPE-EMCosting Betty Magnin

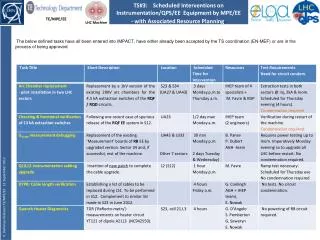

Costing History Operational budgets Invoicing Costbalancing over fiscal year

Budgetary situation (2010) PCB Manufacturing Design office Subcontracting Assembly workshop

2010 pricing model • Operational budget for non invoiceableexpenses • Librarie * • Outsourcing management and follow-up * • Maintenance of workshop equipments • Investmentstrategy • Planifiedexpenses for the replacement of existingequipement (10% of the installed value)* • Expenses for new processes to becharged to the product *4 dedicated budget codes

Operational budget • Libraries (89511) • Altium 1 FSU * • (waspreviouslyallocated for PCAD sinceyears) • 30k/yearpaid by ELEC • Cadence 1 FSU * • Until 2011, wasdone by 2 and then 1 staff, retired 06/2011 * 1 FSU = 100k/year

Operational budget • Outsourcing management (89512) • Before 2009, required 2 FSU • 2010, reduced to 1 FSU • 2011, change S107 to S144, profile reviewedfrom administrative to technician • 2012, increased to 2 FSU • 2013 : impact of LS1 ? • FSU: possible to adaptcapacity to load (3 monthsadvice)

Investment in infrastructure • PCB workshop, 1770k for the last 6 years • Machines for large MPDG 600k • Laser Direct Imaging 700k • Flying probe electricaltester 30k • AOI 380k • Planning tool 60k • Forecast: • Migration into B107 • Laser

Investment in infrastructure • Assemblyworkshop: 650k for the last 6 years • Screen printing of solder paste 30k • Automatic placement 270k • Inspection 30k • Cleaning 50k • Press-fit inserter 30k • BGA repair 110k • Replacement of the reflowoven 200k • Pastedepositionby jet printing 200k • CAD-CAM software (Aegis) 30k

Investment in infrastructure • Repair workshop (B867) • Humidity and temperature control • Copy of the repair area in the assembly workshop • Specific RP constraints (fume extraction, ..)

Invoicing model • 1 job = 1 invoice (JMT or RFF) • Individual if direct demands (PCB or Assembly) • Global if Design + PCB + Components + Mechanics + Assembly • No «overhead» • Atcompletion of the job • Expenses and invoicingthrough the transitory budget codes of the section.

Calculationmethods • Design office • FSU: 1 design = 1 job (JMT) • Estimation based on the technicalparameters of the layout • Invoiced on the actualelapsed time • Invoiced to the user on the basis of • The elapsed time invoiced by FSU • Effective hourly rate 72.- CHF

Calculationmethods • Standard PCB at CERN (done by FSU Team) • Invoiced on the basis of • Technical parameters of the product • Hourlycost of FSU • Consumable costs • MPGD (done by staff) • Invoiced on the basis of • Technical parameters of the product • Elapsed time • Consumable costs

Calculationmethods • Assembly at CERN • Invoiced on the basis of • Elapsed time for manualwork (prototypes, rework and repair) • Technical parameters of the product for machine placement • Consumable costs

Calculationmethods • Components • Invoiced on the basis of the real cost • Mechanical parts • Invoiced on the basis of the real cost • Outsourcedassembly • Invoiced on the basis of the real cost

Costfollow-up Based on payment, according to CET data. Each area of the section has a dedicatedtransitory code Design Office 89509

Costfollow-up PCB Workshop 89569

Costfollow-up Assembly Workshop 89529

Costfollow-up Subcontracting and components 89519